Avingtrans has now released their final results for the year ended 2016.

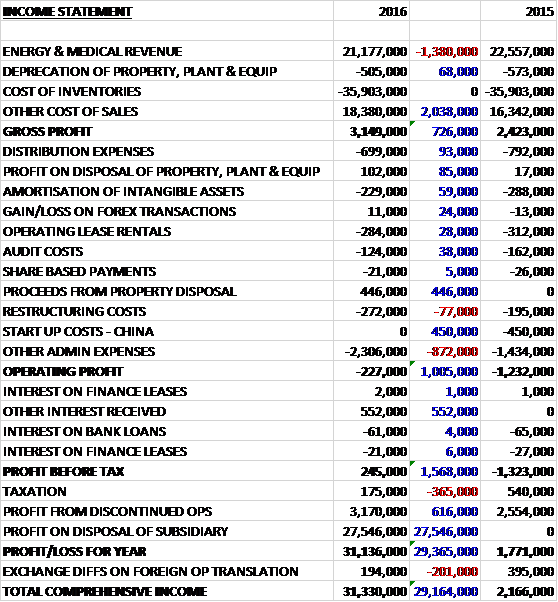

Revenues declined by £1.4M when compared to last year due to the continued subdued oil and gas market but cost of sales fell by £2M to give a gross profit £726K higher. Distribution expenses fell by £93K and there were small decreases in amortisation, operating lease rentals and audit costs with an £85K increase in profit on disposal of fixed assets. There was £446K in proceeds from a property disposal and no Chinese start-up costs which accounted for £450K last year but other admin expenses were up £872K to give an operating loss £1M down on 2015. The group received £552K in interest payments and but tax receipts fell by £365K with the tax position expected to normalise in the coming years, to give a profit from continuing operations of £420K, an positive movement of £1.2M year on year.

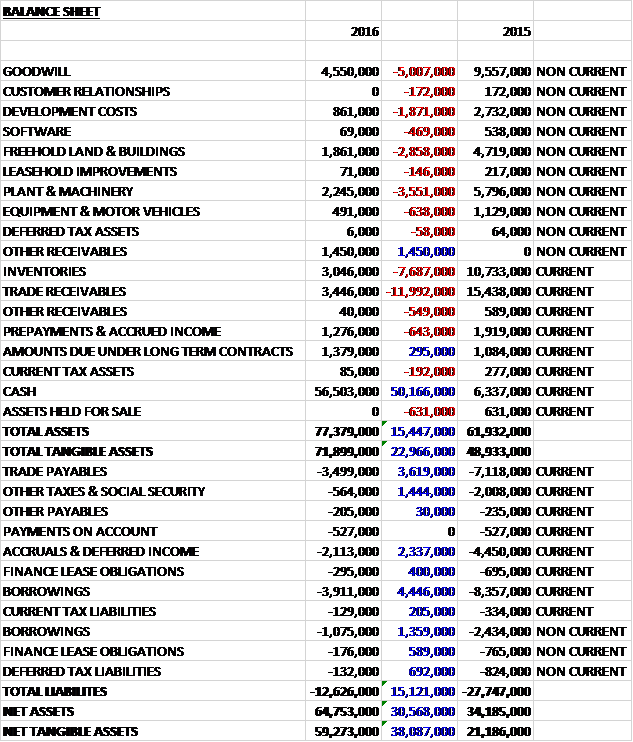

When compared to the end point of last year, total assets increased by £15.4M driven by a £50.2M increase in cash, partially offset by a £12M reduction trade receivables, a £7.7M fall in inventories, a £5M decline in goodwill and a £3.6M decrease in plant and machinery. Total liabilities declined during the year due to a £3.6M fall in trade payables, a £5.8M decrease in borrowings and a £2.3M decline in accruals and deferred income. The end result was a net tangible asset level of £59.3M, a growth of £38.1M year on year.

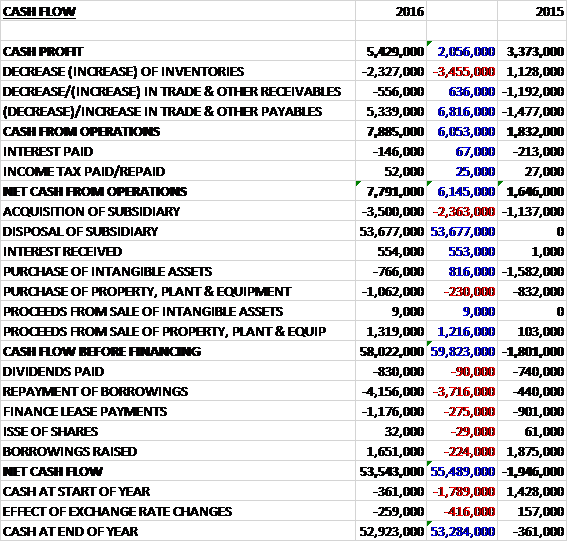

Before movements in working capital, cash profits increased by £2.1M to £5.4M. There was a cash inflow from working capital due to an increase in payables and after a small reduction in interest payments, the net cash from operations came in at £7.8M, a growth of £6.1M year on year. The group spent £3.5M on acquisitions but recouped £53.7M on disposals before spending £766K on intangible assets and receiving a net £257K from selling fixed assets. Before financing there was an income of £58M. The group paid out £830K in dividends, £1.2M on finance leases and a net £2.5M on repaying loans to give a cash flow for the year of £53.5M and a cash level of £52.9M at the year-end.

It is worth noting that there is one customer that accounts for more than 10% of total revenues which is always a risk.

The low oil price continued throughout the year, sapping any momentum in potential prospects for this sector, hence the downsizing of the Maloney business and the sale of the Aldridge manufacturing site. They have also countered the negative effects of the oil price, by focusing on the growth areas in the energy market such as energy storage, carbon capture and nuclear power life extension and decommissioning. The remaining effect of the oil price reduction mostly worked through Maloney in the period and whilst this supressed the revenue by 6% the underlying performance was a very modest profit for the year.

At Metalcraft Chatteris, business with Seamens and Cummins in the UK was steady and site delivery along with quality consistency were further improved. Pre-production activities started on the £47M ten year contract with Sellafield for the provision of 3M3 nuclear waste boxes, albeit that they have seen some changes to phasing of the production start-up. Whilst progress has been somewhat slower than anticipated the delays are not material for the project overall and they have made good progress with site preparations and pre-production tests. The production set-up and prototype testing will continue in the current year with series production expected to start next in the following year.

At Metalcraft Chengdu, results for the unit improved and they made good progress with the existing customers. The business won a £3M contract with Bruker for Nuclear Magnetic Resonance vessels and they have now begun preparations to start production of the Bruker systems in China later this year.

At Maloney Metalcraft, as already mentioned, the oil price effects continued to wash through the business leading to a loss at the site excluding the one-off sale of the building at Aldridge. There was a $2M contract win with HGC Gulf International, however, to supply gas treatment packages. The sector remains subdued but the recent £3.5M contract win with EDF shows that they have value beyond oil and gas.

Crown had a steady year in its core business. The Future Environmental Technologies partnership made progress during the year with the first carbon abatement project now running smoothly in Wales. This technology makes small to medium diesel generators “clean” which is important in a future where the energy grid is more fragmented and localised. Other projects with FET are now underway.

The retained part of the Composites business in Buckingham also made a loss for the year as the group extracted the aerospace related content to go with Sigma, and due to start-up costs for the £3M contract won with Rapiscan. By the year-end the business was running close to break-even with improving prospects.

The big event during the year was the disposal of the aerospace division which comprised Sigma Precision Components, C&H Precision Finishers and Hartshill Ventures for cash proceeds of £53.7M which generated a profit on disposal of £27.5M. The division made a profit of £3.2M in the year before being sold just before the year-end. Of the proceeds, £28M is being returned to shareholders by way of a tender offer.

Following the acquisition of the Rolls Royce pipe business the board felt that it had achieved the majority of the targets which it had set for the aerospace division and it was the right stage in its development to consider a disposal of the business. Subject to achieving an attractive valuation, they believed that shareholder value would be maximised over the long term by disposing of it and returning part of the proceeds to shareholders, with the group also reinvesting part of the proceeds into strengthening their position in the energy sector. They believe that the contract win by the energy business with Sellafield in 2015 demonstrated the significant opportunities available in that market if they were able to put more resources into that sector.

The disposal proceeds represent over twice the original shareholder equity invested in the business’ development. During the year they also sold the freehold of the Maloney Metalcraft building at Aldridge for £1.1M, limiting their exposure to the oil and gas market.

Due to the disposal the group had a net cash position of £51M at the year-end compared to net debt of £5.9M at the end of last year. At the current share price the shares are trading on a PE of 142.2 which increases to 172.1 on next year’s consensus forecast so unless I am missing something, these seem very expensive. After the final dividend was increased, the shares are yielding 1.7% which increases to 1.8% on next year’s forecast.

Overall then this has been a year of change for the group with the sale of the aerospace division, up to now the most profitable part of the company. Of the remaining business, the modest profit did increase although there was an operating loss. Net assets also increased due to the sale and the operating cash flow increased with decent amounts of free cash being generated (this is relating to the aerospace division too I think). The Sellafield contract is starting to ramp up but it looks to be at least another year until it contributes meaningfully and the delays already experienced are a bit of a concern. There do seem to be a number of other smaller contracts being won but the shares are expensive on a PE basis and the forward yield of 1.8% is nothing to write home about.

Having said that, management here have had a history of creating shareholder value so it might be worth backing them to do it again?