Fairpoint has now released its interim results for the year ending 2016.

Revenues increased when compared to the first half of last year as a £2.6M decline in IVA revenue, a £1.3M decrease in debt management revenue and an £803K fall in claims management revenue was more than offset by a £10.2M growth in legal services revenue. Cost of sales also increased to give a gross profit £2.8M above that of last time. Amortisation increased by £129K and other underlying admin expenses were up £2.3M with £325K of acquisition costs also recorded which meant that the operating profit was broadly flat, increasing by just £77K. We then see a £314K reduction in the unwinding of the discount on IVA revenues and other finance costs increasing by £234K which meant that after tax charges declined by £96K the profit for the period came in at £655K, a reduction of £368K year on year.

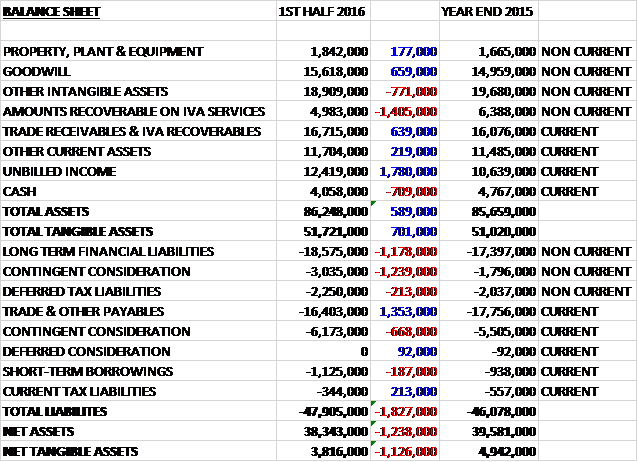

When compared to the end point of last year, total assets increased by £589K to £86.2M driven by a £1.8M growth in unbilled income, a £659K increase in goodwill and a £639K growth in receivables, partially offset by a £1.4M decline in amounts recoverable on IVA services a £771K fall in other intangible assets and a £709K decrease in cash. Total liabilities also increased during the period as a £1.4M decline in payables was more than offset by a £1.9M growth in contingent consideration and a £1.2M increase in long-term financial liabilities. The end result was a net tangible asset level of £3.8M, a decline of £1.1M over the past six months.

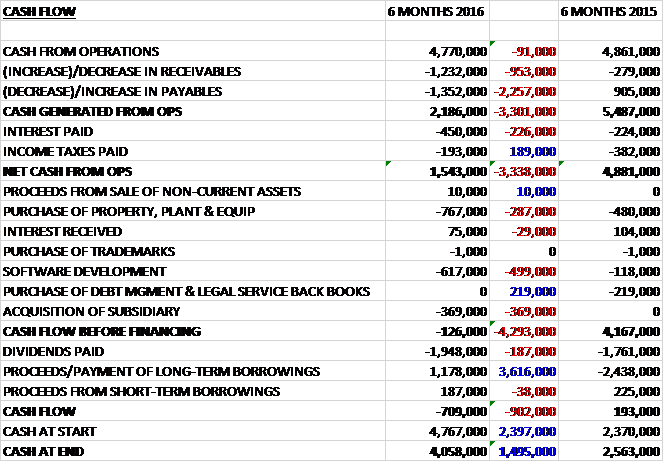

Before movements in working capital, cash profits were broadly flat, falling by just £91K. There was a cash outflow from working capital, partly reflected of working capital movements associated with the reduction in debt solutions activity, and after interest payments increased by £226K, the net cash from operations came in at £1.5M, a decline of £3.3M year on year. Of this £767K was spent on property, plant and equipment; £617K went on software development and £369K on an acquisition so that before financing there was a cash outflow of £126K. The group also paid out £1.9M in dividends and took out £1.2M of new borrowings to give a cash outflow of £709K and a cash level of £4.1M at the period-end.

The operating loss in the IVA division was £148K, a detrimental movement of £239K year on year as a result of fewer new cases as the group refrained from spending on uneconomic marketing activities in debt solutions. The total number of fee paying IVAs under management was 13,811 compared to 16,889 at this point of last year. The number of new IVAs written was 238 compared to 795 but the average gross fee per new IVA was £3,150 compared to £3,036. The portfolio of IVA cases continue to be cash generative and with debt solutions marketing on hold, the focus in this segment will be on cash generation.

The operating profit in the Debt Management business was £760K, a decline of £757K when compared to the first half of last year with a decreasing margin of 29% (compared to 39%) reflecting the decreasing profitability in this segment driven by the regulatory agenda which has increased call handling times, customer attrition and significantly increased risk and compliance overheads. The total number of DMPs under management was 13,252 compared to 20,730 with the orderly wind down of this segment as described below being underway and on track.

The operating profit in the Claims Management business was £263K, a fall of £129K when compared to the first half of 2015. As the claims management segment largely serves the IVA and DMP customer base, the lower profits are largely as a result of the declines in customer numbers in those areas.

The operating profit in the Legal Services business was £3M, a growth of £1.7M year on year on revenues that increased by 90% due to the Colemans acquisition last year (organic revenue was up 4%) despite conveyancing activity being impacted by the Brexit vote and election. During the period the group has focused its activity on investing in common processes, software and IT infrastructure, defining a pricing tariff for over 70 legal products and launching a new website. 80% of products are now administered on a single IT platform and they have extended the product range with the acquisition of a practice specialising in child abuse cases and substantial coverage has been achieved as a result of a new advertising approach.

Changes to the operation of whiplash claims relating to road traffic accidents have been proposed by the government. The board believes that its legal processing centre positions them advantageously to manage such legal work at low cost but the timetable for implementation appears to be lagging behind the scheduled start in April with the consultation process still awaited.

During the period the exceptional items of £325K relate to transaction and related professional services costs associated with the acquisition of a small legal practice specialising in child abuse cases.

David Broadbent has been appointed as CFO, replacing John Gittins who has now stepped down to pursue a portfolio career after having spent four years in the role. David joins from International Personal Finance where he served as finance director and chief commercial officer.

After the period-end, the group announced its decision to exist the debt management plan market due to regulatory changes impacting the whole sector. The FCA is driving a rigorous regulatory agenda in the DMP sector and this resulted in the decision to halt acquisition activity last year. The regulation has severely impacted the commerciality of the industry and has resulted in a reduction in profitability in the period. The ultimate outcome of the revised regulatory regime is expected to transfer competitive advantage to the charitable DMP sector, thus rendering the commercial DMP business model unsustainable. As a result, the group will conduct an orderly wind down of its DMP operations in the second half which will materially affect the results of the DMP segment as well as those of the claims segment given its dependency on selling services to DMP clients. DMP is now expected to make little or no profit contribution in the second half of the year.

It is expected that this restructuring will give rise to exceptional charges in the second half of about £2.5M, of which £1M will be cash outflow in 2016. The decision to exit the DMP market will also give rise to a non-cash impairment of the debt management intangible asset of £5.5M. From 2017 they will implement and benefit from a reduced cost base and a simplified business model focused on the legal services segment.

The group has also taken the decision to put market activity for IVA solutions on hold. The market conditions for debt solutions are likely to continue to be difficult until bank rate increases adversely affect the financial circumstances of home owners who typically have higher incomes which looks unlikely in the short term.

Currently the majority of legal services are trading in line with expectations but conveyancing volumes have been impacted by a slowdown in housing market transactions as a result of Brexit so the expectations for conveyancing has been adjusted materially downwards. Overall the group’s performance in H2 is likely to be similar to H1.

At the period-end the group had a net debt position of £15.6M compared to £5.2M at the same point of last year. At the current share price the shares are trading on an underlying PE of 4.9 but I can’t find a forecast for this year. After the interim dividend was maintained the shares are yielding 44.7% but obviously this won’t be maintained and once again I can’t find a forecast.

On the 10th October the group announced that Peter Watson, MD of Simpson Millar, sold 27,778 shares at a value of £20K.

On the 9th December the group released a trading update where they stated that trading in legal services in 2016 was in line with expectations to the end of October but the results for November are below plan and they are likely to be lower than expected in December as well. Trading across debt services is broadly in line with expectations and the closure of the debt management business remains on track for completion in early 2017. The planned benefit of the reduction in associated overheads is taking longer than expected, however.

As a result of these factors, the full year results for the group are likely to be materially below market expectations. The board is formulating plans to mitigate the potential impact on the financial performance of the group going forward, including the suspension of future dividends.

On the 28th December the group announced that CEO Chris Moat is stepping down with immediate effect. He will continue to provide continuing assistance on the closure of the DMP business. Non-executive Chairman David Harrel will assume the role of Executive Chairman alongside David Broadbent, CFO, who will assume a broader range of responsibilities on a temporary basis with the search for a new CEO underway.

So, things seem to be unravelling here. For what it’s worth in the first half profits were down along with net assets and operating cash flow with no free cash being generated. The IVA business has declined as interest rates remain low, the debt management business is in terminal decline and is being closed and as the claims management business relies on those, it is also suffering. The profit in the legal services business did increase but this seems to have been due to the Colemans acquisition and subsequently performance has deteriorated, presumably as a result of reduced conveyancing business. The CEO has now gone as has the dividend yield and with all parts of the business in free-fall I can’t see these as good value even at these low levels.

On the 28th March the group released an update covering 2016 results. It is expected that revenue will be £52.9M and adjusted pre-tax profit will be £4.9M, a decline of £5.6M year on year. The was an increase in legal services revenue as a result of the full year benefit of the Colemans acquisition offset by the expected significant reduction in revenues in the Debt Solutions division. There was an increase in admin costs of £4.9M which principally reflected the acquisition of Colemans.

The cost of exceptional items and impairment of acquired intangible assets is expected to be £11.8M comprising costs of £2.8M relating to the exit from the debt management business and £9M of impairments in respect of the debt solutions business. As previously announced, following the difficulties experienced in the year the board decided to suspend future dividends. Bet debt at the year-end was £19.9M compared to £13.6M in 2015.

In February 2017 the MOJ announced draft legislation which would result in an increase in the small claims track limit to £5K for road traffic accident claims and to £2K for other personal injury claims together with a range of other measures intended to address soft tissue claims arising from road traffic accidents. Essentially the changes mean that law firms will not be able to recover costs in affected cases from the losing party. The changes are expected to come into force in October 2018.

These changes are expected to have a potential impact of 4% of the group’s current legal services revenue, and it is expected that this impact will be largely mitigated through changes to pricing mechanisms and through improved operating efficiency.

David Broadbent, formerly the CFO, will assume the role of CEO and Mike Dunn will continue as interim CFO until a permanent replacement has been appointed.

Going forward, significant work has been performed over the last three months to improve the visibility of results and the forecasting of legal services revenues, including both billing and movements in work in progress. The analysis indicates that 2017 legal services revenues will be about 15% lower than in 2016. This reflects a reduction in the number of cases settling for value in 2017 and predominantly relates to complex personal injury cases which can take over four years to be closed. The performance of the division is then expected to improve from 2018 as a result of the current case load reaching maturity and an increase in the level of marketing spend to drive new business. Debt Solutions revenues will also decline as the group reduces its activities in that sector.

A restructuring exercise has started which is mainly focused on debt solutions and group overheads. It is expected that around £5M of annualised cost savings will be realised and the exercise is on track to complete by the end of March. The full benefit of the cost savings is not expected to be realised until the second half of 2017, however.

Overall, the performance in 2017 is expected to be well below 2016.

Management believes that the actions taken to reduce the cost base and improve operating efficiency coupled with the expected recovery in legal services revenue should deliver a much improved level of trading performance in 2018.

On the 29th March the group announced the disposal of its ancillary medico-legal business, PIX, for an enterprise value of £1.2M payable in cash. The business has been providing medical records, reporting services and disbursement funding support to certain departments of the group’s legal services division. The business was sold to Premex, whom the group has entered into a three year strategic partnership with for ongoing medical records and reporting services. The business made a profit of £100K last year.

Oh dear, this all sounds very dire. I am keeping well clear for now.

On the 28th June the group announced that it had been notified by its bank, AIB, that it is unwilling to provide the level of ongoing support requested by the company. As a result they are unable to sign off the audit of the accounts which means they are late publishing the annual report which means the shares have been suspended. They are currently in discussions with alternative providers of finance. This is another sorry tale but it seems the group is limping on for now at least.

On the 4th August the group announced that the ongoing support for their business outside the legal business is difficult due to the existence of the onerous lease on the head office which has an annual commitment of £1M for a further four years. As a result, the board have concluded that the holding company of the group is no longer able to continue trading as a going concern and has filed notice of intention to appoint administrators. Oh dear!