Pan African Resources has now released its final results for the year ended 2016.

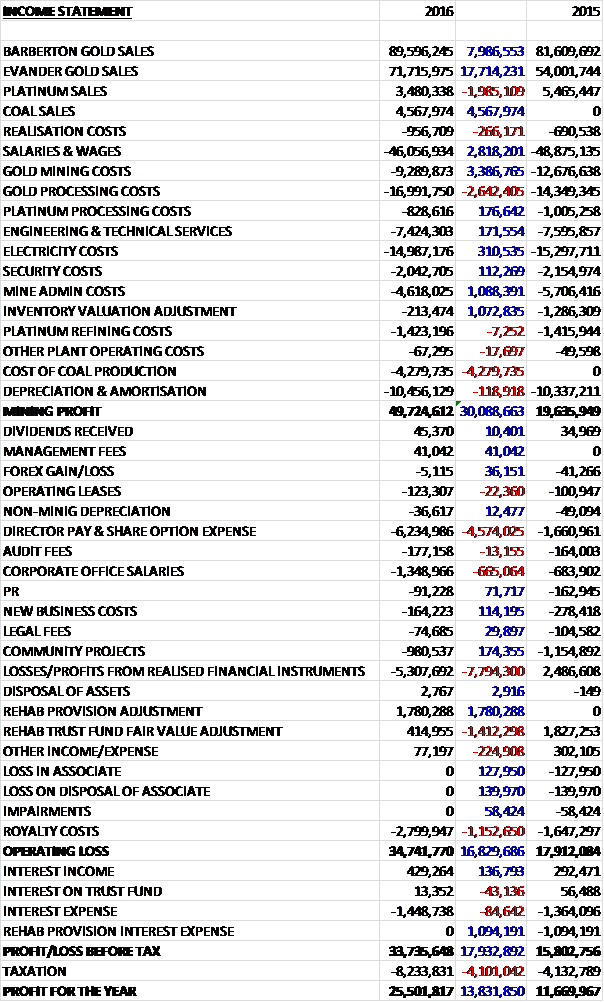

Revenues increased when compared to last year as a £2M decline in platinum sales was more than offset by a £17.7M growth in Evander gold sales, an £8M increase in Barbeton gold sales and a maiden £4.6M contribution from the coal business. Salaries and wages fell by £2.8M, gold mining costs fell by £3.4M but gold processing costs increased by £2.6M. Mine admin costs declined by £1.1M and there was a £1.1M improvement in the inventory valuation adjustment but we see the first £4.3M of coal production costs to give a mining profit £30.1M above that of last year. Director pay and share option expenses increased by £4.6M, not helped by the increase in the share price and corporate office salaries increased by £665K. We also see a £7.8M increase in losses from realised financial instruments, a £1.4M reduction in the rehabilitation fund value increase, and a £1.2M growth in royalty costs, offset by a £1.8M positive rehabilitation provision adjustment which meant that the operating profit increased by £16.8M. After the lack of £1.1M of rehabilitation provision interest expense and a £4.1M increase in tax payments the profit for the year came in at £25.5M, a growth of £13.8M year on year.

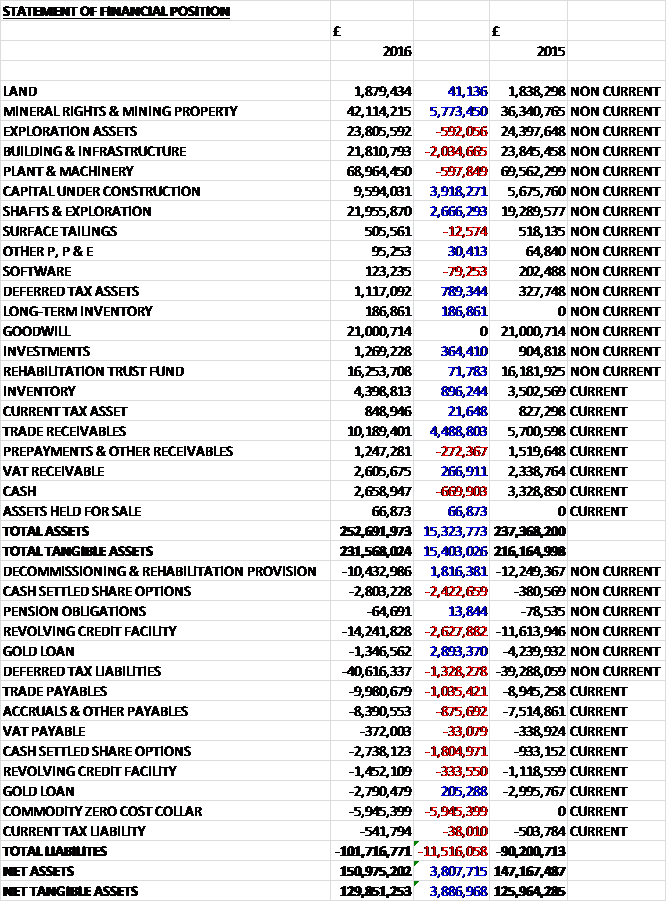

When compared to the end point of last year, total assets increased by £15.3M to £252.7M driven by a £5.8M increase in mineral rights and mining properties, a £3.9M increase in capital under construction, a £4.5M growth in trade receivables and a £2.7M increase in the value of shafts and exploration, partially offset by a £2M decline in the value of building and infrastructure. Total liabilities also increased during the year as a £5.9M increase in the commodity zero cost collar, a £2.9M growth in the revolving credit facility, and a £4.2M increase in cash settled share options, partially offset by a £2.9M reduction in the gold loan. The end result is a net tangible asset level of £129.9M, a growth of £3.9M year on year.

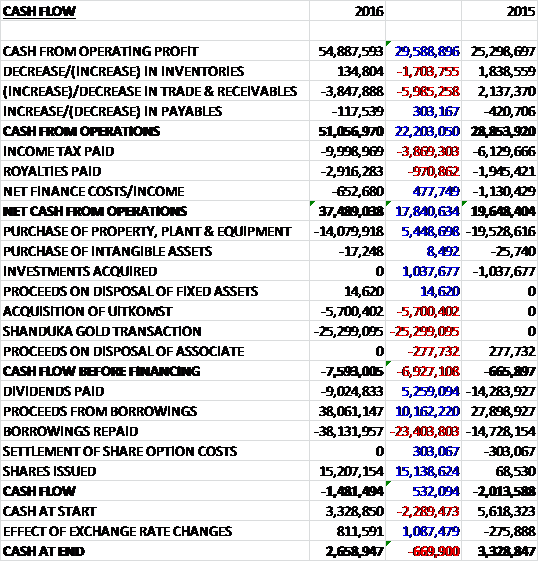

Before movements in working capital, cash profits increased by £29.6M to £54.9M. There was a cash outflow from working capital with an increase in receivables and tax payments increased by £3.9M with a £970K growth in royalty payments to give a net cash from operations of £37.5M, a growth of £17.8M year on year. The group spent £14.1M on property, plant and equipment, £5.7M on the acquisition of Uitkomst and £25.3M on the Shanduka Gold transaction which meant that there was a cash outflow of £7.6M before financing. The group also spent £9M on dividends so issued new shares to raise £15.2M to give a cash outflow of £1.5M and a cash level of £2.7M at the year-end.

The group delivered record gold production with gold sales increasing by 16.5% to 204,928oz and but the effective gold price declined from $1,212 per ounce to $1,164 per ounce with all-in sustaining costs per ounce decreasing from $1,093 to $870. At the end of the year the gold spot price closed at $1,325 per ounce.

The mining profit at Barbeton was £40.2M, a growth of £13.5M year on year. Underground head grades improved from 10.9g/t to 11g/t with the amount of gold sold increasing by 7.1% to 113,281 ounces. There was £1.3M of one-off expansion capex relating to the Royal Sheba development costs and the completion of the BTRP power line extension and installation.

The mining profit at Evander was £9.7M, a positive movement of £18M when compared to last year with a 31% increase in production. Underground head grades improved from 4.6g/t to 5.7g/t due to establishing mining on 8 Shaft’s new 25 level. In addition the tailings retreatment plant assisted their production growth by achieving full nameplate capacity, producing 18,151 ounces of gold from tailing and surface feedstock out of a total of 91,647 ounces in the mine as a whole. The all in sustaining cost per ounce decreased from $1,380 to $1,023 and there was £365K of one-off expansionary capital relating to development costs associated with 8 Shaft’s 26 level.

Following the receipt of a positive high-level economic and technical assessment of the Elikhulu tailings retreatment project at Evander, the group is undertaking a definitive feasibility study which should be available in November 2016. The project will potentially treat slimes at a processing capacity of up to 12MT per annum at a head grade of 0.29g/t. The total mineral resource is 178.7MT at 0.29g/t with a life of operation of about 14 years and 1.7Moz of contained gold. The project is estimated to yield about 50Koz of gold per annum in the initial eight years of production while treating the Kinross and Leslie tailings storage facilities and then about 38Koz per annum from the remaining six years from processing the Winkelhaak tailings storage facility.

The mining loss at Phoenix Platinum was £288K, a detrimental movement of £1.6M when compared to 2015. The operation’s performance was hampered by the business rescue proceedings announced by IFM in August last year as well as the drought and water shortages affecting re-mining and processing. Samancor Chrome was the successful bidder for IFM’s assets and the group have reached an agreement with them, assigning the tailings treatment to them. Although the agreement doesn’t guarantee current arising feedstock to Phoenix – this will be dependent on how TC use the assets – it places Phoenix in a better position where it should be able to continue operations under similar conditions to those prior to the business rescue proceedings. Further, it ensures that Phoenix’s operations are safeguarded and they also have alternative sources of feedstock which are currently being processed.

Uitkomst made a maiden mining profit of £140K this year with 87,538 tonnes of coal produced from its underground operations and acquiring 48,564 tonnes of coal for further processing and blending, resulting in total coal sold of 136,102 tonnes. The group assumed effective control of the mine at the end of March for £9M. The mine produces between 30K to 35K tonnes of coal per month from its underground mining operation and has an estimated life of mine of 22 years at current production rates. The average revenue per tonne received was $48 whilst the cost per tonne was $45.

Locally conditions remain challenging. South Africa faces a possible sovereign credit rating downgrade to sub-investment grade as well as heightened political tension which could lead to further depreciation in the Rand.

During the year the group’s total gold resources increased by 9.4% to 34.9Moz but reserves decreased from 10.4Moz to 10Moz with a plan to increase these reserves in the next year. Platinum reserves decreased from 0.5Moz to 0.2Moz with resources remaining static whilst coal resources were recorded at 23.3MT.

Shanduka Gold is the group’s primary BEE shareholder with its sole assets being a 22.5% interest in PAF’s issued share capital and a notional vendor loan of R558M to its BEE shareholder, the Mabundu Trust. During the year the group acquired 49.9% of Shanduka but consolidates the full interest for accounting purposes.

At the year-end the group had a net debt position of £17.2M compared to £16.6M at the end of last year. At the current share price the shares are trading on a PE ratio of 9.4 which falls to 6.4 on next year’s consensus forecast. After the dividend was increased, the shares have a yield of 5.2% which increases to 5.7% on next year’s forecast.

On the 27th September the group announced that CEO Cobus Loots purchased 248,609 shares at a value of about £55K. Following the transaction he holds 480,184 shares. It was also announced that Finance Director Deon Louw purchased 137,450 shares at a value of £30K which represents his maiden share purchase.

On the 5th December the group announced the results of the feasibility study for the Elikhulu tailings project along with a production update. The board have approved the construction of the project with the planned start date being January 2017 with first gold forecast for Q4 2018 calendar year and full commissioning in December 2018. Annual recoverable gold of 56,000 ounces is expected for its initial eight years and 45,000 ounces for the remaining five years. Optimal plant capacity for the project allows 12M tonnes per annum throughput and the project is expected to add about 25% to the group’s production and reduce the all-in sustaining cost profile. The initial capital cost is expected to be about $120M and the project has a payback period of less than four years based on a gold price of $1,180 per ounce.

Rand Merchant Bank has provided the group with all necessary approvals for a £60.9M five year debt facility with will be dedicated to the funding of the project and will be repaid from the project’s cash flows generated during the initial five years of production. The group are evaluating a number of funding proposals to fund the balance of the initial capital requirement and do not expect any difficulty securing the balance on competitive terms. As the repayment profile is matched to the project’s cash flow generation, it is not expected to impact on the existing dividend policy.

The project entails establishing facilities and infrastructure at Evander to retreat gold plant tailings at a rate of 1M tonnes per month in addition to the existing production from the ETRP which will continue to operate independently to the project for the next 13 years. Three existing tailings storage facilities will be reclaimed.

In 2017, the capital requirement will be $50.2M with a further $69.7M required in 2018 which includes a contingency of $13.2M over those two years. There will then be a further requirement of $21.6K in 2021 and $7.8M in 2026 which is required to re-establish the hydro-mining infrastructure.

Phase 1 of the hydraulic mining at the Kinross tailings storage facility is scheduled to start in Q4 of the calendar year 2018 with commercial production expected to be reached in December. The project is expected to have an AISC of $523 over the life of the project and is expected to be highly cash generative from the start ($45.7M in 2019, tailing off a bit in subsequent years).

In the first half of the year, Barbeton is expected to produce 49,000 ounces, a reduction of 13% year on year with Evander falling by 7.4% to 42,000 ounces. Uitkomst is expected to produce 330,000 tonnes of coal and Phoenix production is expected to increase by 9.1% to 4,900 ounces of platinum. The previously guided gold production of about 200,000 ounces for 2017 is being revised down to 195,000 ounces with gold production in H2 being higher than in H1. This is in light of challenges experienced with the operational environment and underground operations in recent months.

Evander Mine’s 7 Shaft which is used to hoist ore from underground operations to the surface for processing is undergoing critical maintenance following the dislodgement of a steel shaft guide which damaged the shaft infrastructure. Even through primary repairs have been completed, the hoisting speed is curtailed until the full maintenance programme is completed with normal hoisting expected to be resumed in January. The mine experienced a material increase in safety stoppages during the past five months. The operation will issued with four regulatory notices which resulted in 13 lost production days compared to two lost days last time with the majority of these related to the Shaft 7 incident.

At Barbeton, three separate community protests relating to unrest as a result of poor government service delivery in the area and competing recruitment of interests from lobby groups was experienced which resulted in six days of lost production. Union related demands resulted in workers embarking on a go slow which also affected productivity.

Fairview mine experienced flexibility issues, specifically at its very high grade 11 block. Work is underway to develop a new production platform. Further flexibility improvements will be achieved via a new decline under development and a new refrigeration plant will also improve working conditions in this area. Six Section 54 regulatory notices which resulted in eight lost production data were encountered compared to three lost days last time.

At Uitkomst, production and performance remained in line with expectations. The colliery has also bought in additional coal from neighbouring mining operations to optimise its washing plant’s operations. If the current favourable coal price environment continues, the payback period for this acquisition is expected to be less than four years.

Phoenix Platinum processing capacity has increased from 25,000 tonnes per month to 30,000 tonnes following the installation of a scrubber in July 2016. The operation has experienced water constraints due to the persistent drought conditions during October and November but despite these challenge, production is expected to increase by 9.1% to 4,900 ounces in the first half.

Overall then this year has been very strong for the group. Profits increased, net assets grew and the operating cash flow improved, although no free cash was generated after the Shanduka Gold transaction was taken into account. The group produced 205K ounces of gold and although the sales price fell slightly to $1,164 per ounce, the cost per ounce declined even more, down to $870 per ounce. Both main mines saw their performance improve with Evander showing particularly good improvements due to better grades and the start of the retreatment plant operations. Phoenix Platinum fared less well due to the business review proceedings against IFM and water shortages.

So far in 2017, things have not gone quite as well, however. The Evander mine shaft failure and unrest at Barbeton mean the group is likely to produce less gold than last year and I suspect costs will have increased too. The Elikhulu tailings project also increases the risk here with substantial amounts of debt being taken on to fund it, although if all goes to plan it should be a good contributor going forward. The gold price is now about $1,203 per ounce so the group should be making decent money at this level so I guess the issue is, does the forward PE of 6.4 and yield of 5.7% sufficiently compensate for the increased risk associated with Elikhulu and the operational problems at both main gold mines experienced in the first half of 2017? I think they just about do…

On the 27th January the group released a trading update covering the first six months of the year. There was a 14% appreciation in the ZAR/GBP exchange rate during the period. EPS is expected to between 23% and 43% higher than last year in ZAR terms and between 45% and 65% higher in GBP terms. This is helped by the earnings accretive Shanduka transaction which reduced the number of shares in issue by 17.7%.

The Uitkomst Colliery, acquired in March, has performed well during the period, contributing about 8.5% of the group’s EPS. If the current favourable coal price environment continues, the payback period for this acquisition is expected to be less than the four years previously forecast.

Barberton Mines entered into a short tem gold price hedge in July 2015.

During the current period, the group recorded a pre-tax mark to market fair value gain of £5.3M due to a reduction in the gold price with the group receiving an average of $1,257 per ounce in the period.

During the period gold production at Barberton fell 12.8% to 49,212 ounces; Evander mines declined by 6.5% to 42,401 ounces and platinum production at Phoenix grew by 1.8% to 4,575 ounces. The Uitkomst Colliery contributed 327,202 tonnes. The gold production in the second half is forecasted to exceed the first half performance.

Overall then the performance is not bad but it seems that Uitkomst and sterling depreciation is masking a less than stellar performance at the gold mines.

On the 20th February the group announced that in conjunction with the 7A shaft refurbishment programme, they initiated a number of studies to assess the conditions of the infrastructure which identified critical issues requiring remedial action to ensure safe and sustainable operation of these shafts.

The nature of these refurbishments require a suspension of Evander’s underground mining operations for up to 55 days but the tailings and surface operations will be unaffected. The cost of the programme is expected to be about £2.5M which will be funded from existing banking facilities. In light of these developments, the group have revised its gold production guidance for 2017 from 195,000 ounces to 181,000 ounces.

Overall this doesn’t sound great but should be a temporary issue.