Begbies Traynor has now released their final results for the year ended 2016.

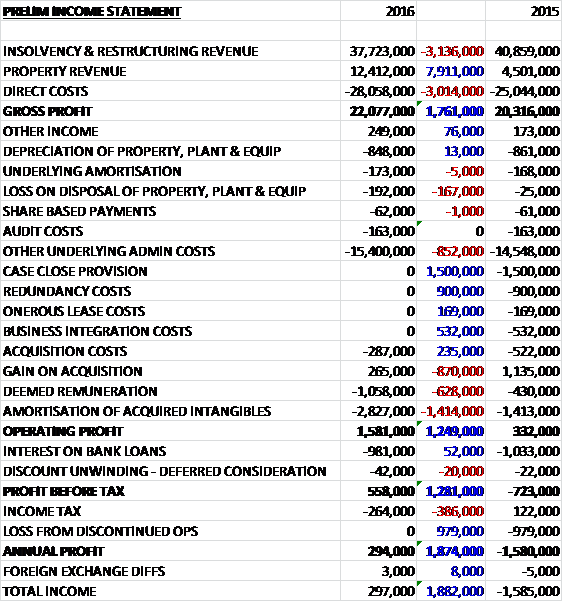

Revenues increased when compared to last year as a £3.1M decline in insolvency revenue was more than offset by a £7.9M growth in property revenue reflecting the full year benefit of the Edisons and Taylors acquisitions, and after direct costs grew by £3M the gross profit increased by £1.8M. Other income was up £76K but there was a £167K increase in losses on disposal of property, plant and equipment and other underlying costs were up £852K. There was a £3.1M decline in one-off costs and acquisition costs fell by £235K but the gain on acquisition was £870K lower, deemed remuneration was up £628K and the amortisation of acquired intangibles increased by £1.4M to give an operating profit £1.2M above that of last time. Bank interest came down slightly and there was no loss from discontinued operations which accounted for nearly £1M last year, although tax was up £386K. The end result was a profit of £294K, a positive movement of £1.9M year on year.

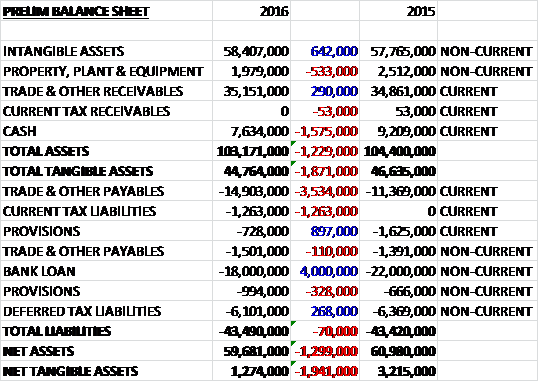

When compared to the end point of last year, total assets declined by £1.2M driven by a £1.6M fall in cash and a £533K decrease in the value of property, plant and equipment, partially offset by a £642K growth in intangible assets and a £290K increase in receivables. Total liabilities were broadly flat during the year as a £3.6M growth in payables reflecting increases in both accruals and other payables, and a £1.3M increase in current tax liabilities were offset by a £4M decline in the bank loan and a £569K fall in provisions. The end result is a net tangible asset level of £1.3M, a decline of £1.9M year on year.

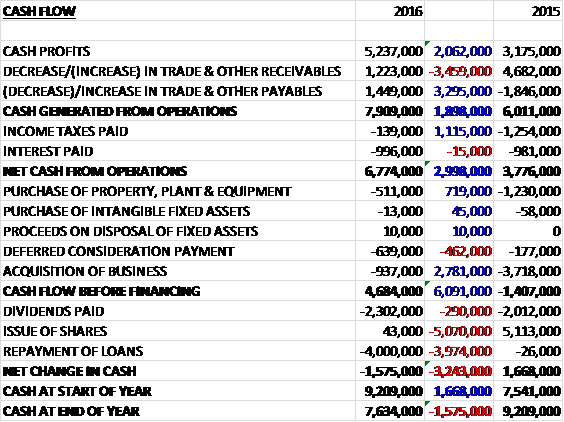

Before movements in working capital, cash profits increased by £2.1M to £5.2M. There was a cash inflow from working capital, although this was slightly lower than last year but after tax payments declined by £1.1M to give a net cash from operations of £6.8M, a growth of £3M year on year. The group then spent £511K on property, plant & equipment; £639K on deferred consideration and £937K on acquisitions which gave a free cash flow of £4.7M. They spent £2.3M of this on dividends and £4M on loan repayments which meant that the cash outflow for the year was £1.6M and the cash level at the year-end was £7.6M.

Overall, results were in line with expectations. The number of corporate insolvencies totalled 14,370, representing a 9% year on year reduction. This is the lowest level since 2004, although the numbers appear to have stabilised at this level over the last twelve months. The number of insolvencies in Q1 have increased by 8% on Q4 but have fallen 7% when compared to Q1 2015.

The profit in the insolvency and restructuring business was £7.5M, a decline of £1M year on year as a results of the reduction in revenue. The insolvency market remains very challenging with the further reduction in UK corporate insolvency appointments over the last year, compounding the impact of reductions over recent years. The group have maintained their market leading position, however, as the largest corporate appointment taker by volume.

The lower level of market activity impacted revenue levels which have only been partially mitigated through continued cost control with operating margins down from 20.8% to 19.8% with £1.5M additional costs in relation to acquired businesses being more than offset by cost savings of £3.6M. The number of people employed in the division reduced by 15 during the year due to a continued alignment of the cost base with current market conditions.

The profit in the property business was £2.4M, a growth of £1.7M when compared to last year representing the first full year of contribution from the division after 2015 only saw five months-worth. The pro-forma results saw a 26% rise in profit with operating margins increasing from 15.3% to 19.4%. Taylors, acquired in November 2015, contributed £100K of the profit in the period.

During the year the business exited a number of non-profitable and low margin engagement which contributed to the overall improvement in operating margins, whilst reducing revenue by £400K. In addition, revenue generated insolvency appointments, principally fixed charge property receiverships, reduced in the year by £800K, reflecting the overall marketplace. The profit impact of these reductions has been offset by additional income from one-off consultancy projects of £500K together with cost reductions of £1.1M. The group have delivered £1M of annualised savings since the Eddisons acquisition, exceeding the initial target of £500K.

The Eddisons team are now being appointed on the majority of the group’s insolvency cases where agents are required which has offset the reduced appointments from the overall market place. The number of people employed in the division has fallen by 28 during the year.

In November 2015 the group acquired the Taylors valuation practice for an initial consideration of £1.1M, satisfied in cash of £500K and through the issue of 1,389,661 new shares with additional contingent consideration of up to £750K payable over the next five years, to be issued in shares. The business specialises in providing commercial business and property valuations for secured lending purposes on a nationwide basis on behalf of a wide range of financial institutions, including all of the major high street banks. The business has been integrated into the existing valuations team, strengthening the combined offering to lenders and it has performed in line with expectations in the period following the acquisition.

In June, after the year-end, the group acquired Pugh & Co. The business is the largest firm of commercial property auctioneers operating outside of London. They hold regular auctions in Leeds and Manchester which complement the Eddisons auctions business which will become the third largest firm of commercial property auctioneers nationally.

In September 2015 the group acquired the assets of Sheffield based P&A insolvency practice out of administration for a cash consideration of £700K, of which £400K was paid on completion and the balance of £300K in the year following the acquisition along with a further contingent consideration of £200K.

Although the board remain cautious about activity levels in their counter-cyclical activities in both business recovery and property services in the near term, the recent acquisition of the Pugh auction business together with the Taylors valuation business gives the opportunity for growth in earnings over the coming year.

At the current share price the shares are trading on a massive PE ratio of 172 as I have included the acquisition costs and amortisation, I can’t find a current forecast. After the final dividend was kept the same, the shares are yielding 4.6%. At the year-end, the net debt position was £10.4M compared to £12.8M at the end of the prior year.

Overall then this has been a mixed year for the group. They are now profitable but whether this is an improvement on last year depends on your treatment of what are underlying costs. The improvement is due to the fact that last year’s redundancy costs and case close provisions were not repeated this year, although costs associated with acquisitions increased this year. If we include the amortisation of acquired intangibles (as I feel we should) then the performance deteriorated year on year. Net tangible assets also fell and are looking rather precarious but the operating cash flow improved and the group generated a decent amount of free cash flow.

The insolvency division saw profits decline due to the continued low levels of corporate insolvencies but the property business saw profits increase due to prior acquisitions, cost cutting and a large one-off consultancy project. The dividend yield of 4.6% looks promising but I am a little concerned over some of the other issues here and this, combined with the high levels of debt mean that I am not going to cover this company again until the situation improves.

On the 20th January the group announced that regional managing partner Julie Palmer sold 22,210 shares at a value of £11K. Not a huge amount but unwelcome nonetheless.

On the 7th March the group released a trading update covering Q3. The expectations for the year as a whole remain unchanged. They have seen an improvement in activity levels in the insolvency business in the quarter which leaves them well placed for a strong final quarter albeit the work in progress in both the insolvency and property services business includes a number of engagements with fees contingent on completion before the year-end. This sounds a bit nervous to me and I wonder whether some of those revenues might slip into next year.

On the 10th April the group announced that two regional managing partners sold 39,878 shares between them at a value of £19,141.

On the 25th April the group announced that Head of Business Recovery and Advisory Mark Fry sold 16,444 shares at a value of £11K.