Solid State has now released its interim results for the year ending 2017.

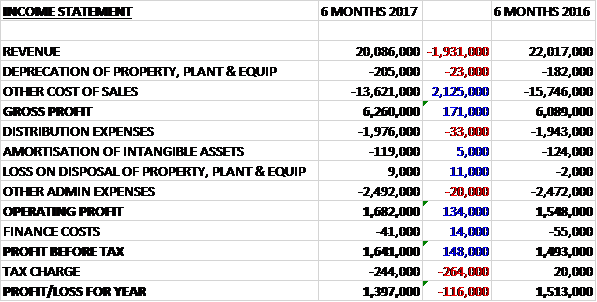

Revenues declined by £1.9M when compared to the first half of last year due to the lack of the mobilisation element of the MOJ contract that was terminated – underlying revenue was flat. Cost of sales also fell, however, due to the MOJ contract being very low margin to give a £171K increase in the gross profit distribution and admin expenses increased modestly and the operating profit grew by £134K. There was a £14K decline in finance costs but the tax charge increased by £264K from a credit last time following a lower R&D claim to give a profit for the period of £1.4M, a decline of £116K year on year.

When compared to the end point of last year, total assets declined by £3.4M driven by a £4.4M fall in receivables and a £762K fall in cash, partially offset by an £887K increase in inventories and a £738K growth in the value of intangible assets. Total liabilities also declined during the period due to a £4M fall in the overdraft and a £524K decrease in payables. The end result was a net tangible asset level of £10.5M, broadly flat over the past six months with a decline of just £14K.

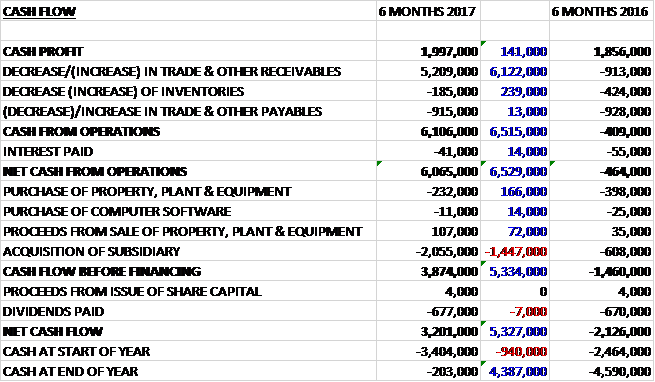

Before movements in working capital, cash profits increased by £141K to £2M. There was a large cash inflow from working capital with a £5.2M decrease in receivables so after interest payments declined modestly, the net cash from operations was £6.1M, a positive movement of £6.5M year on year. The group spent a net £136K on capex and £2.1M on acquisitions to give a free cash flow of £3.9M. After the £677K dividends were paid, the cash flow for the period came in at £3.2M and the cash level at the end of the half was -£203K.

The group benefited from forex gains in the period, reliant in part on forward currency hedges. A continuing weakening of Sterling would not result in a repeat of this benefit in H2, however due to some limited US dollar exposure.

In May the group completed the acquisition of Creasefield for a total consideration of £1.6M. The business specialises in the design and manufacture of custom battery packs to a diverse range or industry sectors principally in the UK including Commercial Aerospace, Oil & Gas, Medical, Subsea, Safety, Water, Rail, Military, Security and Government. It will make a positive contribution to the performance of the group as a whole for the remainder of the year after integration costs and a more significant contribution next year.

The integration of the Creasefield battery operation with the Steatite business has progressed well with efficiencies achieved across both the Redditch and Crewkerne facilities. Production of battery packs are now being predominantly carried out in Crewkerne with the Redditch site focussing on the delivery of computing and communications products. The acquisition has broadened the battery chemistries offered and the range of industrial sectors served by the division and has allowed for a greater share of production and engineering resource.

The combined battery operations are responding to strong demand for power solutions. As well as new opportunities in the industrial sector and harsh environment robotics, existing customers in the aerospace and safety markets are placing repeat business, which gives management confident in the growth potential of this division. The oil and gas industry, which previously accounted for a large proportion of the battery division’s revenue is starting to show signs of recovery but this revenue is now considered supplementary to the existing business flow of the battery division as opposed to being its core as was previously the case.

In the period, Steatite Antennas has had success innovating with a major prime contractor on an electronic solution countering the threat from piracy at sea. In addition, they are now seeing the benefit of interdivisional co-operation and the resulting force multiplier with their battery, computing and rugged communications teams partnering with a third-party company producing a chemical, biological, nuclear and radiological sensor.

The relocation of the division to its new purpose built facilities in Leominster is now underway. Installation of the advanced near field antenna test chamber has already been completed. With additional technical and commercial staff recruited to address pent up demand and to take existing outsourced functions in-house, the business is poised for growth. The business has been requested by a longstanding tier 1 defence OEM client to supply an enlarged loom wired cabinet for advanced systems integration. This is an example for the contribution that Steatite brings to the client relationship through its design-in services and broad product manufacturing capability.

Additionally, the business has been a long term supplier of ticketing machines to the train operating companies. They have been working with them on a redesigned ticketing machine to replace the ones in service at the moment. Just over half these replacement machines have now been supplied to selected companies with the remaining machines to be rolled out under a controlled programme.

At Solid State Supplies, all key metrics are either on target or ahead of target. The book:bill ratio remains positive and the order backlog at the half year point is up 6% and EBIT is slightly ahead of the half year target. In the period the business has expanded its sourcing operation into both component and obsolescence supplies.

Several of the existing customers have carried out audits of their capability in this area and have added them to their register of approved obsolete components suppliers. The division expects several new customers will be added early in 2017 and this area of the business will make a positive contribution to growth in 2018.

The Silicon Labs franchise is now making a significant contribution to the overall business and is expected to increase in value throughout the remainder of the year. During the period the business also secured the Kemet franchise which is a manufacturer of capacitors which complement the existing range of products.

The Ginsbury display business is now benefiting from extensive cross selling and the business has established a close relationship with a number of key Chinese suppliers that is giving it a significant advantage in the market without any compromise in quality. Plans for group cross selling of the battery business are now well advanced and the business has gained access to an increased portfolio of battery cells from leading premium manufacturers.

Despite the fact the MOJ contract was terminated last year, the settlement was not agreed until May 2016. This was agreed on a without fault basis and has resulted in a settlement which will be deployed in the further growth of the group both organically and through acquisitions, of which there is a strong pipeline of potential targets.

While the broader economy continues to encourage prudence in clients’ buying patterns following the Brexit vote, the group order backlog at the period end stood at £14.8M which comprised £12.7M of underlying revenue and £2.1M of Creasefield revenue which compares to £14.2M at the end of last year when the MOJ revenue is taken out so this looks like a reduction in the like for like order backlog, apparently due to shorter order schedules. The board are optimistic about their prospects.

At the current share price the shares are trading on a PE ratio of 8.5 but this increases to 12.1 on the full year consensus forecast. After the interim dividend was maintained at the same level as last year, the shares are yielding 2.9% which increases to 3% on the full year forecast.

Overall then there was not much movement during the period. Profits declined due to a lower R&D tax claim and net tangible assets were flat. The operating cash flow saw a big increase due to a huge reduction in receivables but cash profits did increase modestly too. A lot of free cash was generated due to the big receivable fall, and without this boost the operating cash flow would not have covered the acquisition.

The Creasefield business seems to be bedding in well and Solid State Supplies seems to be enjoying quite a bit of success but progress seems quite sluggish in the other businesses. The order backlog has increased but on a like for like basis, this has seen a decline, apparently due to shorter order schedules. The forward PE of 12.1 and yield of 3% is not too taxing but progress here seems to be a bit slower than I initially thought and although I am currently holding on to the shares, it is not a particularly strong hold.

On the 23rd March the group released a trading update for the year as a whole. Underlying profit before tax is expected to be broadly in line with expectations at over £3.1M. Q4 has seen a number of projects within the higher margin antenna division being delayed so contribution from these projects is expected in future months. The other areas of the manufacturing business unit have performed broadly in line with expectations and the distribution business has performed slightly ahead of expectations.

Profits will be impacted by one off costs arising from the re-organisation of the manufacturing business and the Creasefield acquisition costs of about £200K, and the recent decision to cease development activity in the Steatite Electronic Monitoring Systems business unit. This unit will be treated as a discontinued activity in the year-end accounts and is expected to have attributable losses of about £500K. In addition there are non-cash amortisation charges of acquired intangibles of £200K. The group’s order book stood at £18.1M compared to £16.45M at this point of last year.

Overall though, this all seems a bit like progress is rather hard to come by and I have taken a profit and sold up – I may re-enter after the results if it looks like more progress is being made.