Red24 has now released its final results for the year ended 2016.

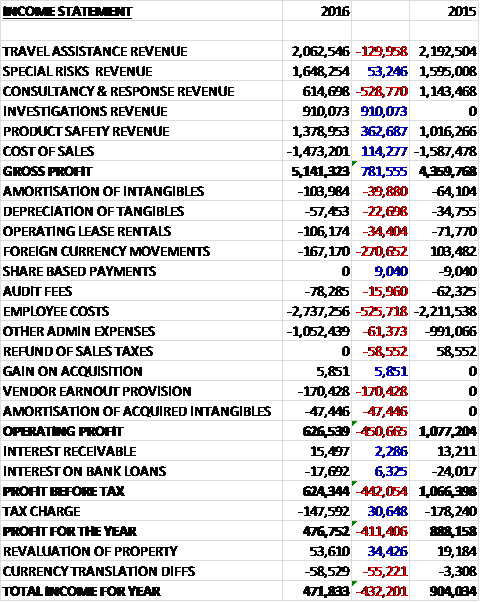

Revenue increased when compared to last year as a £529K decline in consultancy and response revenue and a £130K decrease in travel assistance revenue was more than offset by a £363K increase in product safety revenue and a maiden £910K revenue contribution from investigations. Cost of sales was down £114K to give a gross profit £782K above that of 2015. Amortisation, depreciation and operating lease rentals all saw modest increases and foreign currency movements saw a £271K detrimental movement due to the depreciation of the Rand. Employee costs increased by £526K and other admin expenses were up £61K. We also see the lack of a £59K refund of sales tax that occurred last year, plus a £170K vendor earn-out provision and a £47K amortisation of acquired intangibles which meant that the operating profit fell by £451K. We then see tax charges down £31K and most declines in interest costs to give a profit for the year of £477K, a decline of £411K year on year.

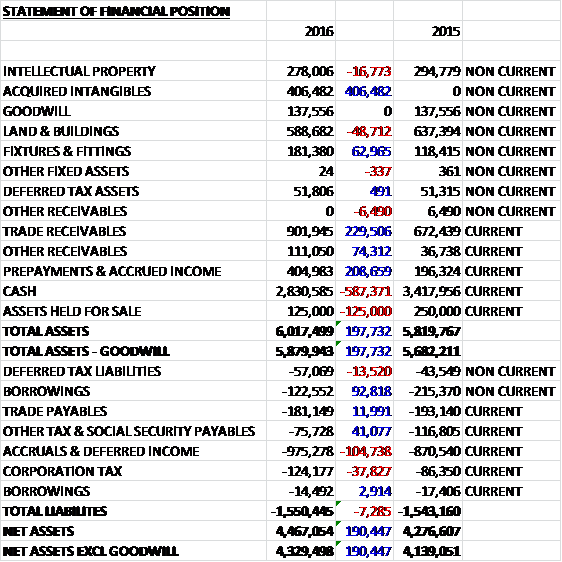

Total assets increased by £198K when compared to the end point of last year driven by a £406K growth in acquired intangibles, a £230K increase in trade receivables and a £209K growth in prepayments and accrued income, partially offset by a £587K reduction in cash and a £125K decline in the value of assets held for sale. Total liabilities were broadly flat as a £96K decline in borrowings was offset by a £105K growth in accruals and deferred income. The end result was a net asset level (excluding goodwill) of £4.3M, a growth of £190K year on year.

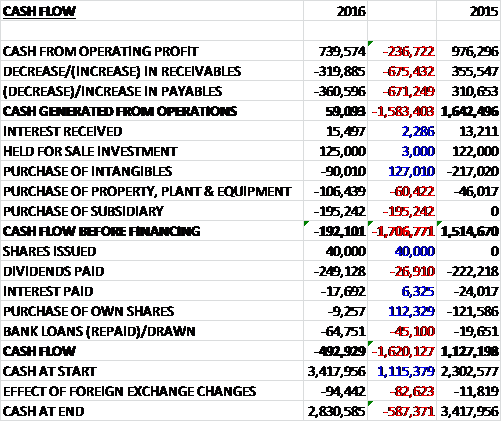

Before movements in working capital, cash profits declined by £237K to £740K. There was a cash outflow from working capital with an increase in receivables and a fall in payables so the net cash from operations came in at just £59K, a decline of £1.6M year on year. The group received £125K from the sale of the latest part of Linx but spent £90K on intangibles, £106K on property, plant & equipment and £195K on acquisitions to give a cash outflow of £192K before financing. The group repaid £65K of bank loans and spent £249K on dividends to give a cash outflow of £493K for the year and a cash level of £2.8M at the year-end.

The gross profit in the Travel Assistance business was £2M, a reduction of £115K year on year due to the loss of the HSBC Premier and Advance books in the UK. This fall has been kept in check by recruiting direct sales staff to focus efforts on building a broader customer base that is less vulnerable to such shocks. Over the last two years the group have made a significant investment in the services to enhance the technical platform, making it both easier to interface with new clients and with new travel data bases. The service now offers travel tracking, e-learning and mobile apps.

The gross profit in the Special Risks business was £1.1M, a fall of £93K when compared to last year as the number of incidents dropped during the year, with the main one being a significant extortion case in the Middle East which ran for three months. The business is now more dependent on incident related revenue than in the past as there has been a reduction in retainer income reflecting the number of insurers underwriting. The Munich office has made a significant contribution to gaining European business and there have been significant client wins for those insurers.

The gross profit in the Consultancy & Response business was £297K, a decrease of £66K when compared to 2015. The year lacked the large evacuation job in Libya which contributed 50% of this division’s revenue. In the current year the largest incident related to the Nepalese earthquake which contributed 24% of revenue and outside these two major incidents, revenue increased by 3%.

The gross profit in the Investigations business was £713K, which represents a maiden contribution from the division and represents nine months of revenue. The RISQ business specialises in employment screening and business investigations – primarily for European businesses with Asian investments. In the first nine months, the division was 11% ahead of budget and the board believe the contribution will grow as the services offered expand the range that can be put to the HR or security purchase holder. Some cross selling has already occurred and this will develop in the coming year.

The gross profit in the Product Safety business was £1M, a growth of £342K year on year. This increase is largely attributable to adding a major provider of insurance in the US and to the start of a business to business product safety service there. Business to business growth is behind board expectations but they are hopeful that the original goals set will be achieved by the end of the year. They have aligned their training in this field with academic institutions so that it becomes possible to achieve a Masters degree and the group have entered into a revenue sharing deal with a university which should benefit 2017, once the course is launched.

This year no customers accounted for more than 10% of revenues compared to two last year but the opening of the office in Germany has played a key part in winning business with Allianz. The group acts as their responder on special risk and product safety and have partnered with their Worldwide Care team to offer clients a combined comprehensive medical and travel risk package which has exciting prospects.

In July 2015 the group acquired RISQ Worldwide, an investigations business based in Singapore. The initial consideration was £259K with a further contingent consideration of up to £826K payable depending on profitability for the three years to 2018.

The group is rather exposed to currency changes. If the Rand appreciated by 10% against Sterling, the cost of operations in South Africa would increase by £150K, but this would be mitigated to some extent by a £100K rise in the value of the office building. As far as RISQ is concerned, if the Singapore dollar were to appreciate by 10% against the US dollar, the cost of operations there would rise by £107K. The group’s exposure to the Euro arises from sales to and purchases from Eurozone countries and is the euro were to depreciate 10% against sterling, profit would be reduced by £65K. Finally, if the US dollar were to depreciate by 10% against sterling, gross profit would reduce by £178K, mitigated somewhat by a £50K reduction in operating costs.

Although there are risks and the market for the group’s services is becoming ever more competitive, the board are encouraged by the way they have continued to progress over the year and are excited about the growth prospects offered by their European partners, Allianz, the US product safety business, cross selling RISQ services and potential further acquisitions.

At the current share price the shares are trading on a PE ratio of 16.5 which falls to 7.1 on next year’s consensus forecast. After an 11% increase in the final dividend the shares are yielding 3.4% which increases to 3.7% on next year’s forecast.

Overall then this has been a bit of a mixed year for the group. Profits declined but this can be attributed to adverse forex movements and the effect of acquisitions and it could be argued that underlying profits were up slightly. Net assets increased but the operating cash flow was down and rather disappointing with no free cash being generated, not helped by an adverse movement in working capital.

The travel assistance business saw profits fall due to the loss of the HSBC contract, although the decline wasn’t that bad considering. The special risk and consultancy & response business both also saw falls in profits due to a lower number of incidents with the latter not seeing a repeat of the Libyan evacuation that occurred last year. The product safety business saw profits increase due to the new insurance client in the US and the Investigations business contributed a useful maiden profit showing the acquisition to be a rather good one.

Things are a little uncertain here and the susceptibility to forex movements is a bit of a worry but a forward PE ratio of 7.1 and dividend yield of 3.7% look to have priced these concerns in – I continue to hold.

On the 1st August the group announced that it was in discussions with iJet which could lead to an offer being made for the Red24. These are at a preliminary stage so far and iJet has until the 29th August to make a firm offer. IJet later confirmed that the price being discussed is 24p per share. This obviously caused a jump in the share price but I still think it undervalues the group.

On the 26th August the group announced that discussions with iJET have moved ahead constructively and continue to do so. Following negotiation, they increased the indicative price of the possible offer from 24p per share to 26p. The deadline has now been extended so we have until the 26th September to see a bit emerges. I am holding on here given the price is below this level.