Zytronic has now released its final results for the year ended 2016.

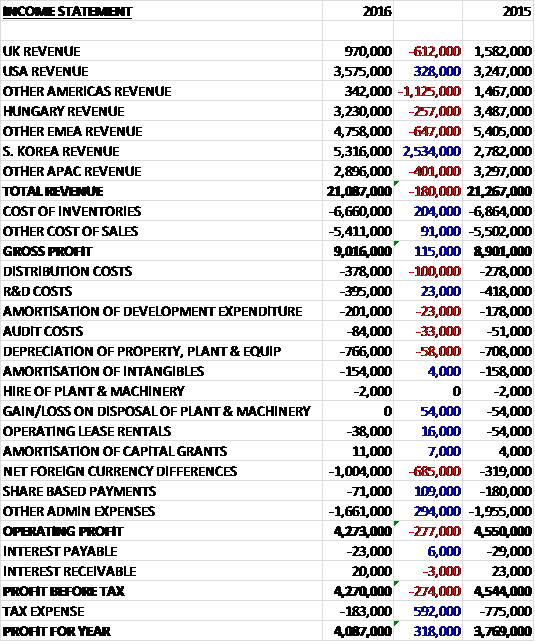

Revenues declined marginally when compared to last year as a £2.5M growth in Korean revenue and a £328K increase in US revenue was more than offset by a £1.1M decline in other Americas revenue, a £900K reduction in EMEA revenue and a £401K decrease in other Asia Pacific revenue. Cost of sales also declined, however, and the gross profit was £115K higher. Distribution costs increased by £100K and there was a £685K increase in forex losses, partially offset by a £109K decline in share based payment and a £294K decrease in other admin expenses to give an operating profit £277K below that of last year. Interest costs were broadly flat but there was a substantial £592K reduction in tax charges due to changes in deferred tax, enhanced tax reliefs after electing into the Patent Box regime and over-provision in prior years to give a profit for the year of £4.1M, a growth o £318K year on year.

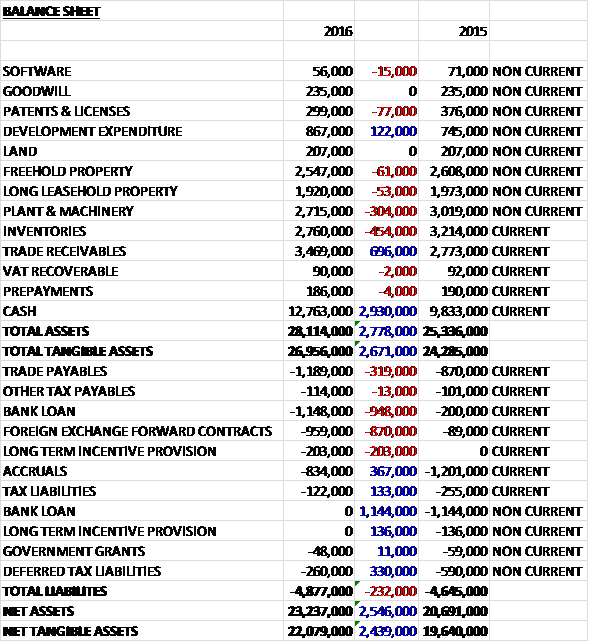

When compared to the end point of last year, total assets increased by £2.8M to £2.1M driven by a £2.9M growth in cash and a £696K increase in trade receivables, partially offset by a £454K decline in inventories and a £304K fall in plant and machinery. Total liabilities also increased during the period as an £870K growth in forex liabilities and a £319K increase in trade payables was partially offset by a £367K decline in accruals and a £330K fall in deferred tax liabilities. The end result was a net tangible asset level of £22.1M, a growth of £2.4M year on year.

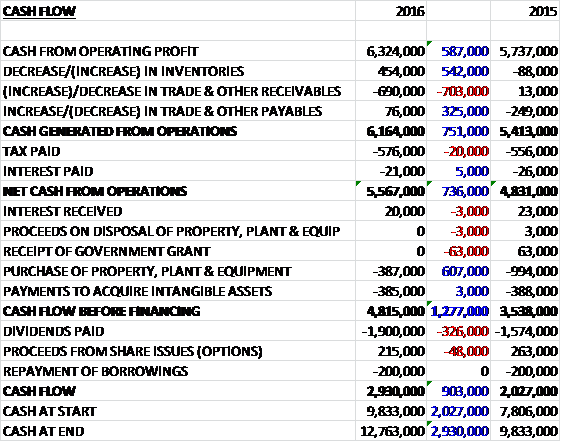

Before movements in working capital, cash profits increased by £587K to £6.3M. There was a small cash outflow from working capital but this was less than last year and after a £20K growth in tax payments the net cash from operations came in at £5.6M, a growth of £736K year on year. The group spent £387K on tangible assets and £385K on intangibles which meant there was a free cash flow of £4.8M, of which £1.9M was paid out in dividends to give a cash flow of £2.9M and a cash level of £12.8M at the year-end.

During the year revenues for the touch sensor business grew by 5% to £18.2M whereas there was a 26% reduction in revenues to £2.9M of the original non-touch glass display products which they have been diversifying away from for several years. By far the most significant factor for this reduction was a further decrease in the ATM displays revenue of £700K to £1.6M.

Exports accounted for 95% of the total revenues whilst touch export revenues grew by 8% to £17.6M. There was a significant growth in Asia Pacific touch sales coming from their bespoke curved MPCT solutions in the gaming market but a reduction in Americas touch sales, mainly associated with the vending machine market. The total number of touch sensor units supplied across all size ranges was 130,000, a reduction of 19,000 with the most significant fall attributable to a decrease in medium-sized 15” sensors associated with vending applications.

The financial market remained the top touch revenue generating application at £6.4M, a £100K increase. The market was affected by Asian ATM manufacturers continuing to strengthen their local positions against the group’s larger global ATM customers as well as the merger of Diebold with Wincor Nixdorf. The gaming market continued to show considerable growth and became the second highest touch application revenue contributor with a £2.5M increase to £5.9M as project deliverable increased.

The vending market saw revenues declined by £1.1M to £2.6M. As expected the decline in both volume and revenue was mostly attributable to another year of significantly reduced supply for the medium sized 15” Coca Cola Freestyle units, after their substantial purchasing of sensors to align with the original LCD display unit end of life programme in 2015.

The industrial and signage application markets declined by £600K to £1.4M and £200K to £1M respectively. By far the biggest contributor to the drop was the 52% reduction across numerous individual projects from the French channel partner, coupled with the effects in general of the oil and gas sector. Signage was affected by the end in 2015 of the car showroom information table system project for a new model launch with a UK customer.

In combination the other application markets of healthcare, home automation and telematics increased by £100K to £900K with the volume of the cooktop project, under home in particular, improving over the year.

The work in establishing an increased direct presence for the group in some key geographies continued with the appointment of a US-based national sales engineers. This was complemented by the increase to 41 in their channel partner network from 38 with 16 regional agreements across the Americas, 11 across APAC, 13 across EMEA and one new global value added reseller agreement with the display division of Future Electronics.

A key feature of the year has been the continued development of the multi-touch multi-user mutual projected capacitive technology for ultra-large format sensor designs. This has continued their strategic focus on key growth application areas such as casino cabinet gaming, casino surface table gaming and vertical and horizontal signage.

The group completed the design and production release of the ZXY150 series controller for MPCT functionality in the large volume area of sensor sixes less than 20”. In conjunction with this development, the silicon phase of the developed Zytronic MPCT application specific integrated chip started, with delivery of first article approval samples of the ASIC expected in January 2017. The production release of MPCT controllers supporting the full range of sensor sizes incorporating the ASIC is scheduled for Q4 2017.

Over the period the group also continued further developments of their software and firmware IP, in both the PCT and MPCT solutions with the release of Android and Mac operating systems specific hardware drivers as well as a single finger unique zoom functionality instead of the normal multi-finger gesture.

A significant amount of development time over the year was expended on the design and procurement of a laser system for the bonding of their electrode pattern to their flexible PCB controller connector tails, with a production ready unit expected to be in service by January 2017. The group also continued over the year to work on alternative sensor electrode materials as well as providing significant technical support into their relationship with Cryptera as they move towards and expectation of 2017 production projects of encrypted touch solutions.

Following the major capacity planning expansion work undertaken last year, this year’s spend in plant and equipment has been incurred in adding several new 2D direct-write electrode printing machines to increase the throughput and capacity of the production of ultra-large touch sensors. A large portion of the spend in intangible assets related to continued work on the MPCT Asia Pacific project and a new Fibre Laser PCB Bonding Table and Vision system.

The Patent Box regime allows companies to apply a rate of corporation tax of 10% to profits earned from patented inventions and similar IP. As the group have now opted in, claims have been made in relation to 2014 and 2015 along with the 2016 estimate which has resulted in income of £289K and £127K respectively.

The year has started well with orders, revenue and current trading ahead of the same period last year.

At the current share price the shares are trading on a PE ratio of 15.6 which falls to 14.3 on next year’s consensus forecast. After the dividend was increased by 20% the shares are yielding 3.5% which increases to 4.1% on next year’s forecast. Net cash at the year-end stood at £11.6M compared to £8.5M at the end of last year.

Overall then this has been a pretty decent year for the group. Profits did increase but this was due to the start of the patent box tax regime and without that they would have declined. Net assets were up, however, as were operating cash flows with plenty of free cash being generated. The non-touch business is dwindling due to a reduction in ATM display orders but the touch screen business is performing OK as strength in gaming orders was partially offset by continued declines in vending sales to Coca cola and French industrial sales declining.

There seems to be a decent pipeline of new products coming on stream but the main problem here remains the large, lumpy orders. This year has been saved by the large Korean gaming contract, without which performance would have been poor. There is a great deal of net cash here though which means the forward PE of 14.3 is not too taxing and the yield of 4.1% is a decent incentive. I remain a holder here.

On the 16th February the group released an AGM trading update where they stated that trading had continued to be ahead of the previous year and remained in line with management expectations.