Cranswick has now released its interim results for the year ending 2017.

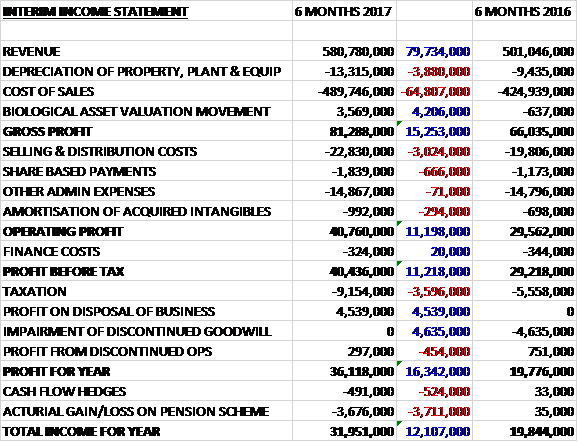

Revenue increased by £79.7M when compared to the first half of last year with £39.6M of that due to the Crown Chicken acquisition. Depreciation was up £3.9M and other cost of sales increased by £64.8M but there was a £4.2M positive movement in the value of biological assets to give a gross profit £15.3M above that of last time. Selling and distribution costs grew by £3M and share based payments were up £666K but other admin expenses were broadly flat to give an operating profit £11.2M ahead of last time. Finance costs were down £20K but tax charges increased by £3.6M to give a profit from continuing operations of £31.3M, a growth of £7.6M year on year.

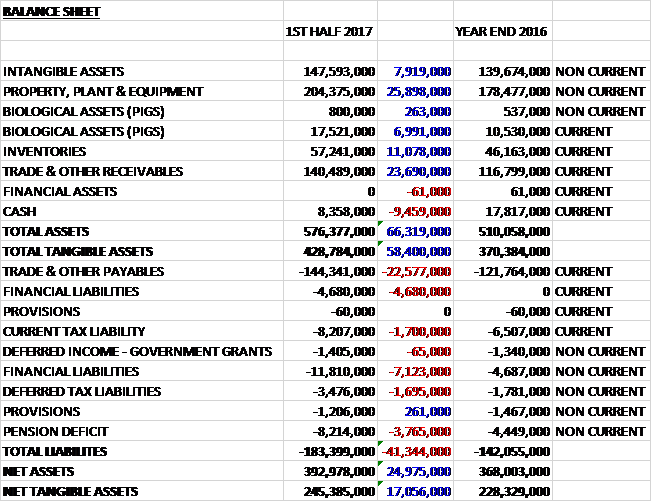

When compared to the end point of last year, total assets increased by £66.3M driven by a £25.9M growth in property, plant and equipment, a £23.7M increase in receivables, an £11.1M growth in inventories, a £7.9M increase in intangible assets and a £7.3M growth in the value of the pigs, partially offset by a £9.5M decline in cash. Total liabilities also increased during the period due to a £22.6M growth in payables, an £11.8M increase in financial liabilities and a £3.8M growth in the pension deficit. The end result was a net tangible asset level of £245.4M, a growth of £17.1M over the past six months.

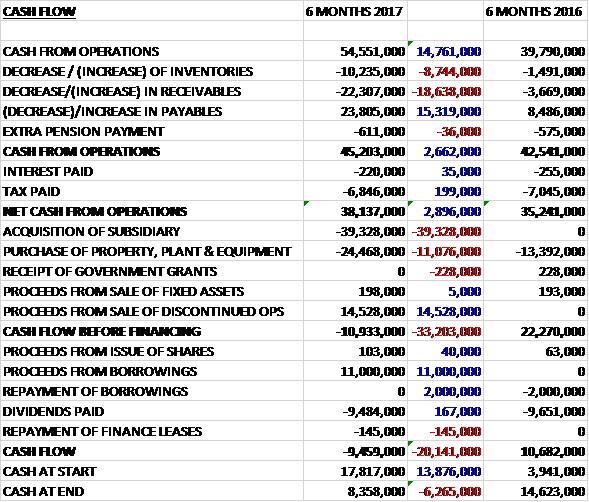

Before movements in working capital, cash profits grew by £14.8M to £54.6M. There was a cash outflow from working capital and after tax payments declined by £199K, the net cash from operations was £38.1M, a growth of £2.9M year on year. The group spent £24.5M on property, plant and equipment along with £39.3M on acquisitions but did receive £14.5M from the sale of discontinued operations to give a cash outflow of £10.9M before financing. After £11M was drawn down in borrowings to pay the £9.5M of dividends, there was a cash outflow of £9.5M and a cash level of £8.4M at the period-end.

Underlying revenue grew by 8% with corresponding volumes ahead 16% as the benefit of lower input prices in the early part of the year was passed on to customers. New contract wins and a greater number of pigs being processed underpinned the volume growth. Pig prices increased sharply during the period, particularly during Q2. The UK price rose 25%, but was on average still 5% lower than during the same period last year. The steep rise reflected an even more pronounced increase in its European equivalent of 41% resulting in the EU reference price reaching parity with the UK price by the period-end. The principal reason for the uplift was strong demand for European pig meat from China.

Improvements in productivity together with the rising pig price resulted in an improved contribution from pig production compared to the same period last year. Total export volumes grew by 23%. Volume growth to Far Eastern markets of 37% together with an 11% increase into the US was offset by a 4% decline in sales to other export markets. The strong growth in shipments to the Far East reflected an increase in pig numbers processed at the processing facilities and growth in the number of products being supplied.

Fresh pork revenues grew by 3% with volumes up 10%, driven by strong export growth, a buoyant wholesale market and the benefit of new, long-term retail contracts. The number of British pigs processed increased by 9% in the period against market data highlighting that UK retail fresh pork volumes fell 3% year on year with much of this decline due to lower promotional activity. The next phase of redevelopment of the Norfolk facility was completed shortly after the period-end. The £6M investment is to replace the previous abattoir has increased capacity, improved efficiencies and will facilitate the site’s push for USDA accreditation.

Sausage sales were 16% higher with volumes ahead by 40%. New contract wins with the group’s two largest retail customers for their “Butcher’s Choice” ranges, with together delivered 350 tonnes of incremental volume, underpinned this performance. Sausage production restarted at the Norfolk facility during the period to meet the increase in demand. Sales of premium beef burgers from the Lazenby’s facility also grew strongly with volumes up 24%. New mixing and blending equipment has been commissioned to support the next phase of growth and development of the facility, new product launches and increased volumes of festive garnish ranges will ensure the site has a busy run in to Christmas – over 40M pigs in blankets are being produced this year, double last year’s total.

Bacon sales were 4% lower despite strong volume growth of 8% as lower input prices were passed through to customers. The premium bacon sector continues to outperform the overall category, but slower year on year growth than in previous periods highlighted the recent trend by retailers to move away from promotional mechanics and multi-buy offers.

Cooked meat sales increased by 13% with volumes 17% higher reflecting new business wins coming on stream. Three major new contracts, with business secured for the long term and with built in pricing models to address raw material price movements, leave the cooked meats category in good shape heading into H2. The ongoing capital investment programme resulted in £13M being spent across the three cooked meats sites during the period to upgrade facilities, add capacity and introduce new capability to produce slow cook, sous vide, food on the go, and BBQ ranges which have been added to the portfolio of products following recent contract wins.

Sales in Crown fresh poultry grew by 8.3% in the period since acquisition compared to the same period in the prior year reflecting strong volume growth. The business is being integrated successfully and is forging strong links with their premium cooked poultry and pig farming operations.

Sales of premium cooked poultry grew by 13% supported by a 22% uplift in volumes. The £9M capital investment programme which was completed at the start of the current financial year has enabled new business to be secured and produced more efficiently by using the latest in-line cooking and spiral chilling techniques. This category is perfectly suited to the latest customer trends which are focused on quick, easy, healthy and tasty meal solutions, with convenient protein a core component. Latest market data shows the UK cooked poultry category has grown at 4% over the last year, and that growth is accelerating.

Sales of continental products increased by 14% with volumes up 18%. The business continues to source new products from a complex array of suppliers across the Mediterranean region. The Made in Manchester concept highlights the significant value add that the experienced and innovative teams at the two Manchester facilities bring to the fast growing category. The two facilities are now operating at full capacity. To enable the business to continue to grow, a new £25M facility will be built in the NW of England which will consolidate production from the two existing sites. The new site, based in Bury, will increase current capacity by about 70% and will enable the product ranges to be produced more efficiently.

Pastry sales were 1% ahead of the prior year in revenue terms with volumes 4% lower. Further improvements in operational performance at the site supported the modest sales growth in what is the quietest part of the year. New product lines continue to be launched and these, together with a strong Christmas and seasonal promotional programme, leave the business well placed to drive further volume growth moving into the second half of the year.

The group has spent a considerable amount on capex in the first half and future capex under contract stands at £10.4M compared to £4.3M at this point of last year.

In April the group acquired Crown Chicken for a cash consideration of £43.3M, generating goodwill of £12.9M. The principal activities of the business are the breeding, rearing and processing of fresh chicken, as well as milling grain for the production of animal fees. The acquisition provides the group with a fully integrated supply chain for its poultry business. In the six months since acquisition the business has contributed profit of £2.7M.

During the period the group disposed of its shareholding in the Sandwich Factory to Greencore for £16M, including £1M of contingent consideration. The disposal gave rise to a profit of £4.8M and the business made a profit of £297K during the period. At the end of the period the group had a net debt position of £2.9M compared to a net cash position of £17.8M at the end of last year.

In November, after the period-end the group acquired Dunbia Ballymena for an initial cash consideration of £16.9M and a further contingent consideration of up to £1.3M. The principal activity of the business is primary pork processing and the acquisition enhances the group’s pig processing capability and establishes a significant presence in Northern Ireland.

Going forward the board believe that the group remains well positioned to deliver their expectations for the current year.

At the current share price the shares trade on a PE ratio of 24 which falls to 20.4 on the full year consensus forecast. After a 13% increase in the interim dividend the shares are yielding 1.6% which increases to 1.8% on the full year forecast.

Overall then this has been another strong period for the group. The profit increased, net assets grew and the operating cash flow increased, although after acquisitions no free cash was generated so this is very much still in the growth stage. Most categories performed well with just bacon and pastries showing no or negative growth with the former due to lower sales prices and the latter down to lower volumes. The group is investing a lot in capex and acquisitions at the moment which is good, but I feel that perhaps they shouldn’t bother with the limited dividend on offer here. This is all good but the forward PE of 20.4 and yield of 1.8% definitely prices this in so these look a bit expensive to me at the moment, not leaving much margin for error.

On the 2nd February the group released a Q3 trading update which was in line with board expectations. Total revenue was well ahead of last year, underpinned by strong volume growth and supported by a robust performance over Christmas. Export sales continued to grow strongly, with Far East revenues well ahead reflecting both ongoing demand from the region and increased output from the group’s two primary processing facilities. Input costs rose further during the period buy efficiency improvements, internal pig production and constructive pricing discussions with customers helped partially mitigate the impact.

Dunbia Ballymena performed in line with expectations since the acquisition and integration is proceeding to plan. Crown Chicken continued to contribute strongly during the period. The business is being integrated successfully and is forging strong links with the premium cooked poultry and pig farming operations.

Work has recently started on the new, purpose built continental products factory in Bury. This substantial investment will consolidate the group’s two existing facilities and provide additional capacity to support this growth category.

Net debt increased during the quarter and was above the level reported at the same stage last year. The board is confident in both the prospects for the remainder of the year and the continued long term success of the group. This all sounds fine – the increasing input costs could be the sign of an issue though.