Ricardo has now released its final results for the year ended 2016.

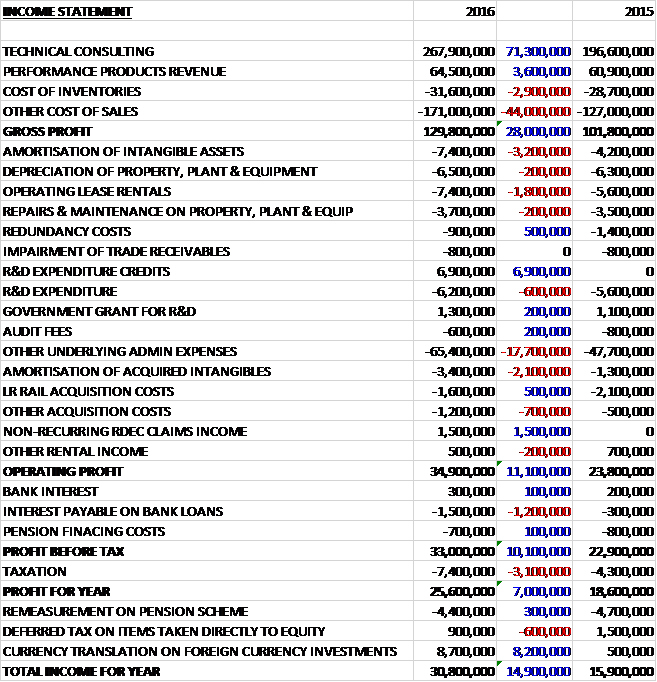

Revenues increased when compared to last year with a £71.3M growth in technical consulting and a £3.6M increase in performance products, mainly attributable to acquisitions with organic revenue up 7%. Cost of sales also grew which gave a gross profit £28M above that of last year. Amortisation increased by £3.2M, operating lease rentals were up £1.8M and other underlying admin expenses increased by £17.7M but there was a £6.9M R&D expenditure credit. The amortisation of acquired intangibles was up £2.1M but there was a £1.5M in non-recurring RDEC claims income to give an operating profit £11.1M higher. Interest cost increased by £1.2M and tax charges grew by £3.1M, partially relating to the new R&D tax rules, which meant that the profit for the year came in at £25.6M, a growth of £7M year on year.

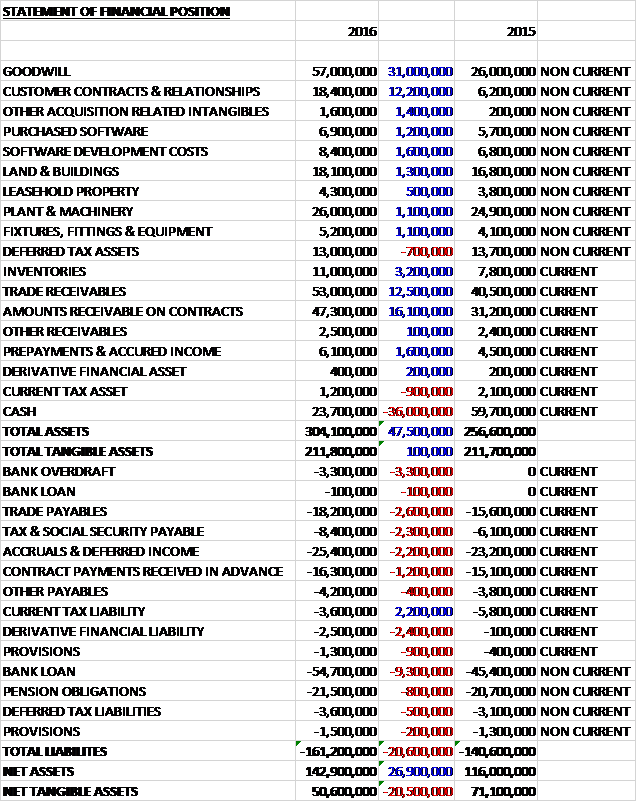

When compared to the end point of last year, total assets increased by £47.5M to £304.1M driven by a £31M growth in goodwill, a £16.1M increase in amounts receivable on contracts, a £12.5M growth in trade receivables, a £12.2M increase in customer contracts & relationships and a £3.2M growth in inventories, partially offset by a £36M reduction in cash. Total liabilities also increased during the year due to a £9.3M increase in bank loans and a £3.3M growth in bank overdrafts along with some smaller increases. The end result is a net tangible asset level of £50.6M, a decline of £20.5M year on year.

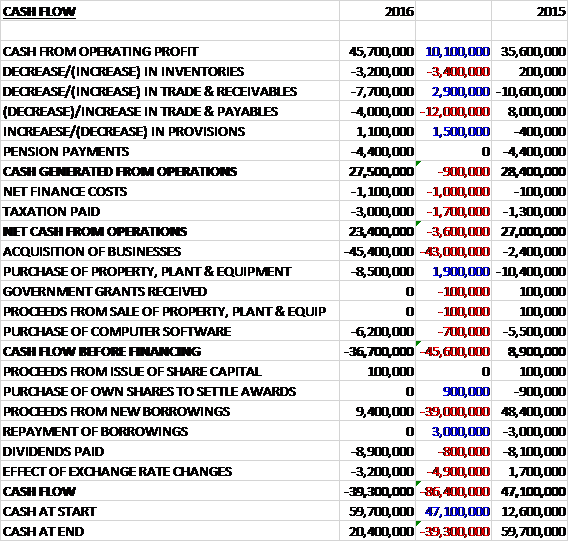

Before movements in working capital, cash profits increased by £10.1M to £45.7M. There was a cash outflow from working capital and this was larger than last year so after finance costs grew by £1M and tax was up £1.7M, the net cash from operations came in at £23.4M, a decline of £3.6M year on year. This covered the £8.5M of fixed asset purchases and £6.2M in computer software but not the £45.4M spent on acquisitions so there was a cash outflow of £36.7M before financing. The group took out £9.4M of new borrowings which covered the £8.9M paid out in dividends so the cash outflow for the year was £39.3M to give a cash level of £20.4M at the year-end.

The operating profit in the technical consulting division was £28.1M, a growth of £9.3M year on year, of which £3.9M was attributable to Lloyd’s Register Rail and £600K to Cascade. The European Technical Consulting division was a key driver of growth, with profits growing significantly as a result of an internal reorganisation undertaken in the prior year to improve co-ordination and delivery to clients, as well as to achieve cost efficiencies. The division secured a range of large, multi-year programmes in the automotive, commercial vehicles and energy sectors with a particular increase in vehicle electrification activities in many regions. Activity levels have been high across all engineering disciplines with increasing demand for powertrain application, calibration, electrical and electronics skills.

The rail business has performed well with a number of successful joint bids with the core business. They have established a new brand and have seen a positive reaction to the new products and services they can offer. In July, following the award of UKAS accreditation, they established Ricardo Certification, a business that will independently manage and deliver the assurance and accreditation services to the Rail sector.

The performance of the US business has struggled in challenging market conditions with reduced levels of work in Detroit and Chicago, partially offset by increasing work in California. The business is increasingly focused on achieving growth in the commercial vehicles sector, especially around platooning technologies and the growth of autonomous vehicle and connected car technologies in both the traditional automotive and new entrant landscape. Ricardo Defence Systems was established in the previous year to enable the group to deliver classified projects for the US Defence Administration, and this business has won a number of new contracts, primarily in the land defence business.

China remains a key market and the group have secured a number of large, locally won contracts, some of which are being locally delivered through the Shanghai and Beijing based technical centres. These contracts have included a mixture of hybrid vehicle, engine, transmission and rail activities. In the motorcycle business the business has been on the delivery of existing large, multi-year powertrain and vehicle programmes and the global roll-out of an expanded product and services offering to existing and new clients. As a result they have secured a number of contracts with new clients in the UK, US and Asia. They are also developing their urban mobility product offering.

The energy and environment consulting business has performed well, reducing its reliance on the UK public sector where ongoing cuts continue to be experienced. In Asia the business continues to grow its activities, establishing a greater geographical footprint through the acquisition of the rail business in China. The strategic consulting activities continue to make progress.

The operating profit in the Performance Products division was £7.3M, a decline of £400K when compared to last year due to lower one-off software license sales and an expected reduced level of shipments of high performance and monorail transmissions this year, partially offset by increased volumes in respect of the new engine supply contract for McLaren. The order intake in the year stood at £103M compared to £43M as they secured a high profile multi-year transmission supply contract.

The expansion of the engine build facility is now complete. This gives a doubling of capacity and the capability to deal with increased engine variants. Production of engines for the McLAren 650S, 675LT and the P1 supercar continues in line with expectations, and full production of engines for the 570S has been added. The group remains a key supplier to the motorsport sector, having started deliveries for BMW and Multimac GT3 programmes and for the Hyundai R5 Rally programme. They continue to manufacture for Formula 1, and supply products such as the transmissions for the Japanese Super Formula 14, Indy Lights and the Renault World Series. Production also continues for the Porsche Cup and Bugatti transmissions in line with long term supply agreements. As part of a teaming agreement with a defence Tier 1 business, the group has developed and provided retrofit kits for the Cougar family of vehicles for the UK MOD.

The year ended with another record closing order book of £231M compared to £140M last year, with £66M of that in respect of the two acquired businesses. On a like for like basis, the closing order book has increased by 18%.

On the 1st July 2015 the group completed the acquisition of Lloyd’s Register Rail, a rail consultancy and assurance business. They provide services ranging from rolling stock design, signalling and train control, intelligent rail systems, operational efficiency improvements, training and independent assurance services. The acquisition cost £46.3M in cash and generated goodwill of £24.2M. Since the date of acquisition, the business has contributed £3.9M in underlying operating profit.

In August the group acquired Cascade Consulting for a total cash consideration of £3.2M which included goodwill of £2.5M. The business is an environmental consultancy business specialising in the UK water sector which provides additional capability and reach in water resource management, ecosystem services and environmental impact assessment. Since acquisition it has contributed £600K to the underlying operating profit of the group.

After the year-end the group acquired Motorcycle Engineering Italia for an initial cash consideration of £2.1M. The business was formed from the operating assets and employees of Exnovo, a vehicle design house. The acquisition generate goodwill of £2.1M.

The average value of Sterling was 1.9% higher against the Euro, 5.9% lower against the US dollar and 1.5% lower against the Chinese Renminbi during the year but significant exposures are hedged through forex contracts. The movement in forex rates and the impact on performance was more significant as a result of the Brexit vote but these movements have only impacted upon the final week of the year.

The new R&D Expenditure Credit (RDEC) became mandatory from April and the group adopted RDEC from July 2015. Under the new regime, the current year R&D credit is no longer a tax incentive that benefits the corporation tax line in the income statement but is instead treated as grant income to offset R&D expenditure within operating profit, increasing pre-tax profit, the associated tax charge and the effective rate of tax. In addition, applications have been revised during the current year in respect of 2014 and 2015 which were open under the new RDEC regime, generating £1.5M of non0recurring income.

Going forward, market conditions remain positive. The group has European operations which will continue to support the EU’s R&D programmes and deliver to their European clients close to their operations, as before. They enter the new financial year with a record order book and a good pipeline of opportunities across all sectors. Taking this together with the long term assembly contracts, the board continue to have confidence in the further development of the group.

At the current share price the shares trade on a PE ratio of 20.5 which increases to 26 on next year’s consensus forecast which looks very expensive. After a 9% increase in the full year dividend, the shares are yielding 1.9% which falls to 1.6% on next year’s forecast. The group has a net debt position of £34.4M as of the year end compared to a net cash position of £14.3M at the end of last year.

Overall then this has been a fairly good year for the group. Profits have increased, both organically and through the contribution from acquisitions and whilst the operating cash flow declined, this was due to working capital movements with cash profits growing. The net tangible asset level did take a battering, however. The technical consulting business is growing well with the European division being the driver due to cost controls and some decent new projects driven by the drive for vehicle electrification. The US division fared less well, however, due to a tough market.

The performance products business saw profits decline due to lower software sales and a reduction in high performance and monorail transmissions. There was a large order intake, however, and the business for McLaren seems to be ramping up. The forward PE of 26 and yield of 1.6% seems to have baked this good news in, however, so I am just holding for now (although I am not sure how accurate these figures are given the ridiculous rules surrounding private investors and access to broker forecasts).

On the 7th October the group announced that MD Mark Barge sold 2,045 shares at a value of £20K. O the 10th October he sold another 1,153 shares at a value of £12K. He now owns just 911 shares in the company.