AG Barr has now released its interim results for the year ending 2017.

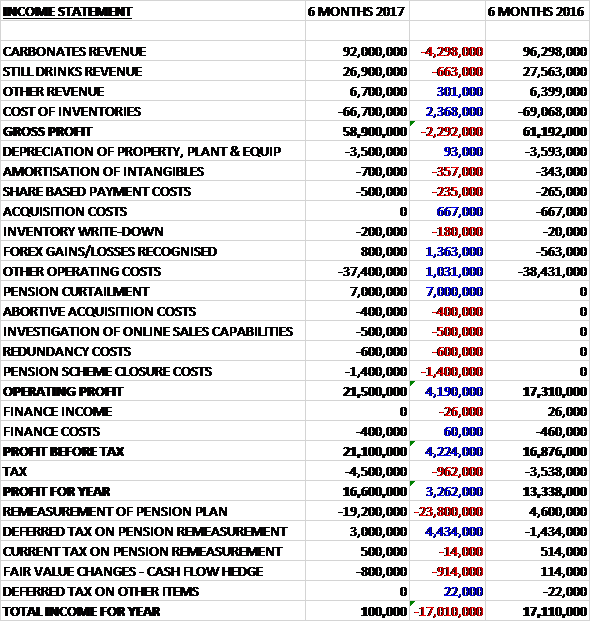

Revenues declined when compared to the first half of last year with a £4.3M reduction in carbonates revenue and a £663K fall in still drinks revenue with other revenue up £301K. Cost of sales also declined to give a gross profit £2.3M below that of last time. Amortisation payments increased by £357K and there was a £235K growth in share based payments but acquisition costs were down £667K, there was a £1.4M positive swing from forex movements and other operating costs declined by £1M. We also see a net £5.6M gain from the pension closure but £400K costs due to an abortive acquisition, a £500K charge relating to the investigation of online sales capabilities and a £600K redundancy cost. All this meant that the operating profit grew by £4.2M and after tax charges grew, the profit for the period came in at £16.6M, a growth of £3.3M year on year.

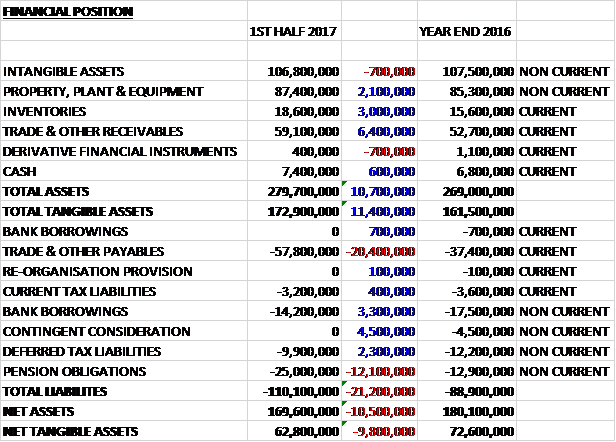

When compared to the end point of last year, total assets increased by £10.7M to £279.7M driven by a £6.4M growth in receivables, a £3M increase in inventories and a £2.1M hike in property, plant and equipment. Total liabilities also increased during the period as a £20.4M growth in payables and a £12.1M increase in pension obligations were only partially offset by a £4M reduction in bank borrowings, a £4.5M fall in contingent payments and a £2.3M decrease in deferred tax liabilities. The end result was a net tangible asset level of £62.8M, a decline of £9.8M over the period and I would like to understand the cause of the payables increase.

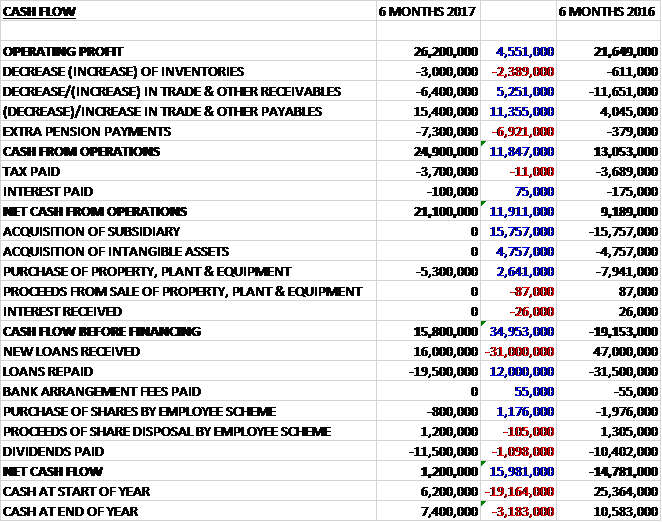

Before movements in working capital, cash profits increased by £4.6M to £26.2M. There was a small cash inflow from working capital, a reversal of last year’s situation, but there was a £7.3M extra pension payment. Nevertheless, net cash from operations came in at £21.1M, a growth of £11.9M year on year. The group only spent £5.3M on capex so the free cash flow was a healthy-looking £15.8M which covered the £11.5M paid out in dividends along with some debt repayments so the cash flow for the period was £1.2M and the cash level at the end of the half year was £7.4M.

The gross profit in the Carbonates division was £47.9M, a decline of £2.3M year on year and the gross profit in the still drinks business was £7.5M, a reduction of £700K when compared to the first half of 2016.

The soft drinks market in the period was down 0.7% in value and 0.4% in volume reflecting a deflationary market with increased promotional activity. The stills market was flat in revenue terms but bolstered in volume terms by a 7% growth in water so overall volume was up 1.5%. Carbonates were down 2.4% in volume and nearly 1% in value. Deflation levelled out from its previous position and it is expected that the current period of food and drink deflation could reverse next year.

While maintaining overall market share, the group have seen the impact of changing consumer preferences. In line with general market trends, lower and no sugar products have performed better. Irn-Bru Xtra and Rubicon Spring, both of which contain no added sugar, are performing well at this early stage and the board expect these new introductions to the portfolio to make a material contribution to the business across the balance of the year.

The gross profit in the other business, including Funkin cocktail solutions, rental income from vending machines and the sale of ice cream, was £3.5M, a growth of £700K year on year. The Funkin business performed strongly with 28% revenue growth driven by distribution gains in the UK and US, a successful innovation pipeline and investment in new digital platforms.

The international business has delivered a credible performance with revenue up 16%. The board expect this momentum to continue, supported by a further territory extension agreement with Rockstar signed in September, covering Russia and a number of Central Eastern European countries. Margins in the period have been supported by ongoing cost control actions and the impact of longer term structural cost reduction and capital investment, all factors that are expected to have a positive impact on margin over the full year.

As can be seen there were a number of “non-underlying” costs during the period. There was £500K of advisory costs incurred as part of a strategic review of the market threats posed by new and emerging digital trading models (I feel that including this as non-underlying is frankly ridiculous). There were also £600K of redundancy costs arising from the reorganisation of direct sales routes that was completed in the period. Finally, the group’s defined benefit pension scheme closed to future accrual in May. This resulted in a £7M curtailment gain which was offset by a further £1.4M of costs incurred in relation to the closure of the scheme, including £1.3M of past service cost for one year’s additional service negotiated with the active members of the scheme.

The group has announced a proposed organisation restructure that is likely to impact around 10% of the total employee base. It is anticipated that the majority of changes from the process will have been implemented by the end of the year and the expected cost of this reorganisation has been estimated at around £4M with an ongoing annual benefit of about £3M.

The government’s proposed soft drinks sugar tax is now in the consultation phase. The board believe this tax is a punitive and unnecessary distortion to competition in the UK market which will be complex and expensive to implement. They believe their actions and sugar reduction progress, along with those of many competitors, make the implementation of a soft drinks only sugar tax an unnecessary measure.

Following the Brexit vote, the reduction in the value of Sterling, if sustained, will lead to higher input costs across a number of key commodities. This is currently forecasted to have an impact of around £3.5M in 2017 but the group are taking action to offset this costs were possible. Going forward, they are starting to see the benefits of their product development initiatives. Market conditions remain volatile and somewhat unpredictable but assuming a strong trading performance in the key Christmas period, they remain on track to deliver profit slightly ahead of last year.

At the current share price the shares are trading on a PE ratio of 16.9 which increases to 17.3 on the full year consensus forecast. After a 5% increase in the interim dividend, the shares are yielding 2.7% which increases to 2.8% on the full year forecast. The net debt position at the period-end was £6.6M compared to £11.3M at the end of last year.

Overall then this has been a difficult half year for the group. Although profits were up, when the pension changes are discounted, they fell year on year. Net assets also declined but there was a healthy increase in operating cash flow with a good level of free cash being generated. Aside from water, all markets daw declines in both volume and value terms, although deflation is expected to reverse slightly going forward. Both the stills and carbonates divisions saw profits decline but profits at Funkin grew during the period. The international business also looks healthy.

Going forward, the outlook statement looks OK but the sugar tax and decline in Sterling both offer potential headwinds and I feel that the forward PE ratio of 17.3 and dividend yield of 2.8% don’t quite offer good enough value to take this into account.

On the 1st February the group announced a trading update covering the whole year. The UK soft drinks market remained highly competitive with value up 1% and volume increasing by 1.5%. The group’s second half trading performance strengthened, supported by product innovation, specifically through the launch of Irn Bru Xtra and Rubicon Spring. Revenue is expected to be around £257M, a growth of 1.5% on a like for like basis.

They have maintained tight control of their costs and in Q4 implemented a re-organisation that has reduced their overhead base. The operating margin for the year remains in line with board expectations. They have announced plans to invest £10M in PET capability at their Milton Keynes facility, further improving efficiency and flexibility. Overall, the board believe that the combination of strong trading, innovation and tight cost control will enable them to meet their profit expectations for the year.

Looking ahead the uncertain economic environment indicates that 2017 will be another challenging year but the board believe they are well placed to deliver long-term value to shareholders. Not a bad update, but nothing really has changed here.