Getech has now released its final results for the year ended 2016.

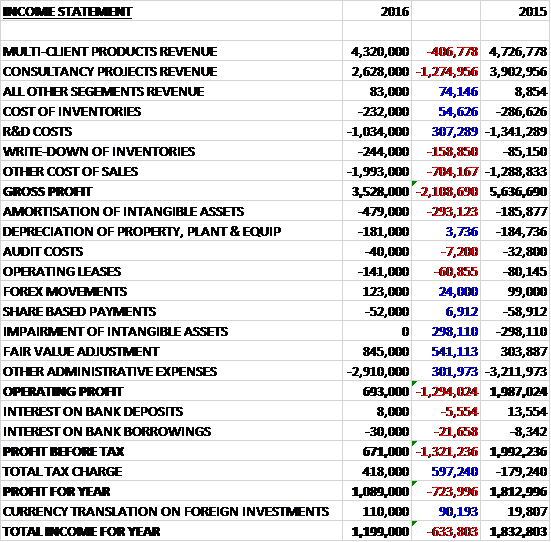

Revenues declined when compared to last year due to a £407K fall in multi-client products revenue and a £1.3M decrease in consultancy projects revenue. R&D costs fell by £307K but other cost of sales increased by £704K to give a gross profit £2.1M below that of 2015. Amortisation charges increased by £293K relating to the first full year of Globe platform amortisation costs, and operating leases grew by £61K but there was a £24K positive forex effect, a £541K growth in fair value adjustments, no impairments, which accounted for £298K last year, and a £302k reduction in other admin expenses to give an operating profit £1.3M down on last year. Interest charges grew but there was a £418K tax rebate compared to a £179K charge in 2015 so the profit for the year was £1.1M, a decline of £724K year on year.

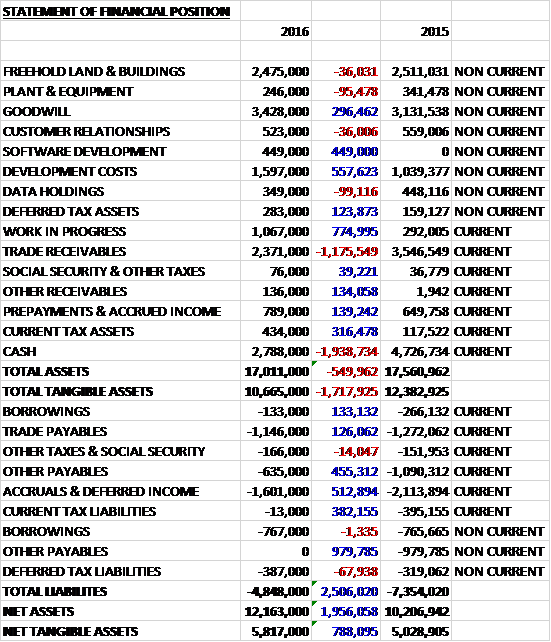

When compared to the end point of last year, total assets declined by £550K, driven by a £1.2M fall in trade receivables due to the payment of outstanding debtor balances from national oil companies, and a £1.9M decline in cash, partially offset by a £558K increase in the value of development costs, a £775K growth in work in progress due to the timing of the multi-client regional reports product cycle with several new reports nearing completion to be sold in 2017, and a £449K increase in software development. Total liabilities also declined during the year due to a £1.4M fall in other payables and a £513K decrease in accruals and deferred income, mainly relating to Globe deliverables. The end result was a net tangible asset level of £5.8M, a growth of £788K year on year.

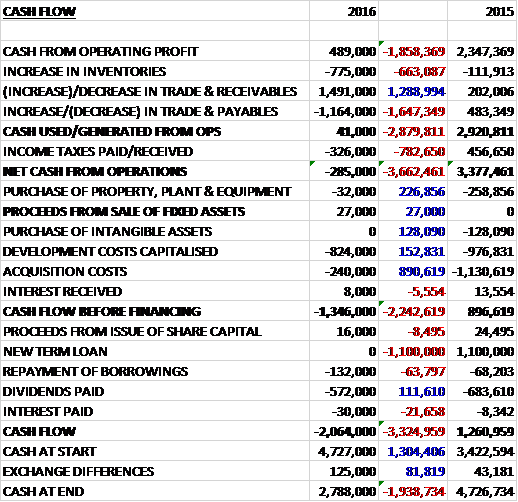

Before movements in working capital, cash profits declined by £1.9M to £489K. There was a cash outflow from working capital, which was greater than last year and after a £783K swing to tax payments, there was a net cash outflow from operations of £285K, a detrimental movement of £3.7M year on year. The group didn’t really spend anything of property, plant and equipment but development costs were £824K and £240K was spent on acquisitions to give a cash outflow of £1.3M before financing. After £572K was paid out in dividends and some borrowings were repaid, the cash outflow for the year was £2.1M and the cash level at the year-end came to £2.8M.

The profit in the multi-client products and service division was £2.9M, a decline of £272K year on year whilst the profit in the consultancy project division was £658K, a fall of £1.6M.

With oil prices remaining low and volatile during the year, the market backdrop remained challenging for the group. Budgets for drilling exploration wells did not say any significant signs of recovery and the market for proprietary consulting work remained week. The group’s clients continue to refresh and rework their views around the opportunity sets within and outside of their exploration portfolios, however, which has resulted in continued demand for their data and regional multi-client consulting activities.

During the year the group enhanced its capabilities in gravity and magnetics through the formation of a dedicated centre of excellence. As a low-cost alternative to seismic data, gravity and magnetic data continues to be seen as an attractive purchase of natural resource companies. As such, data sales remain an important revenue stream. In July 2016 they delivered the three-year Altimeter Gravity Programme which has provided a route for their customers to enhance the quality of their satellite data.

Globe, as a client-funded product suite, is now in its sixth year of support and continues to gain more interest and use. Activity through 2016 was pre-funded by a broad grouping of international oil company and large independent oil company customers.

Within consulting, the year saw the completion of work on the Angolan basin review for Sonangol which was one of the largest they have had. They have recently been awarded further consultancy work by the government of Sierra Leone.

The group has made a couple of acquisitions. ERCL was completed in 2015 and its operations were integrated into the group during 2016. The business has extended the group’s commercial reach beyond its traditional regional gravity and magnetics new business venture market into a more seismic-linked sphere where they are now able to offer detailed well planning, field development and asset and data management advice.

Under the ERCL brand the group continued to support the Mozambique government’s petroleum activities through the provision of commercial and geotechnical training and advice. As part of this work, the year saw the completion of the country’s fifth licencing round and work commenced on preparation of data products for future rounds.

In addition to this, ERCL recently won a World Bank contract to support the government of Sierra Leone in its petroleum activities and it has ongoing work in a number of other countries including Lebanon, Namibia, Palestine and Pakistan. They also provide exploration and development-based technical assistance to a range of independent upstream companies with recent activity including operations in China, Equatorial Guinea, Mexico, Morocco and Spain.

In June 2016, the group acquired Exprodat. The business specialises in the provision of services and consultancy relating to data management and the use of GIS. GIS is an industry-standard tool that is fundamental in supporting many aspects of oil and gas operations. The group already has a long standing GIS team but they had to date been focussed on servicing the group’s internal business needs so Exprodat brings an additional GIS resource that is dedicated to generating an external income stream for the group.

Exprodat has developed and licenses commercially several GIS software packages that support petroleum exploration. During the current downturn, the client retention of these subscription-based software products has been around 95% which brings a substantial client base to the group with a significant proportion of recurring revenue. The business also delivers GIS training in both public and private environments.

Following these acquisitions the group is now looking to extend its operations beyond its core oil and gas customer base and they are currently engaged in operations in the nuclear, mining, agriculture and water management industries. Although not yet significant as standalone revenue streams, the recent advances into these sectors highlight the fact that their geoscience and GIS skills have the potential to be applied to a much broader spectrum of activities. These opportunities are under investigation and have the potential to diversify the revenue base.

In the first half they implemented significant cost control measures which resulted in a material step-down in the cost structure with staff, general and admin costs lowered by 22% on an annualised basis. Having rationalised their cost base towards the end of the first half, there was an improved underlying performance in the second half with a profit of £530K compared to £140 in H1. The cost base is predominantly in Sterling but a significant proportion of revenues are denominated in dollars so recent forex movements have been favourable, adding £123K to annual profits.

During the year the group appointed Dr. Jonathan Copus as CEO in August 2016, having previously worked as an exploration geologist at Shell, an E&P sell ide analyst at a number of city companies and most recently as CEO at Salamander Energy, which was acquired by Ophir in 2015. Also, Chris Flavell has joined the board. He has 35 years of experience in operating E&P companies and consultancies, most recently managing Tullow Oil’s exploration geoscience team before leaving to form a geoscience-focussed recruitment consultancy. In addition, Raymond Wolfson, Colin Glass and Paul Carey are stepping down having spent considerable time at the company.

The oil price has strengthened recently which, combined with a reduced cost profile, should make future E&P investment more attractive. At the same time, the deep cuts to staffing in many companies meant that their capability to undertake exploration is severely curtailed. While the market is at best uncertain, the group has a pipeline of significant sales prospects awaiting approval. For the first time in several years, feedback from clients leaves the board encouraged by the market mood and the recent increase in the oil price gives their customers more confidence that their budgets will become available in 2017.

If we discount the fair value adjustment the shares are trading on a PE ratio of 50 and I have been unable to find a forecast for the coming year. Sensibly the group has opted not to pay a final dividend this year.

On the 29th November the group announced that director Peter Stephens acquired 300,000 shares at a value of £75K. He now holds 1,395,500 shares.

On the 13th December the group the group released a trading update. Following the rebound in profitability in the second half of last year, they have secured several strategically important new contracts and their day to day activities continue to be focused around the customer, profitability and diversified growth.

They have secured a new sale of Globe phase-two to a major, and have been contracted by the UK Oil and Gas Authority to develop and implement a GIS information management strategy. This work for the OGA extends their operations beyond their core exploration market, being focused on spatial data that spans the full E&P asset lifecycle. In addition, having won their first contract within the nuclear industry last year, they are currently at an advanced stage of discussions to expand on this work.

Going forward, although the outlook for the core exploration market remains uncertain, feedback from customers leaves the board cautiously encouraged by the market mood.

Overall then, this year has clearly been a difficult one for the group with continued low oil prices affecting client budgets considerably. Profits declined and there was a net operating cash outflow in the year. Net assets did improve, however, and the multi-client products and services have been holding up much better than the consulting products. The second half of the year did see an improvement, however, as the group cut costs and started expanding outside of their core oil and gas area.

So far this year, the oil price has improved and the group have won some new contracts. The current PE ratio of 50 is very expensive but given the improvements in the second half of last year, I would expect that to be lower this year – it is a shame there don’t seem to be any forecasts. There is also a director purchase and I have to say that these shares look more interesting now than they have done for some time – I’m thinking about dipping in here.