Dewhurst has now released its interim results for the year ending 2016.

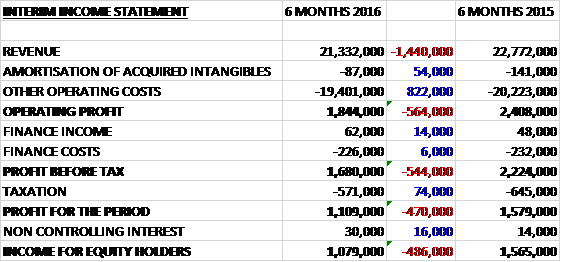

Revenue declined by £1.4M but operating costs also fell, down by £876K to give an operating profit £564K below the first half of last year. Finance costs saw a modest decline by tax was down £74K to give a profit for the period of £1.1M, a decline of £486K year on year.

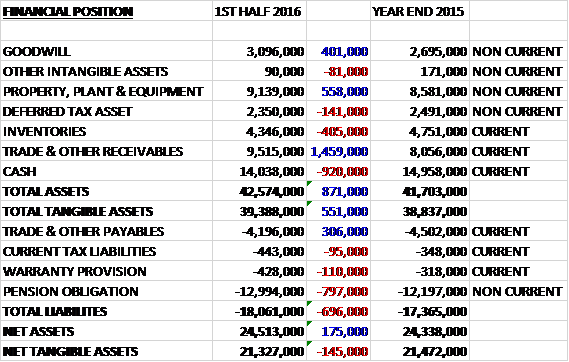

When compared to the end point of last year, total assets increased by £871K driven by a £1.5M growth in receivables, a £558K increase in property, plant & equipment and a £401K growth in goodwill, partially offset by a £920K decrease in cash and a £405K decline in inventories. Total liabilities also increased during the year as a £797K growth in the pension obligation and a £110K increase in the warranty provision was partially offset by a £306K fall in payables. The end result was a net tangible asset level of £21.3M, a decline of £145K over the past six months.

Before movements in working capital, cash profits were flat at £2.6M. There was an outflow of cash from working capital, in particular an increase in receivables, and after tax payments grew by £299K the net cash from operations was £108K, a decline of £755K year on year. This didn’t cover the net £612K spent on capex and after £86K was also spent on non-controlling interests, before financing there was a cash outflow of £528K. After dividends were paid out, the cash outflow for the period was £1.4M and the cash level at the period-end was £14M.

Market conditions were challenging during the period with the Q1 performance being particularly weak. Sales did recover in Q2 but confidence remains somewhat fragile. In the lift businesses, the UK and Australia were generally weaker while in North America sales were up. Keypad sales were well down, however, and there was a change in the mix of customer products. Transport products bounced back from last year’s low levels to record an improvement. Currency movements reduced revenue by about £400K with weakness in the Australian and Canadian dollar.

Going forward, demand overall seems to be continuing at the level of Q2 but there is a great deal of uncertainty in the political and economic situation. Public sector spending restraints are unlikely to easy any time soon and customers’ concerns about pricing are unlikely to diminish. The group are therefore focused on controlling expenditure whilst continuing to push ahead with appropriate investments to improve the business in the longer term.

After the interim dividend was kept the same, the shares are yielding 2.2% which doesn’t seem to compensate for the increased uncertainty for the business so I remain out.

On the 30th August the group released a trading update for the year ending 2016. The recovery reported at the interim stage has continued through Q3 and into the fourth quarter to date. Seasonal effects mean that H2 is traditionally stronger than the first half but the effect is expected to be greater than usual this year. If currencies remain broadly at today’s level through to the end of September, it will benefit the reported sales and profits for the year.

The Brexit vote has not yet affected the group’s underlying level of business. There have been reports in the media of cancellations and deferrals in commercial property transaction but it is too early to say what impact this will have. The combined effects of these factors mean that the board now expect full year profits to be significantly higher than current market expectations.

Despite the slightly concerning comments around Brexit, this is a good update and I have purchased some shares here.

On the 14th November the group released a trading update covering the year ended 2016. The recovery reported in August continued through Q4 and whilst seasonal effects mean the second half is traditionally stronger than the first, the effect this year has been greater than usual. A significant proportion of the group’s sales and earnings are generated in foreign currencies and the depreciation of Sterling has continued to benefit reported sales and profits. Accordingly, the board currently expects revenues to exceed £47M this year with a positive impact on profits compared to current market expectations.

This all seems good here, I continue to hold.