Origin Enterprises has now released its final results for the year ended 2016.

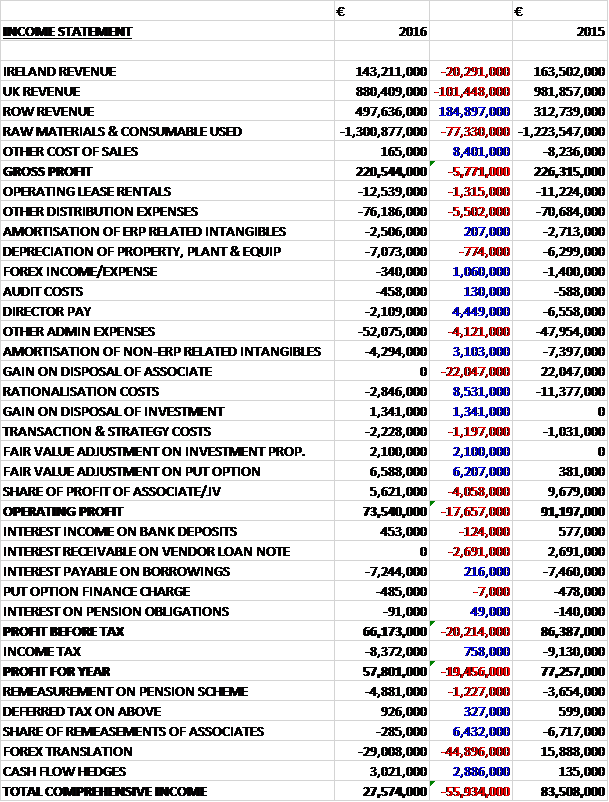

Revenues increased when compared to last year as a €20.3M decline in Irish revenues and a €101.4M fall in UK revenue was more than offset by a €184.9M growth in ROW revenues, with the growth entirely down to forex movements as constant currency revenues declined due to lower input prices and crop marketing volumes. Cost of sales also grew due to an increase in raw materials and consumables used so the gross profit fell by €5.8M. Distribution expenses were up €6.8M but there was a €1.1M positive forex movement. Amortisation declined by €3.1M, rationalisation costs were down €8.5M, there was a positive €6.2M movement in the fair value adjustment of the put option and a €2.1M positive movement in the fair value adjustment on investments.

There was no gain on disposal of an associate, however, which netted €22M last year and the share of joint venture profits declined by €4.1M due to the disposal of the Valeo Foods shareholding, all of which meant that the operating profit decreased by €17.7M. There was no interest receivables on the vendor loan note this time, which brought in €2.7M in 2015 but tax charges fell by €758K to give a profit for the year of €57.8M, a decline of €19.5M year on year.

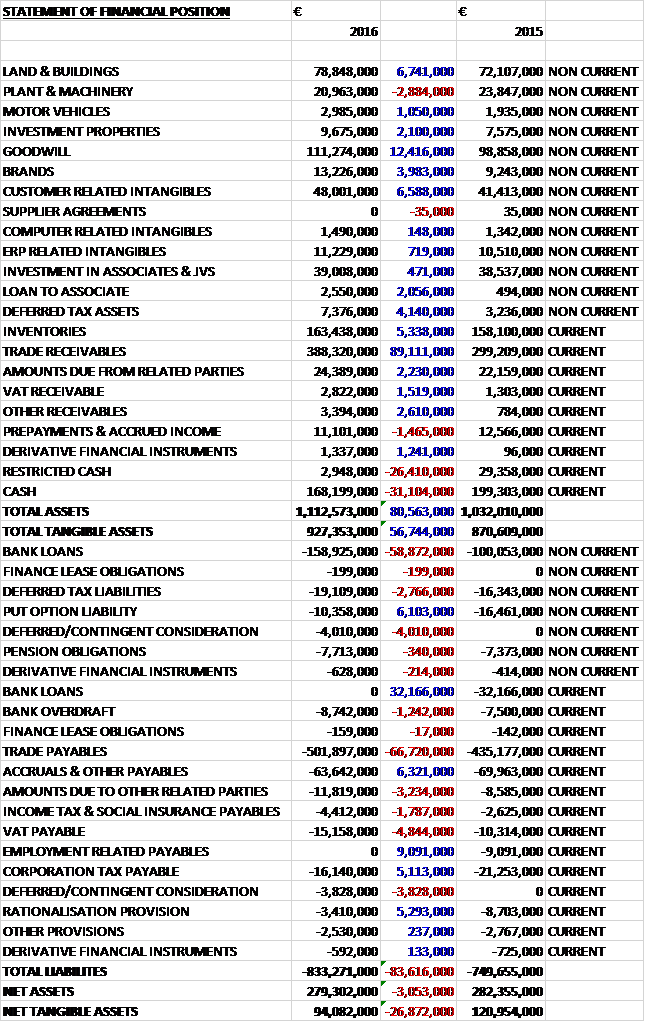

When compared to the end point of last year, total assets increased by €80.6M driven by an €89.1M growth in trade receivables, a €6.6M increase in customer related intangibles, a €12.4M increase in goodwill and a €6.7M growth in the value of land and buildings, partially offset by a €57.5M fall in cash. Total liabilities also increased during the year as a €66.7M growth in trade payables and a €26.7M increase in bank loans was only partially offset by a €9.1M decline in employment related payables. The end result was a net tangible asset level that decreased by €26.9M year on year.

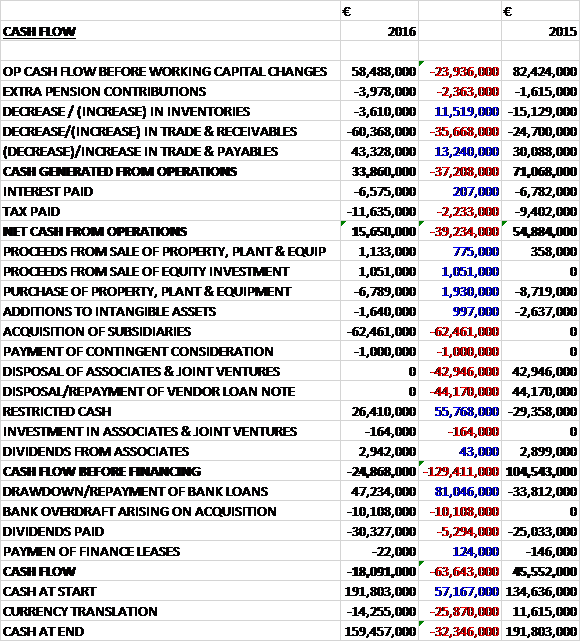

Before movements in working capital, cash profits declined by €23.9M to €58.5M. There was a cash outflow from working capital which was larger than last year, mainly as a result of a large growth in receivables, and after tax payments increased by €2.2M the net cash from operations came in at €15.7M, a decline of €39.2M year on year. The group spent a net €4.7M on property, plant and equipment along with €1.6M on intangible assets and €63.5M on acquisitions which meant that before financing there was a cash outflow of €24.9M. The group drew down a further €47.2M of bank loans and after dividends of €30.3M were paid and the €10.1M of overdraft acquired with the acquisition, the cash outflow for the year was €18.1M and the cash level at the year-end was €159.5M.

Agri-services had a challenging year. Underlying revenue decreased 3.7% due to the impact of lower input prices and crop marketing volumes. Underlying service revenue and input volumes increased 0.1% during the period, reflecting a 3.2% reduction in Ireland and the UK with a 12.2% increase in Central and Eastern Europe. The operating margin reduced, largely reflecting the impact of unseasonal weather and weaker primary producer returns.

In the UK Agrii performed robustly in a very difficult environment. The business recorded lower revenues and margins due to a combination of adverse weather and reduced farm profitability. Unseasonably lower temperatures and higher rainfall levels across the UK during Q2 and Q3 led to very late spring growing conditions which resulted in delayed and missed service and input application. Pressure on farm incomes and cash flow, combined with the more compressed nature of seasonal activity led to highly competitive trading conditions and lower demand across a variety of market sectors. Agronomy service revenue and crop protection volumes recovered well during Q4 following significant shortfalls in Q3. Seed and nutrition performed strongly for the year as a whole, growing market share despite the challenging backdrop.

In Poland the business achieved a satisfactory result in the context of extreme weather conditions which negatively impacted revenues, profits and margins. Service and input application was significantly curtailed following a combination of prolonged frost conditions and an absence of snow cover throughout Northern and Central Poland during March and April. This unusual weather pattern led to the loss of about 20% of total autumn and winter crop plantings in additions to a shorter growing season for spring cropping. The market backdrop was generally mixed reflecting weak farm sentiment due to poor crop potential and a delayed season. This, together with a reduced market for service and input application drove highly competitive trading conditions.

The group’s Romanian operations delivered a good maiden contribution this year. There was a strong organic performance with higher underlying revenues, volumes and margins reflecting growth in all service and input portfolios. Crop growing conditions were generally excellent throughout the period reflecting the benefit of good autumn establishment and favourable spring weather. Integration was advancing during the period with the initial areas of focus being organisational simplification, the introduction of enhanced technical support to the sales teams and product specialists, and the establishment of five knowledge transfer demonstration farms.

In Ukraine a more challenging market backdrop in the year drove a lower year on year operating profit result, with service providers responding competitively to the impacts of weaker local currency and on-farm cash flow pressures on primary producer economics. Soil fertility and seed technology applications maintained good development momentum during the period. New customer gains in the year were supported through the expansion of the agronomy sales force together with an extension of the regional distribution footprint of the business.

Business to Business agri inputs achieved a satisfactory performance in highly competitive market conditions. General uncertainty regarding fertilizer raw material price development and delayed seasonal timing due to late spring conditions, together with pressures on farm incomes, drove lower revenues, volumes and margins in the year. Weaker demand in the UK was partly offset by a robust volume performance in Ireland underpinned by higher livestock numbers with primary producers focused on maximising grass production to achieve higher milk volumes.

Amenity performed satisfactorily in the year with the professional channel continuing to provide growth opportunity supported by new customer development and the benefit of ongoing product and service innovation. Development continues to be positively supported through the formation of industry leading partnerships. During the year, Rigby Taylor became the official service provider to the UK FA pitch improvement programme, an initiative to improve playing surfaces in order to encourage increased participation in grass roots football. In 2016, the group completed the acquisition of UK-based Headland Amenity, a niche provider of turn management and maintenance solutions which should enhance the group’s sector position in the wider amenity market.

Against the backdrop of weaker returns from beef and dairy enterprises, Feed achieved a satisfactory performance underpinned by a modest volume increase in the period. Sport demand was robust at varying times during the year reflecting unsettled weather patterns, while price volatility drove generally weaker forward buying momentum. The John Thompson joint venture delivered a satisfactory performance during the year.

During the year the group made a number of acquisitions. In September 2015 they acquired Redoxim which is a provider of agronomy services, macro and micro inputs to arable, vegetable and horticulture growers based in Romania. In November they acquired the Kazgood group based in Poland. The business provides agronomy services, inputs, crop marketing solutions and is a manufacturer of micro nutrient applications. In December they acquired Comfert SRL. Based in Romania, the business is a provider of agronomy services, integrated inputs and crop marketing support to arable and vegetable growers.

In August 2015 the group acquired ReSo Seeds ltd, a UK-based mobile seed cleaning and processing specialist. Finally, in July 2016 they acquired Headland Amenity ltd, a UK-based supplier of products and synergistic programmes to improve sports turf surfaces. All of these business were acquired for €76.8M, including the debt acquired, and generated goodwill of €26.6M.

As can be seen there were a number of exceptional items this year (as in every year). Rationalisation costs comprise termination payments arising from the restructuring of agri-services in the UK; a gain on disposal of an investment in Adaptris has been recorded for €1.3M; transaction related costs principally comprise costs incurred in relation to the acquisitions during the year and strategy related costs relate to one-off costs associated with the Agri Services strategy review. Also, during the year the group conducted a valuation of their investment properties which resulted in an increase in the carrying value of the properties of €2.1M. Finally, the fair value gain on the put option liability relates to the movement in fair value of the liability in respect of the Agroscope acquisition.

Notwithstanding the fact that sector sentiment remains subdued reflecting the current pressures on farm incomes, the group is well positioned to respond to present market conditions and to benefit from a sustained improvement in primary producer returns.

At the current share price the shares are trading on a PE ratio of 16 which falls to 13.6 on next year’s consensus forecast. At the year-end, the group had net cash of €200K compared to €59.4M at the end point of last year. This figure considerably flatters the situation, however, and the average net debt during the year was €190M which was a similar level to 2015. After the dividend was kept the same this year, the shares are yielding 3.5% which is expected to remain the same again next year.

On the 25th November the group released a trading update covering Q1 2017. They had an encouraging start to the year with all businesses performing well in the seasonally quiet first quarter. A combination of generally favourable weather conditions and an improved planning environment for primary producers in the period in key geographies led to good early season activity levels on-farm resulting in higher demand for the group’s services and inputs. The total sown area for the principal autumn and winter crops is broadly equivalent to last year across the group’s markets. On the assumption of normal weather patterns, this cropping profile provides a solid foundation for the second half of the year.

Revenue from agri-services saw an 11% increase with underlying revenue up 1.3% reflecting higher seed, crop protection and fertilizer volumes, largely offset by lower fertilizer and feed prices and lower crop marketing volumes. Underlying service revenue and input volumes increased 7.2% in the year.

In the UK, Agrii delivered a satisfactory performance in the period, recording higher year on year revenues and margins. There was solid momentum across all service and input portfolios as favourable weather conditions supported crop planting activity in the quarter. Primary crop producers experienced a more stable planning and operating environment in the period with their margins currently benefitting from a combination of lower unit costs for key macro inputs and recent sterling depreciation.

Autumn and winter crop plantings are well advanced with estimates for the total sown area at 2.95M hectares, broadly similar to last year. In the case of winter wheat there is an estimated 1.4% increase in plantings but winter oil seed rape is showing an estimated reduction of 10%, largely due to agronomic and rotational crop planning decisions.

In Poland performance was satisfactory. This was against the backdrop of weak farm sentiment due to the impact of highly unseasonal weather patterns earlier in the calendar year which resulted in below average crop yield and quality. Agrii’s agronomy portfolios maintained development momentum in the period, reflecting more focused customer channel management in the enlarged business. There has been solid progress with respect to crop sowings in the period with total plantings for the principal autumn and winter crops estimated at 6M hectares compared with 5.9M for last year.

In Ukraine there was an improved Q1 performance with new season momentum supporting higher revenues and margins as the business benefits from the recent expansion of its distribution footprint. Market conditions continue to be impacted by currency weakness which is leading primary producers to adopt more concentrated or just in time procurement patterns.

While crop planting progress has been slower than anticipated due to below average rainfall in Central and Western Ukraine, autumn and winter sowings are expected to be head of last year. Total autumn and winter plantings for cereals and oil seed rape are estimated at 7.6M hectares compared with 5.8M hectares last year. Total forecast plantings for the growing season as a whole are expected to be equivalent to last year at about 21M hectares.

The Romanian business delivered a satisfactory performance. A combination of good early autumn planting and growing conditions together with new customer development supported higher underlying revenues, volumes and margins across all service and input portfolios. Recent rainfall has delayed the final harvesting of earlier spring sown crops and curtailed progress on new plantings. The total sown area for autumn and winter crops is estimated to be 3.15M hectares compared to 3.25M hectares last year. The shortfall is expected to be reflected in higher spring cropping.

Business to business agri inputs in the UK and Ireland achieved a good result in the period with performance benefitting from a combination of higher volumes and improved margins. Increased volumes were the principal driver supporting the performance of fertilizer in the period. Greater visibility on raw material pricing is providing confidence to primary producers to fix a portion of their nutrition requirements ahead of the main application period in the second half of the year. The amenity business performed satisfactorily in the period underpinned by continuing momentum within the professional sports turf channel. Headland Amenity, which was acquired in Q4 last year, performed well in the period with the integration progressing to plan. Feed ingredients delivered a satisfactory result supported by a stable year on year volume performance and John Thompson also delivered a satisfactory performance in the period.

Although sector sentiment remains subdued reflecting the current pressures on farm incomes, there has been an encouraging start to trading in Q1. The autumn and winter cropping profile established to date provides a solid foundation for the more important second half of the year.

Overall then this has been a difficult year for the group characterised by inclement weather across most of their markets. Profits are down, depending on which non-recurring items are omitted, net assets declined and the operating cash flow fell with even free cash before acquisitions not covering the dividends. In the UK, adverse weather and lower farm profits weighed down on profits with Poland also suffering from poor weather and progress in Ukraine being held back by a weak local currency and poor farm cash flow. The only area to see growth was Romania which benefitted from excellent growing conditions.

So far this year, the performance has been much better due to improved weather conditions. The UK was solid due to better weather but Poland still struggled due to weak sentiment and poor weather earlier in the year. Ukraine put in an improved performance but currency weakness is still a problem and Romania performed well due to new customers and better planting conditions, although recent rain has delayed harvests. Fertilizer volumes improved as there was greater transparency on raw material prices.

Pressure on farm incomes continued but so far this year seems to be improving and with a forward PE of 13.6 and yield of 3.5% these shares may be worth a go. The fact that they are reliant on the weather is a problem but assuming normal conditions return, this could be interesting.