Utilitywise has now released its final results for the year ended 2016.

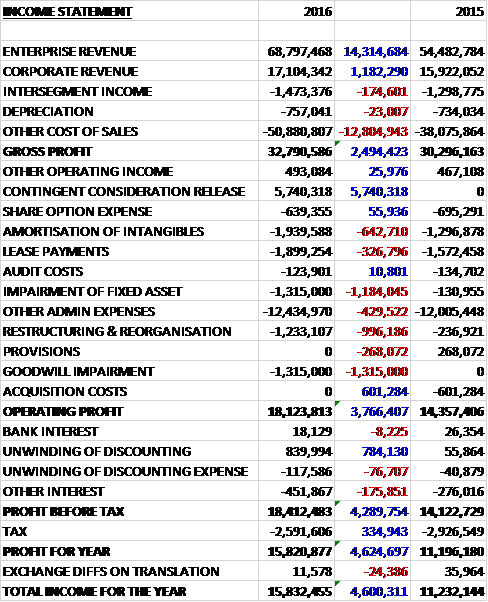

Revenues increased when compared to last year with a £14.3M growth in enterprise revenue and a £1.2M increase in corporate revenue. Cost of sales also grew to give a gross profit £2.5M above that of last year. We then see a £5.7M contingent consideration release offset by a £643K growth in amortisation, a £327K increase in lease payments, a £1.2M growth in impairments, a £996K increase in restructuring costs, a £1.3M goodwill impairment and a £430K growth in other admin expenses to give an operating profit £3.8M above that of last year. Finance income increased and tax payments reduced so the profit for the year came in at £15.8M, a growth of £4.6M year on year.

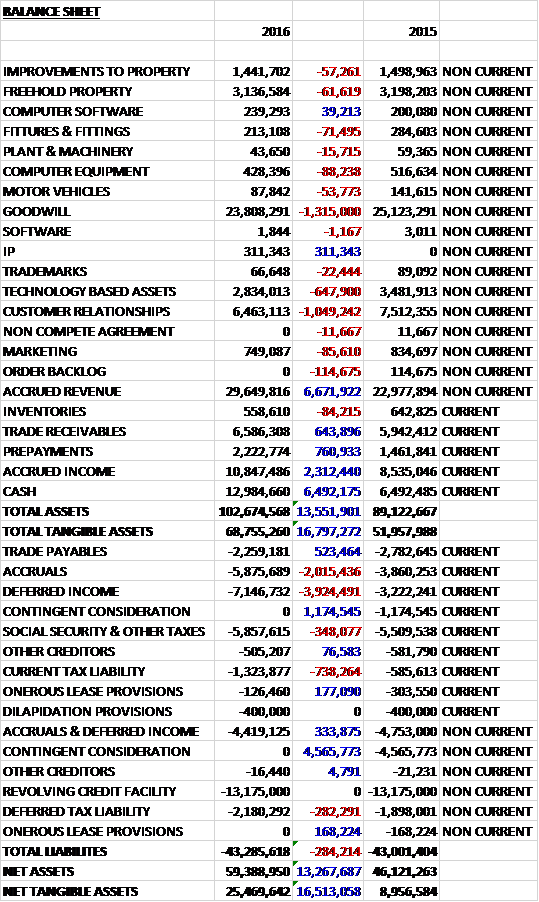

When compared to the end point of last year, total assets increased by £13.6M driven by a £9M growth in accrued income and a £6.5M increase in cash, partially offset by a £1.3M decline in goodwill and a £1M fall in the value of customer relationships. Total liabilities also increased modestly as a £3.9M growth in deferred income and a £2M increase in accruals was partially offset by a £5.7M decline in contingent consideration. The end result was a net tangible asset level of £25.5M, a growth of £16.5M year on year.

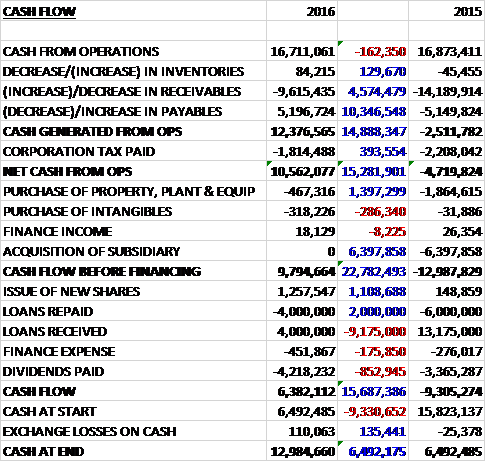

Before movements in working capital, cash profits declined by £162K to £16.7M. There was a cash outflow from working capital with receivables increasing once again but this was less pronounced than last year and after tax payments declined by £394K the net cash from operations came in at £10.6M, a positive movement of £15.3M year on year. The group then spent just £467K on fixed tangible assets and £318K on intangibles to give a free cash flow of £9.8M. The group issued new shares to the value of £1.3M and paid out £4.2M in dividends to give a cash flow of £6.4M and a cash level of £13M at the year-end.

The adjusted EBITDA in the Enterprise division was £17.1M, a growth of £2.8M year on year with the UK and Ireland order book additions increasing by 35% although margins fell somewhat due to the higher attrition in the sales force population. European revenues were up £2.2M to £7.7M with continued progress in the main markets of France and Germany.

The adjusted EBITDA in the Corporate division was £1.2M, a decline of £2.3M when compared to last year as the group increased its investment for future growth and the growth in lower margin ESOS project work which resulted in the acquisition of 214 new customers with 37% actively considering procurement. Revenues were up 7% due to a full year contribution from T-Mac, otherwise they would have fallen.

The change in payment terms with some suppliers combined with a reduced reliance on renewals and extensions has improved the cash conversion and the group expect this to continue.

The year was impacted by the energy consultant headcount falling behind the planned growth rate and as a result the year-end number of 625 represented only a 2.5% increase over the prior year and although they have been successful in recruiting new energy consultants during the period, the net increase was low due to the level of attrition. The attrition challenge is being addressed by a number of initiatives following the appointment of a People Operations Director. These include improvements to the recruitment process, a new on-boarding, training and coaching programme to advance consultant success rates and the strengthening of the team and management structure including a higher ratio of support staff to energy sales people.

The group have appointed Brendan Flattery as CEO and Geoff Thompson, the founder and previous CEO has stepped into the role of executive chairman with the current chairman moving to a non-executive role. Earlier in the year MD of the Enterprise division Steve Attwell left the group and Chris Charlton was promoted internally having managed the European business immediately prior.

The integration of T-mac Technologies has been successful and enabled the group to access additional opportunities as a result of their enhanced offering. The acquisition added cloud based energy monitoring and controls capability to the service portfolio. The number of customers benefiting from the smartdash data analytics software acquired with T-mac is currently at 1,808 and a plan is in place to roll out the software to all customers as they arrange installation of its AMR Smart Meter.

This service enables a wider and more comprehensive dialogue around energy management with customers and includes the deployment of the Edd:e monitoring hardware alongside the T-mac controls hardware as a key part of this.

The partnership with Dell to introduce internet of things building automation solutions to customers is progressing well with trials underway and the group see a significant opportunity to roll this out to both new and existing customers. IoT connects internet-enabled devices with software to provide users with a more granular control over energy consuming assets. Devices include heating, ventilation and aircon, security, refrigeration and lighting. Connecting disparate devices together in a single, intelligent system can provide significant cost and performance advantages over traditional building energy management systems.

Exceptional items in the year relate to an impairment charge in connection to the acquisition cost of T-mac Technologies. There is also a credit of £5.7M which has arisen from the release of deferred consideration where earn-out criteria are not anticipated to be met. There was also a charge of £509K in relation to legal fees incurred as a result of a dispute with a competitor and restructuring and re-organisation costs such as settlement payments of £678K.

Future secured revenue as declined by 2.3% to £25.6M but order book additions in the UK and Ireland were up 35% to £84.5M. The board are confident in their outlook for the year ahead and having started the year in line with expectations, look forward to continued strong revenue growth and profit generation. The will launch in Q2 their family of internet of things technology solutions and have developed the Advantage Plan, created new revenue streams and changed the nature of their billing relationship with customers. The deregulation of the commercial water market in England also provides another revenue opportunity that they will run alongside their existing energy procurement offering.

At the current share price the shares trade on a PE of 11.9 (excluding some impairments and the deferred consideration movements) but this falls to 9.7 on next year’s consensus forecast. After a 30% increase in the total dividend the shares are yielding 3.4% which grows to 3.7% on next year’s forecast. The net debt position at the year-end was just £200K compared to £6.7M at the same point of last year.

On the 17th October the group announced that it had been selected by Asda Stores as their chosen supplier of internet of things building solutions. Under the terms of the agreement, they will work with Asda’s facilities services partner, City Holdings, to deploy their Integrated Technology Management Solution across its UK estate.

On the 31st October the group announced that new CEO Brendan Flattery acquired 60,000 shares at a value of just under £100K. This represents his first purchase.

Overall then this has been a bit of a slow year in some respects but progress has been made in others. Profits did increase but when we take out the effects of the goodwill impairment and contingent consideration release, they were broadly flat with a small decline. Net assets grew and the operating cash flow was up with some decent free cash. This was due to an improvement in working capital movements, no doubt aided by the improved payment terms. Cash profits actually declined marginally during the year.

The enterprise division seems to be doing fairly well with increased profits but sales personnel attrition is holding it back somewhat. The corporate business saw profits fall which is being attributed to lower margin work and greater investment in the business. There does seem to be some decent new technology and revenue streams coming on line and although the future secured revenue has declined, the order book is up.

The forward PE of 9.7 and dividend yield of 3.7% looks pretty good and there is very little in the way of debt at the moment. This is a tricky one – now that the group seems to be cash generative, this has removed a lot of the issues I had with it but operationally, this year has been rather difficult. I am tempted to take a punt at these levels.

On the 15th December non-executive director Richard Feigen sold 58,675 shares at a value of £111K. He is now interested in just 10,000 shares – not a good omen.

On the 23rd December the group announced that non-executive director Paul Hailes sold 10,000 shares at a value of £19.4K. Not a huge sale and he still holds 35,000 shares.

On the 21st February the group released a trading update for the six months to the end of January. The group performed in line with management expectations during the period with double digit revenue growth compared to the same period of last year. Net debt was £4.1M compared to £10.2M at this point of last year and £200K at the year-end.

The enterprise division performed strongly with an increase in revenue and profit compared to the same period of last year. Gross order book additions were £50.2M compared to £40.4M last time and the revenue pipeline increased from £25.6M to £28M over the period.

The corporate division saw a reduction in revenue primarily due to slower progress than previously hoped in the deployment of technology solutions to certain customers but was also impacted by ESOS related revenue in the first half of last year which has not recurred this time. That revenue reduction, coupled with the ongoing investment that started in the second half of last year, has led to a reduction in profit compared to H1 last year. The board remains confident in the outlook of this division.