Following acquisitions in the year the group has four operating segments: Commercial Jet Broking, Private Jet Broking, Freight and Baines Simmons. Cabot Aviation services results are aggregated into Commercial Jet Broking. Air Partner has now released its final results for the year ended 2016.

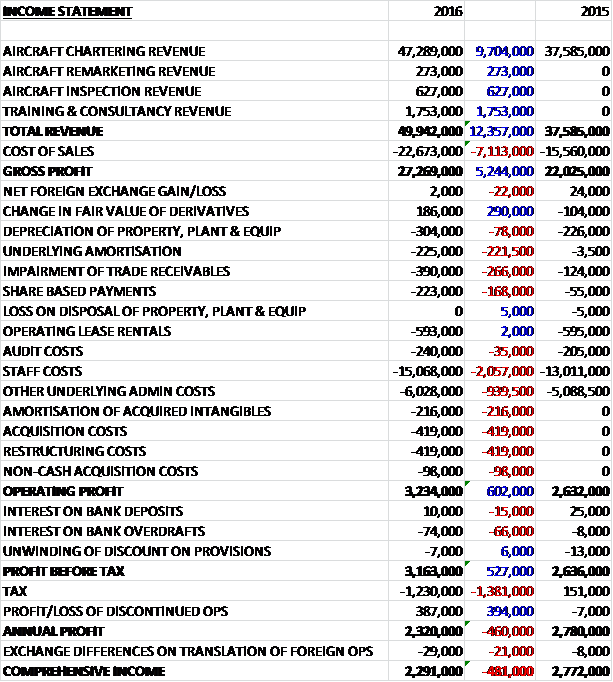

Revenues increased when compared to last year with a £9.7M growth in aircraft chartering revenue and a £1.8M increase in training and consultancy revenue. Cost of sales also increased to give a gross profit £5.2M above that of 2015. The group benefited from a change in the fair value of derivatives but this was offset by a £222K growth in underlying amortisation, a £266K increase in the impairment of trade receivables, a £168K growth in share based payments, a £2.1M increase in other staff costs and a £938K increase in other underlying admin costs. We also see some non-underlying admin costs such as £517K of acquisition costs, £419K of restructuring costs, and £216K of amortisation of acquired intangibles to give an operating profit £602K above last year. There was a modest increase in finance costs but tax costs grew by £1.4M due to last year’s US tax credit not being repeated which meant the profit for the year came in at £2.3M, a decline of £460K year on year. The profit from discontinued operations relates to the release of a provision for claims by former employees which have lapsed.

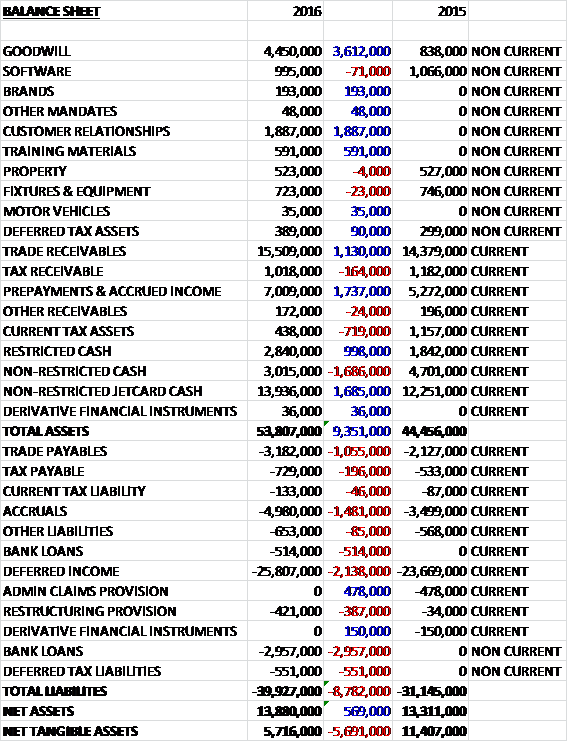

When compared to the end point of last year, total assets increased by £9.4M driven by a £3.6M increase in goodwill, a £1.7M growth in prepayments and accrued income, a £1.9M increase in customer relationships and a £2.7M increase in jetcard cash, partially offset by a £1.7M decline in other cash and a £719K fall in current tax assets. Total liabilities also increased during the year due to a £3.5M growth in bank loans, a £2.1M increase in deferred income, a £1.5M growth in accruals and a £1.1M increase in trade payables. The end result is a net tangible asset level of £5.7M, a decline of £5.7M year on year.

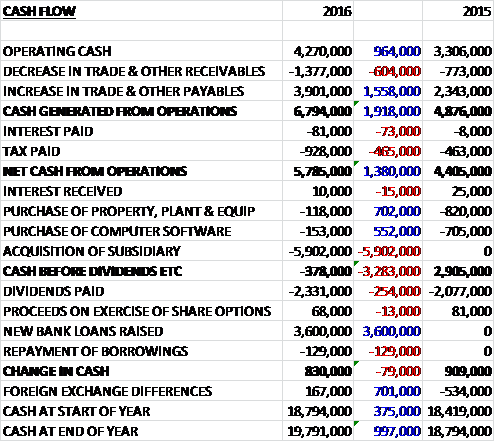

Before movements in working capital, cash profits increased by £964K to £4.3M. There was a cash inflow from working capital due to an increase in payables and after tax and interest both grew, the net cash from operations was £5.8M, a growth of £1.4M year on year. The group spent all of this on the acquisitions so with negligible capex elsewhere, there was a cash outflow of £378K before financing. The group then raised £3.6M from a new loan which paid for the £2.3M in dividends which gave a cash flow for the year of £830K and a cash level of £19.8M at the year-end.

The underlying operating profit in the Commercial Jet Broking business was £3M, a growth of £259K year on year driven by strong trading in the UK and Europe which benefited from a larger tour operating programme compared to the prior year. During the period the group was a beneficiary of a guarantee from one of its Tour Operating clients in Southern Europe and in the latter part of the year, following late payment from the client, they claimed against the guarantee. The claim was disputed by the guarantor and is now subject to court action which led to a £400K provision in H2.

Within the UK commercial jet team the group focused on developing a clearer sales strategy, invested in new staff and focused on improving the service levels they provide. There was a strong contribution in the oil and gas and sports sectors along with continued government work. Trading in Europe benefited from a larger tour operating programme as well as a strong performance in Germany. Austria delivered a stable performance while results in Italy were down year on year due to government related work in the previous year not being repeated. Despite some new customer gains, the performance in the US was below management expectations due to a lower number of one-off charters as well as less activity than expected from a key customer.

Cabot Aviation results are included in this division with their main business being acting as an agent and broker to airlines and other aircraft owners such as banks, operating lessors, manufacturers and insolvency practitioners, to dispose of their surplus aircraft. The business also advises clients on the acquisition of aircraft and their fleet management process. The integration has gone well and the group have extended their remarketing product range to include private jets. They have also placed their wet lease operations within the remit of the Cabot management team. In the second half of the year the business was appointed as exclusive marketing agent by China Airlines for two B747s and by Kenya Airways for four B777s, two of which have been delivered at the start of the coming year.

The underlying operating profit in the Private Jet Broking division was £2.4M, an increase of £1.6M when compared to last year, aided by prior year profits being impacted by increased investments into Jet Card. The increasing profitability was largely driven by a very strong performance in the UK, a solid performance in Europe, but somewhat offset by a weaker performance in the US. The ad hoc broking performance has been mixed. While the performance in the UK was strong, the US and European businesses have experienced a decline in profit which is being addressed this year.

Jet Card cash deposits at the year-end stood at £16.8M, up on the prior year balance of £14.1M and the number of Jet Cards stood at 209, an increase of 12 year on year. Jet Card profit is not recognised until the client has flown hours and the focus has been to increase the number of cards and to improve the frequency of use which is reflected in the utilisation rate which has increased by 33%.

The underlying operating profit in the Freight Broking business was £767K, a growth of £399K when compared to 2015. The business has continued their work with government aid agencies to assist in a number of geopolitical crises and in addition, strong growth has been seen in the German and US businesses. They have benefited from their focus on developing stronger relationships and a good reputation with freight forwarders. In addition, their Red Track technology has contributed to the success of their aircraft on ground business.

The underlying operating loss in the Baines Simmons business was £99K which represents a maiden contribution which reflected the disruption caused by the sale processed and the costs associated with the change of ownership. Good integration progress has been made across central functions and an interim MD has been appointed to drive integration with the group with the business being restructured into training, consulting and outsourcing. They have implemented a new leadership and executive team and begun the roll out of the Customer First programme. Since the end of the year, the business has been awarded a ten year contract to provide aviation support services to the Isle of Man Aircraft Registry.

During the year the group embarked on their “Customer First” programme to improve their customer service proposition. Certain components of customer’s interaction with the group were identified that could be improved. Phase one of the programme was completed with the roll out of across the entire booking and Customer First principles were applied to the acquired businesses.

In May the group acquired Cabot Aviation Services, a global aircraft remarketing broker which adds significant aircraft sales and dry lease expertise to the group. In August they acquired Baines Simmons, an aviation safety consultant which will enable the group to extend their service and product capabilities with offerings complementary to their existing broking business. The total consideration for Cabot was £814K, consisting of £514K of cash and £300K of equity which generated goodwill of £787K. The total consideration for Baines Simmons was £5.7M, satisfied entirely in cash and generating £2.8M of goodwill. Cabot contributed a loss of £95K and Baines Simmons a loss of £74K but had they both been contributing for the full year, they would have generated a loss of £15K and a profit of £117K respectively.

At the start of May, Amanda Wills and Shaun Smith joined as non-executive directors. Amanda was previously CEO of Virgin Holidays whilst Shaun was finance director at Aga Rangemaster and is currently finance director at Norcros. At the AGM, non-executive director Andrew Wood stepped down from the board after five years in the role.

Trading in the current financial year is encouraging and given the full year contribution expected from the two acquisitions, the board enter the year with a degree of optimism. Operational challenges remain, however, particularly the performance in the US and the sluggishness of Private Jets in Europe with improvements needed in those areas. In addition, ad hoc charters are likely to continue to be impacted by economic instability in the major world markets for the foreseeable future.

At the current share price the shares are trading on an underlying PE ratio of 13.7 which reduces to 10.4 on next year’s consensus forecast. After a 10% increase in the final dividend, the shares are yielding 6% which increases to 6.2% on next year’s forecast with the board stating that it is looking to build a dividend cover to between 1.5 and 2 times underlying EPS. Not including the Jetcard cash, the net debt position is £500K compared to a net cash position of £4.7M at the end point of last year.

Overall then this has been a decent year for the group. Profits did decline but this was entirely due to the non-recurrence of last year’s tax credit and pre-tax profits rose. Net tangible assets declined but operating cash flow improved, although after acquisitions there was no free cash flow. All parts of the business saw operating profits improve with a notable performance from the Private Jets broking division. Overall the performance in the UK and Germany was good whilst it was more disappointing in the US and Italy.

The acquisitions are yet to really contribute to the business but they seem sensible enough. So far this year, the market seems to be rather difficult but the board remain confident and with a forward PE of 10.4 and dividend yield of 6.2% these shares continue to look good value and I remain a holder.

On the 25th August the group released an update covering the first six months of the year. Trading has been strong and as a result, underlying pre-tax profit is expected to be at least £3M compared to £2.2M in the first half of last year, with a strong net cash position. The broking division has seen a strong like for like performance and the trading & consultancy division has started the year well, winning a number of new commercial and government contracts.

The board remains optimistic about their prospects for the remainder of the year. This all seems positive for me, I have bought back in here.