Newmark Security has now released its final results for the year ended 2016.

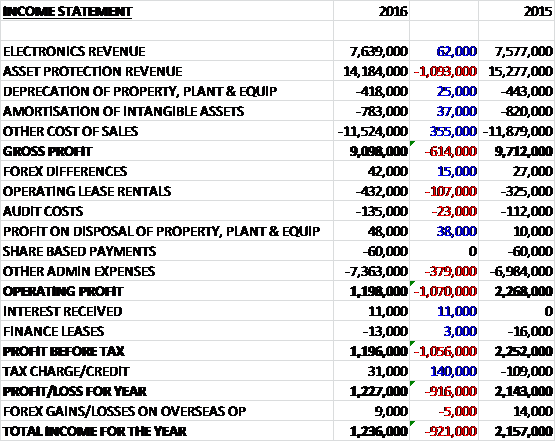

Overall revenues declined when compared to last year as despite flat electronics revenue, asset protection revenue decreased by £1.1M. Cost of sales were also down but the gross profit fell by £614K. Operating lease rentals grew by £107K and other admin costs also increased which meant that the operating profit declined by £1.1M. After finance costs were broadly similar to last year and there was a £140K positive swing to tax credits in 2016 due to tax losses brought forward, R&D allowances and the lower future UK tax rate reducing the deferred tax balance, the profit for the year came in at £1.2M, a decline of £916K year on year.

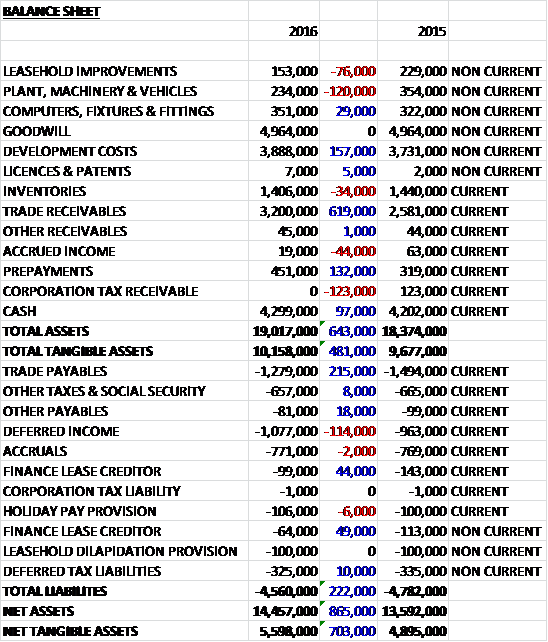

When compared to the end point of last year, total assets increased by £643K to £19M, driven by a £619Km growth in trade receivables, a £157K increase in development costs and a £132K growth in prepayments, partially offset by a £123K reduction in corporation tax receivable and a £120K fall in plant, machinery and vehicles. Total liabilities declined during the year as a £114K growth in deferred income was more than offset by a £215K fall in trade payables. The end result was a net tangible asset level of £5.6M, a growth of £703K year on year.

Before movements in working capital, cash profits declined by £1.1M to £2.4M. There was also an outflow from of cash from working capital compared to an inflow last year, mainly as a result in a growth in receivables due to the timing of sales in the months approaching the year-end, but there was a £300K positive swing in tax receipts so that the net cash from operations was £1.8M, a decrease of £2.8M year on year. The group spent £205K on property, plant and equipment along with £945K on development costs so that there was free cash flow of £649K. Of this, £182K was used to repay finance leases and £460K was paid out in dividends to give a cash flow for the year of just £96K and a cash level of £4.3M at the year-end.

The loss in the Electronic business was £452K, a detrimental movement of £500K year on year. Access Control saw a 6% growth in revenues with a clear divergence in sales of the JANUS and SATEON product lines. This was due to Microsoft’s discontinued support for the 32-bit and earlier operating systems which adversely affects the 16-bit operating system that JANUS runs on so revenues from the product continued to decline.

SATEON Pro and SATEON Enterprise both saw significant increases in revenue during the year and revenues were further bolstered by the trend for clients to migrate from JANUS to SATEON platforms. As legacy hardware can be used with SATEON there is no need to rewire a site when upgrading and end users can benefit from future-proofing without significant capex requirements. Technical and marketing tools have been developed and released to drive an upsell campaign and as a result a healthy pipeline of upgrade opportunities has been developed.

During the year SATEON version 2.9 was released which enabled on site facial recognition and verification along with further integrations. Integrations into SALTO and Aperio wireless locks launches SATEON into the wireless market and increases the chances of winning large hotel and education projects. This has been achieved by reducing the cost associated with hard-wired projects, allowing integrators to install systems into a large number of doors in a shorter amount of time.

Version 2.10 was launched in June 2016 and offers new installer and advanced search features which will streamline the management of the system. Overseas, SATEON was adopted by a major cruise line in the US with further revenues expected during this year as the roll out continues. Projects and pipeline continue to grow in the Middle East and it is expected that headcount will be increased locally to support sales. During the year a sales office was opened in Hong Kong which increased overheads.

Workforce Management revenues declined by 5.4% in the year with revenues in the UK business falling by nearly 10%, largely as a result of a decline in sales in the RS series of legacy hardware and the natural slowdown of the rollout across the estate of a large apparel retailer. New partners in the UK, US and Australia came on stream in the year and it is expected that revenues will increase as these channels begin to resell the Grosvenor proposition.

The group have scaled up their US sales and marketing resources, a new website has been launched and a number of business development activities are underway to leverage the position in the US market and attract new channel partners across North America.

The profit in the Asset Protection business was £2.8M, a decline of £568K when compared to last year. Revenues in the product division declined by 12.1% due to the forecast decline of the Post Office programme for installation of time delay cash handling equipment. Revenue from new Eclipse rising screens and screen reconfiguration work fell by 36% after the branch refurbishment programme for a long-term customer was completed during the year. Counter Shield revenue increased by nearly 45% as a result of a substantial order received from a Local Authority in London. Despite the declining Post Office contract, revenues of cash handling products to high street financial institutions increased by 71.5%.

Revenues of fixed glazing and counter protections systems increased by 45% and revenue for secure doors increased by 55% as a result of a large branch refurb programme by a long standing customer in the financial sector. Revenue for secure walling systems, however, decreased by 58% after a major supermarket chain cancelled plans to open new stores. Revenue for other non-standard products decreased by 43% after a branch closure programme by a large financial institution was suspended but export revenues increased significantly after receiving an order for 25 ballistic doors for a hotel project in Iraq.

Recertification of ballistic resistant products is planned for the current year and this will enable the group to be more competitive in local as well as international markets. Additional successful blast product testing was undertaken at the Government’s Centre for the Protection of National Interest in June 2016.

Revenue in the Service division was the highest in five years with an increase of 12% year on year. This was the result of pneumatic upgrade work on rising screens that have provided security to many financial institutions for over 25 years. The group still see an appetite to retain these systems with the benefit and safeguards they provide to staff in robbery situations. They continue to explore other revenue streams and whilst initial growth may be slow, they see cost benefits in clients using their multifaceted services. They are confident that they will be able to offer these broader services nationally over the next few years. The group have invested in improved IT over the last year and they anticipate a fall in admin costs whilst revenue capture systems improve.

Following the Brexit vote the group could be affected by a lack of confidence in the economy by their customers in the UK, potentially leading to delays in spending, but the benefit to exports should outweigh additional material cost of imports but overall it is too early to forecast the impact.

The operating profit for the current year will be significantly lower than last year. This reflected the fact the strategy of material investment in new products, new customer acquisition and new geographies has taken longer to be realised than originally expected. The opportunity pipeline continues to grow but the conversion into sales has been slower than hoped. A number of new products are to be launched during the current year including the SATEON advanced range and a new Android based terminal for workforce management, which the board are optimistic will resonate with potential customers.

At the current share price the shares are trading on a PE ratio of 9.3 which increases to 23.3 on next year’s consensus forecast. After the final dividend was kept the same, the shares are trading on a yield of 4.3% which is predicted to remain the same next year. Net cash increased from £3.95M to £4.14M.

Overall then this was a pretty difficult year for the group. Although net assets improved, profits declined and the operating cash flow reduced. Although they are still generating some free cash flow. The Electronic division is now loss-making, driven by reduction in workforce management sales as the roll-out to a large client slowed down. Asset protection profits declined in the year as the post office contract came to an end. It does seem as though the group is very susceptible to client refurb cycles so earnings are somewhat up and down.

In the coming year, profits are likely to be even lower with the forward PE predicted to be 23.3. The yield is likely to remain the same, at 4.3% but times are not easy at the moment and I am staying out for now.

On the 22nd September the group announced a trading update. Due to delays to the conversion of the opportunity pipeline and other operational difficulties, they now expect results for the current year to be materially below market expectations and they expect to report a loss for 2017.

Historically revenue in the asset protection business has varied substantially from one year to the next due to the timing of major refurbishment programmes in this financial year. The revenue stream within this division during the last few years has included substantial sales of cash handling equipment to the Post Office as part of their Network Transformation Programme. This revenue stream was expected to reduce during 2017 and the group has been seeking to replace it by broadening their product range.

Despite being appointed as UK distributor of a leading manufacturer’s doors and partitions range, new orders and sales have been considerably slower than anticipated in the first four months of this year and the pipeline and outlook for the rest of the year is not sufficient for the board to have confidence the recent slowdown will be reversed in the immediate future.

In the Electronic Division, sales of JANUS continue to decline year on year whilst SATEON revenues are increasing. SATEON revenues have nearly doubled compared with the same period last year but this has been offset by the decline in JANUS revenue. Whilst sales of SATEON enterprise level projects have outperformed expectations, penetration of the high volume mid tier market has been limited, partly due to a delayed release of the new variant SATEON. Significant revenues from this new release are now not anticipated until next year. In addition, some national systems integrators, key clients of the division, have recently issued profit warnings as projects have been delayed or postponed post-Brexit.

Workforce management sales in the UK have remained flat following the completion of the programmes in the last two financial years of roll out programmes for an apparel retailer and supermarket chain.

Further afield, performance in the Asia Pacific region continues to disappoint as the Hong Kong office tries to establish sales and distribution channels and conduct business development activities. The US office has shown 8% growth in workforce management revenue, however, which is in line with expectations. Focus remains on growing both existing customers share of wallet and establishing new channel partners, as the group prepares to launch a new Android-based WFM terminal next month.

This is a pretty dire profit warning and I am not touching this for now.