E2V has now released its final results for the year ended 2016.

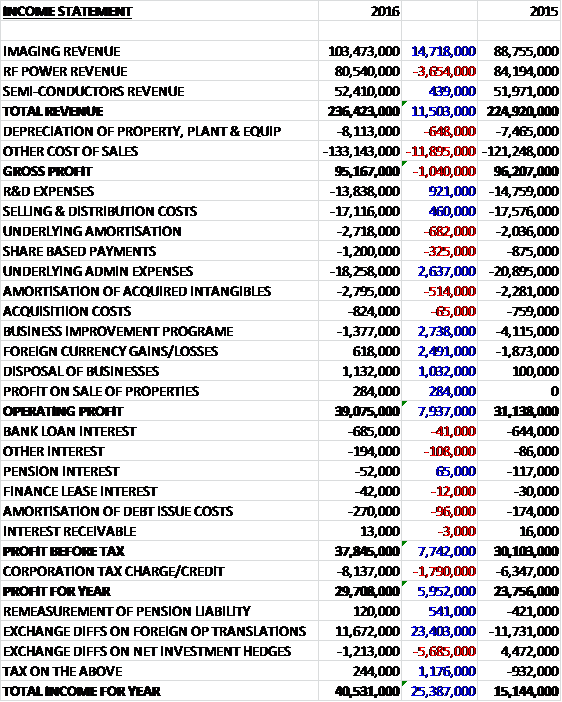

Revenues increased when compared to last year as a £3.7M decline in RF Power revenue was more than offset by a £14.7M growth in imaging revenue with semi-conductor revenue remaining broadly flat. By geographical spread, revenue was up in Asia Pacific and steady in North America and Europe. Cost of sales grew at a faster rate, however, due to a £5.5M swing to forex losses on the retranslation of working capital and realised losses on forex contracts (although this was offset by a 2.4% increase in revenues through beneficial forex movements), so gross profit fell by £1M. R&D expenses fell by £921K and selling & distribution costs reduced by £460K but underlying amortisation grew by £682K and share based payments increased by £325K, offset by a £2.6M decline in other underlying admin expenses.

Overall, non-underlying costs were much more favourable than last year as a £514K growth in the amortisation of acquired intangibles was more than offset by a £2.7M decline in restructuring costs and a £2.5M positive swing in forex relating to the hedging instruments. The group also benefited from a £1.1M gain from the disposal of the thermal imaging business and a £284K profit from the sale of properties to give an operating profit some £7.9M above that of last year. Interest costs increased modestly and there was also a £1.8M growth in tax charges relating to deferred tax gains last year following the government’s announcement of a reduction in corporate tax rates, which meant the profit for the year came in at £29.7M, a growth of £6M year on year.

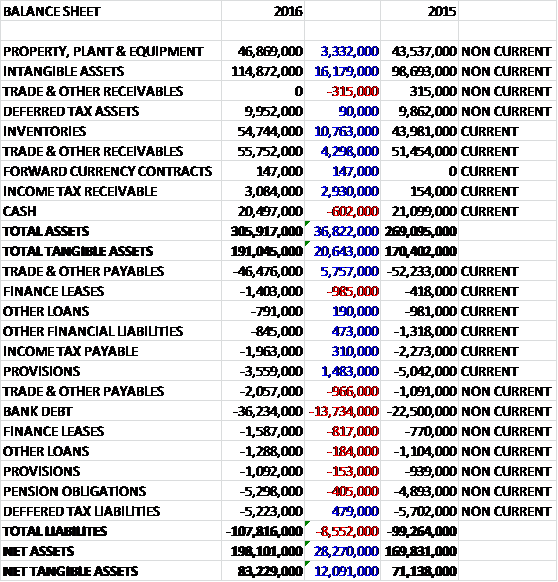

Total assets increased by £36.8M when compared to the end point of last year, driven by a £16.2M growth in intangible assets, a £10.8M increase in inventories, a £4.3M growth in receivables, a £2.9M increase in income tax receivable and a £3.3M growth in property, plant and equipment. Total liabilities also increased during the year as a £13.7M growth in bank debt as partially offset by a £4.8M decrease in payables and a £1.3M fall in provisions. The end result is a net tangible asset level of £83.2M, an increase of £12.1M year on year.

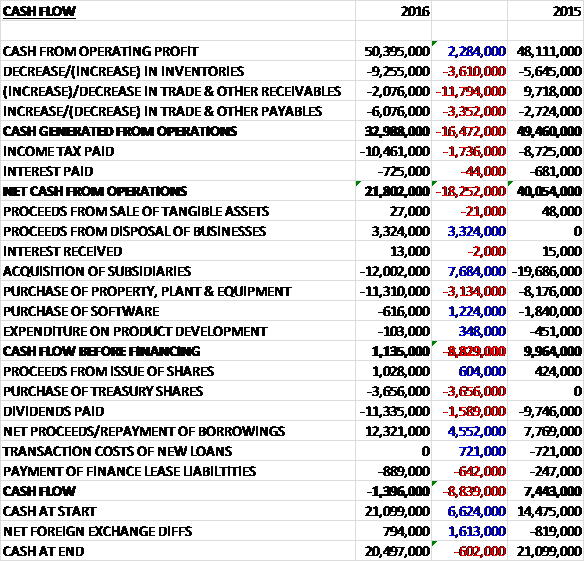

Before movements in working capital, cash profits increased by £2.3M to £50.4M. There was a large outflow of cash through working capital, however, in particular a decrease in payables and a growth in inventories which meant that after tax payments also grew by £1.7M, the net cash from operations came in at £21.8M, a decline of £18.3M year on year. The group spent £11.3M on property, plant and equipment along with £616K on software and after the thermal imaging business sale is taken into consideration, they spent a net £8.7M on acquisitions with left them with just £1.1M before financing. This didn’t even cover the £3.7M spent on shares for the director awards let alone the £11.3M of dividends so the group took out new loans of £12.3M to give a cash outflow of £1.4M and a cash level of £20.5M at the year-end.

The adjusted operating profit in the Imaging division was £15.7M, a growth of £6.4M year on year on revenues that increased by 17%, although when the contribution from the acquired business and the favourable forex movement is excluded, like for like revenues were up 12%. Underlying growth came from strong demand in automatic data collection, machine vision sensors and optical inspection CMOS cameras. Life sciences delivered modest growth reflecting stronger end user demand. In Space, revenue growth came through delivery on programmes, although these programmes remain technically challenging and the group is continuing to commit the resources needed to improve delivery to their customers (read: probably not profitable contracts then).

The overall profit growth reflects the contribution from the revenue growth with professional imaging delivering improving margins and in space margin improvement reflects the benefit of improving operational performance. R&D activities have been increased to drive future growth, focusing on areas of strong customer demand such as industrial automation and space. The business has widened its scope of services with the integration of AnaFocus that provides customer specific CMOS sensors for a wide range of applications, although the thermal imaging was sold during the year.

In Space, the group have established a new management team under a new divisional president and they have seen the start of some operational improvement and better delivery to customers. The recovery programme being addressed by the management team is complex, however, and will take some time. The board are pleased with the pace of progress though as a year ago they had ten larger problem contracts and in the year fur of these have been delivered and their financial position improved with a further five due for delivery in the coming year.

At the year-end, the order book stood at £93M compared to £90M at the end point of last year and the orders for delivery over the next year are £60M compared to £70M, reflecting delivery on space programmes and the shorter order cycle nature of the professional imaging business. The focus for the coming year in professional imaging is to make new markets and take market share whilst in space the focus is on embedding the operational changes and deliver ongoing margin improvement.

The adjusted operating profit in the RF Power business was £17.8M, a decline of £670K when compared to last year on revenues that fell by £3.7M. This decline came about as a modest growth in radiotherapy reflecting increased demand from key OEM customers along with growth in commercial and industrial markets was more than offset by weakness in defence with slower than anticipate programme wins and a pause in industrial processing systems.

The decline in profit reflected a modest improvement in the margin to 23.2% due to cost control and the alignment of the cost base in defence to the expected activity level. R&D activities continue to be focused primarily on radiotherapy applications. The board continues to expect that spares revenue will grow in line with the past expansion of the installed base which should account for about two thirds of growth with the rest expected from continued new build demand. In defence, the key driver of growth is the level of NATO defence spending. Defence budgets across the NATO countries are currently constrained and the board do not expect this to change in the short term despite global and regional threats.

The majority of the growth in the division is anticipated to come from radiotherapy where the group continue to prioritise their investment. Their other applications continue to be driven by the general industrial cycle and as discussed, defence will remain subdued reflecting defence budgets. During the year the group made progress on their site restructuring programme and it is anticipated that it will be completed over the next two years. They have also established separate units for the Lincoln-based defence activities.

The adjusted operating profit in the Semi-conductors division was £14.2M, an increase of £3.9M when compared to 2015 on revenues that were broadly flat when the £600K contribution from the acquired SP Devices business is excluded. US legacy product lines saw revenue increase from flow down on programmes, along with good growth coming from their own design high speed data converters for space applications. This was offset by lower demand for microprocessors. In other applications there was the anticipated decline in the legacy ASIC business as those products approach the end of their life cycle.

The profit growth represents a significant improvement in the margin due to an improved product mix, good cost control and an improved operational performance. The board see continued ongoing market growth for high reliability products in civil aviation production rates which have seen high single figure growth rates. Their own designed space qualified data converters are winning market share as they enable their customers to reduce the size and weight of their satellites and at the same time increase the number of communication channels. The steady demand for products that are provided primarily into defence applications is driven by the flow down of funds into the large defence OEMs.

The SP Devices business provides sub-system solutions for analogue to digital conversion applications. These are used by customers including leading OEMs across a number of sectors including industrial test and measurement, healthcare, communications and science. It also brings proven patented technology in software and board level sub-systems and services.

The order book at the year-end was £20M, flat year on year with orders for the next twelve months down £3M to £15M reflecting the anticipated decline in the legacy ASICs business and some delays to anticipated orders in Q4. The focus for the coming year is on delivering growth from the product line acquisitions and announced microprocessor last time buys. They will continue to invest in cards, subsystems and their own IP development moving up the value chain.

The customer service seems to be improving at the group with their customers providing improved scores in their most recent customer survey. Although, as part of the recent focus on customers and to improve responsiveness, the group have increased their inventory levels which has contributed to the cash outflow seen in working capital. It is worth noting that in the second half of the year the group cut capex to the same level as depreciation to try and offset the working capital cash outflow. In the coming year, however, it is expected that capex spending will be some £14M higher than depreciation as the Chelmsford reorganisation continues.

Towards the end of January the group acquired Signal Processing Devices Sweden, a company specialising in the design and development of analogue to digital processing technology. The business brings proven patented technology in software which complements E2V’s existing broadband data converter business. It is reporting in the semiconductors business segment. The group paid a total consideration of £12.6M consisting of £9.8M in cash and £2.8M in contingent consideration with a total goodwill of £10.2M being generated on the transaction. In the two and a bit months since acquisition, the business contributed operating profit of £92K and had the acquisition taken place at the start of the year, it would have contributed £300K.

As can be seen there were a number of non-underlying costs. The group completed the acquisition of SP Devices in January which incurred transaction costs of £232K. There were also exchange losses of £199K relating to the outstanding contingent consideration for both SP Devices and last year’s acquisition, Anafocus. In addition there were costs of £393Km relating to payments from the acquisition dependent upon future employment.

During the year the group repositioned its regional teams in the US and Asia so that they are aligned with the group divisions, and they have also reorganised RF’s defence business into three distinct units. Costs of £1.2M have been recorded principally relating to staff costs and including £214K to establish a new facility in Lincoln for the microwave business unit. The reorganisation of the Chelmsford facility continued in the year with costs of £441Km incurred in the period.

Last year group have also announced that they will cease manufacturing in China in the first half of the coming year and they also started a consultation process regarding the planned closure of the sales office in Bievres in France. As these programmes progressed during this year, a credit of £269K was recorded due to an onerous lease provision that is no longer required.

In October the group sold its thermal imaging business. The net proceeds on the transaction were £2.9M and a gain on the sale of £1.1M was recorded. The £284K recorded for the property sale relates to the 2010 disposal of a former Lincoln site whereby further payment was received depending on the square footage of the new properties built on the site.

The prevalent exchange rates at the end of the year would give rise to a 7% revenue tailwind going forward and the net benefit on adjusted operating profit is estimated at 4%, although exchange rates do of course remain volatile as always.

Going forward, whilst the board remain cautious about the broader economic environment, their outlook for 2017 remains unchanged with a similar first half/second half weighting to that seen in 2016. The group closed the year, as expected, with a 12 month order book of £130M, a decrease of 11% when compared to the end point of the prior year. This reflects the changing composition of the group’s revenues with growth coming from shorter order cover businesses, delivery on programmes in space and the cycle of the radiotherapy business along with the anticipated decline in RF Defence.

The goal remains to double the adjusted operating profit in the five years from 2015. This seems dangerous to me as some of the sluggish markets the group is involved in means that this will have to come from acquisitions with the associated increase in gearing or shareholder dilution.

At the year-end the group had a net debt position of £20.8M compared to £4.7M at the end point of last year. At the current share price the shares are trading on a PE ratio of 14.4 which falls to a decent looking 12.8 on next year’s consensus forecast. After a 5.9% increase in the total dividend the shares are yielding 2.8% which increases to 3% on next year’s forecast.

Overall then, this has been a fairly solid year for the group. Profits were up and net assets increased along with cash profits. Due to a large build-up of working capital, the operating cash flow declined, however, and the group did not manage to produce much free cash, certainly not enough to cover the dividends. The imaging business performed well, driven by growth in automatic data collection, machine vision sensors and CMOS cameras. The Semi-conductors business also saw an increase in profits but this was due to an improved product mix and cost cutting rather than top line growth.

The RF Power business fared less well, however, with the poor performance driven by reduced demand from the defence sector. It is worth noting that capex is going to increase in the coming year and the closing order book has deteriorated, although this is put down to an increase in business with shorter order cover. With a forward PE pf 12.8 and dividend yield of 3%, the shares are probably priced about right.

On the 7th June the group announced that director Stephen Blair purchased 10,000 shares at a value of about £20.5K. This transaction gives him 129,338 shares in total so a good sign despite not being a massive purchase.

On the 13th July the group released an update covering Q1. Activity in what is typically a quiet period was muted but they expect to deliver a strong improvement in Q2, supported by order intake secure during June. Cash collection has been in line and they have targeted inventory reductions to improve on the planned year-end net debt reduction. The outlook for the current year, subject to the broader economic environment remains unchanged with 60% of revenues to be made in the second half.

Professional imaging is seeing demand continuing to grow for industrial automation, particularly in Asia. Order intake across its activities increased in June for delivery in Q2and there is a good pipeline of opportunities which support the anticipated revenue profile for the rest of the year. Space Imaging has good order cover in the short term and the board are confident of securing the follow-on production orders where they are designed into major programmes. This underpins a significant step-up in revenue anticipated in H2 and builds the order book cover for the next year. Space Imaging is along cycle business and continues to experience challenges on its technologically demanding programmes.

RF Power is seeing improving demand in radiotherapy and continues to deliver to its OEM customers under the existing contracts, which are expected to be renewed before the year-end. In commercial and industrial, they expect demand to remain steady. The defence business has the opportunity pipeline to support its anticipated revenue profile but there have been some recent delays in programme awards. In Semiconductors, the group achieved strong order intake in June for the component portfolio and this supports the Q2 revenue delivery. The anticipated revenue profile is expected to be supported by their partnership with Peregrine Semiconductors, product line acquisitions made in the prior year, NXP last time buy and SP Devices.

Cash generation in the quarter reflected the expected collection of year-end receivables and net borrowings decreased by £11.2M to £9.9M. It is expected that net borrowings at the half year to be broadly in line with the position at the prior year-end, however.

They have increased their focus on working capital management. They have reduced manufacturing cycle time in space imaging and they have made good progress with their reorganisation of the Chelmsford site. When completed within the next two years, it will provide further reductions in manufacturing cycle time and associated working capital. Semiconductors has implemented an inventory reduction plan, which is expected to deliver a reduction in inventory by the end of the year and represents most of the incremental inventory improvement of £5M to enhance the planned year-end net debt reduction. Over the next two years the board see the opportunity for further reduction in working capital by £10M coming from delivery of a more even revenue profile and further shortening of manufacturing cycle time.

A 1c strengthening in the US dollar relative to Sterling is expected to increase revenues by about £1M with a 40% drop through to operating profit so the group should be benefiting from the recent forex movements.

The group have also announced that Finance Director Charles Hindson will not stand for re-election at the next AGM after being in the role for the past seven years.

Overall then, this is a decent update. The slow-down in Q1 is concerning, however, and I am a bit nervous when companies have to increase their performance in the rest of the year to hit targets – although the increased orders suggest this is possible for E2V. The recent weakness in Sterling is also a positive for the group but there just seems to be a bit of uncertainty at the moment and I think a clearer picture of group performance should have emerged by the interim results stage so I’m holding back for now.