Martin & Co has now released its interim results for the year ending 2016.

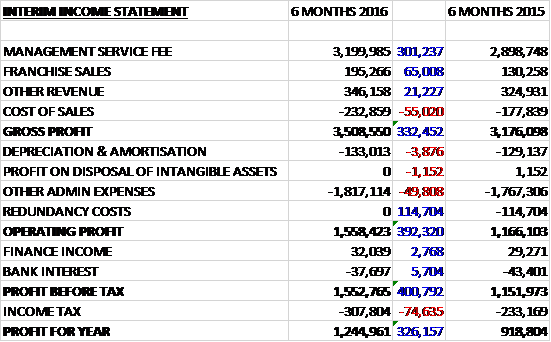

Revenues increased when compared to the first half of last year due to a £301K growth in management service fees, a £65K increase in franchise sales and a £21K growth in other revenue. Cost of sales increased modestly which meant that gross profit increased by £332K. Admin expenses increased by £51K but there were no redundancy costs that accounted for £115K last time to give an operating profit £392K ahead. Bank interest fell slightly but tax costs increased by £75K which meant that the profit for the period came in at £1.2M, a growth of £326K year on year.

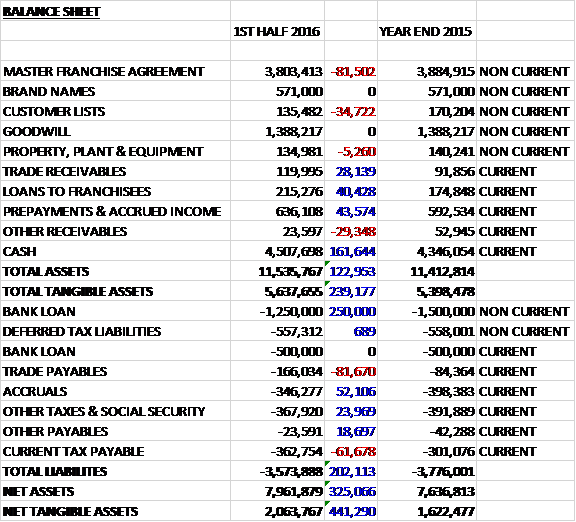

When compared to the end point of last year, total assets increased by £123K to £11.5M driven by a £162K increase in cash, a £40K growth in loans to franchisees and a £44K increase in prepayments and accrued income, partially offset by an £81.5K decline in the master franchise agreement. Total liabilities declined during the period as an £81.7K growth in trade payables and a £61.7K increase in current tax payables was more than offset by a £250K decrease in the bank loan. The end result was a net tangible asset level of £2M, a growth of £441K over the past six months.

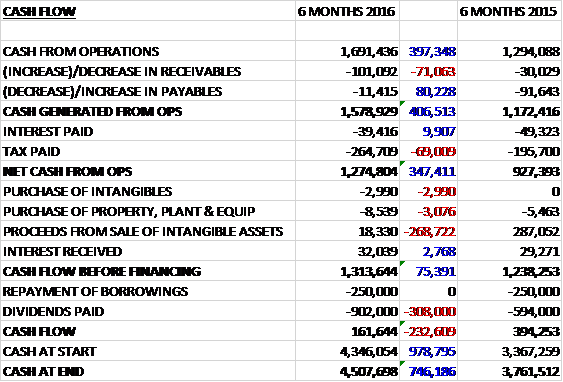

Before movements in working capital, cash profits increased by £397K to £1.7M. There was a cash outflow from working capital, although this was broadly similar to last year but tax payments increased by 69K to give a net cash from operations of £1.3M, an increase of £347K year on year. There was very little in the way of capex, indeed the group actually made more from asset sales than from purchases so there was a free cash flow of £1.3M. Of this, £250K was used to pay back loans and £902K was spent on dividends to give a cash flow of £161K for the period and a cash level of £4.5M at the end of the half.

Market conditions became challenging as the Brexit vote approached but, whilst uncertainty remains, there are now signs of recovery in lettings transactions. Estate agency activity is mildly depressed in London and the South compared to last year but activity in the Midlands and North remains in line with budgetary expectations.

Management service fees from lettings continued to grow steadily at 7% whilst management service fees from sales, driven by the stamp duty change in April and no general election, increased by 24%. The Brexit vote has had a dampening effect on house transactions whilst lettings appear to be recovering from a short lived downturn. Significant uncertainty still remains in the sector following the vote.

The integration of two property franchisors and the associated four property brands acquired as Xperience is now complete. In September, after the period-end, the group acquired EweMove for a total consideration of up to £15M. They paid £5M in cash on completion, drawing down £2M from their facility with Santander, and issued £3M of new shares to the owners. Up to a further £7M of deferred payment may be payable after the financial statements for 2018 are approved by the board, dependent on performance criteria linked to EBITDA for the enlarged group. This can be paid in cash or by the issue of new shares at the company’s discretion.

EweMove is an online estate and letting agent with 85 active franchisees as of the period-end. The agency operates a scalable central technology platform and operational hub to support local property experts/franchisees. The directors believe that there is capacity in the UK market for substantial growth in the number of local property experts. The business is now generating cash and future growth should be self-funding (current pre-tax profit is £120K). It will continue to operate from its own HQ in Yorkshire to preserve the brand identity and the two founders have taken up senior positions within MartinCo to improve online marketing and technology capacility across all brands.

Going forward, considering the current momentum the board remains confident of future progress and trading results for the full year.

At the current share price the shares are trading on a PE ratio of 18 which reduces to 13.6 on the full year forecast. After an 11% increase in the interim dividend, the shares are yielding 3.6% which increases to 4% on the full year forecast. At the end of the period the group had a net cash position of £4.5M compared to £3.8M at the same point of last year but obviously that changed following the acquisition after the period-end.

Overall then this was a very strong set of results from the group. Profit increased, net assets grew and operating cash flow was up on last time, with a decent amount of free cash flow generated. Unfortunately there are two events that change things somewhat, the Brexit vote supressed demand around that period and although lettings seem to have recovered, estate agency sales are still subdued. Also, the acquisition, although seemingly a shrewd move, does increase risk somewhat. This is a tricky one, I am minded to think that the forward PE of 13.6 and yield of 4% looks about right.

On the 2nd February the group released a trading update covering the whole year. Revenue increased by 15% to £8.2M and current trading is in line with expectations. Trading performance in the final months of 2016 was robust despite challenging market conditions during the immediate aftermath of the Brexit vote. This performance has been driven by organic growth in Management Services Fees, an expanding network of franchises and tight cost control measures.

EweMove made a modest contribution to group EBITDA with 96 franchisees at the year-end. It is currently targeting experienced estate agents and business proprietors as potential franchise recruits to rapidly expand its network in 2017. The group is also importing some of the intellectual capital of the business into its five traditional high street brands, and will be launching new websites with a facility for customers to book valuation appointments in real time.

There is no timetable for the implementation of the government’s proposal to ban or restrict the charging of fees to tenants in England. A total tenant fee ban in Scotland was successfully overcome by the group, winning market share at the expense of smaller lettings business, many of whom withdrew from the market.

The board do not envisage the government’s recent interventions in the buy to let sector significantly impacting their business. Early indications show that investors are beginning to incorporate their activities into trading companies to avoid the stamp duty surcharge and to retain the benefit of interest tax relieve on buy to let loans. The board remain positive about the outlook for their core lettings business and all of this sounds quite good to me.

On the 23rd February the group announced that they are changing their name to the Property Franchise Group which sounds very generic!

On the 16th March the group announced that it had changed its name to The Property Franchise Group. Great. That’s probably the most generic name I have ever seen!