Northern Petroleum has now released its interim results for the year ending 2016.

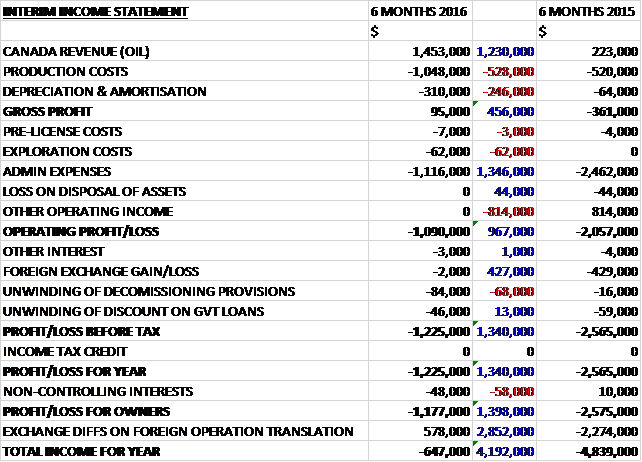

Revenue grew by $1.2M when compared to the first half of 2015 and after product costs increased by $528K and depreciation grew by $246K the group made a small gross profit of $95K, an improvement of $456K. Exploration costs grew by $62K and other operating income was down $814K but admin expenses declined by $1.4M to give an operating loss $967K below that of last time. After a $427K detrimental movement in forex the loss for the period came in at $1.2M, an improvement of $1.4M year on year.

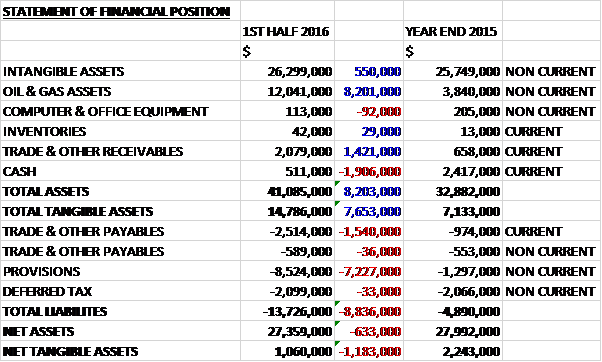

When compared to the end point of last year, total assets increased by $8.2M driven by an $8.2M growth in oil and gas assets due to the Canadian assets acquired and a $1.4M increase in receivables, partially offset by a $1.9M decline in cash. Total liabilities also grew during the period due to a $7.2M increase in provisions relating to the decommissioning provision of the acquired Rainbow Assets, and a $1.6M growth in payables. The end result was a rather precarious net tangible asset level of $1.1M, a decline of $1.2M over the past six months.

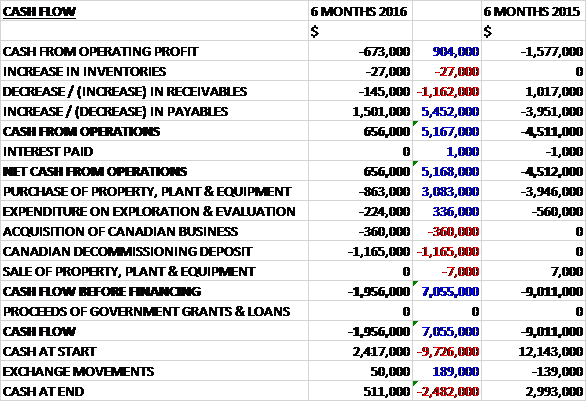

Before movements in working capital, cash losses improved by $904K to $673K. There was a cash inflow from working capital due to a large increase in payables so there was a net cash inflow of $656K during the period, an improvement of $5.2M year on year. The group spent $863K on property, plant and equipment along with $224K on exploration and $360K on acquisitions with a further £1.2M going on the decommissioning deposit although this was returned after the period-end due to the increase in production. There were no funding items so for H1 there was a cash outflow of $2M and a cash level of just $511K at the period-end.

The average oil price during the period was just $39 per barrel and the current production is about 390bopd, although average production in the period was 300bopd. The planned summer work programme completed with five wells being brought into production – three workover wells on production from mid-September and two waterflood wells recently started with oil rate expected to build in October. One well is currently suspended since August due to pipeline repair and is forecast to be back on production in October at about 50bopd.

The group is evaluating an opportunity with a local power generation company concerning a joint venture to produce shut-in gas within their leases to generate power both for operations and to sell to the local grid. The cash balance as of the end of September was $1M and the remaining $200K from the abandonment deposit is expected to be returned in October.

In January 2016 the Alberta Energy Regulator transferred a number of Rainbow area leases in Alberta to the group following a deposit of $1.2M. The rainbow assets include a total of 117 operated and 41 non-operated wells, of which about one third are either currently in production of are believed to have the potential of being brought back into production. The remaining wells are either suspended or already abandoned and will be reviewed for further production potential. The consideration of $360K is considered equal to the fair values of the assets so no goodwill has been generated.

When acquired, the assets were producing about 150 barrels of oil per day and contained 1.1M barrels of proven plus probable oil reserves. The acquisition included a number of wells, pipeline infrastructure and two production facilities with a direct tie-in to the national pipeline network. A small, low cost work programme of well and facility repairs was conducted through the remainder of winter and into spring, initially increasing the production to over 400bopd.

Production continued throughout Q2 with some downtime due to torrential rains during May and June which affected the wells not tied into the pipeline infrastructure due to trucking restrictions. With the increase in production during Q2 and despite the poor weather conditions, the group still averaged about 300bopd in the first half. They also secured contracts from local operators to process and ship their crude, generating additional income from the facilities.

In Italy, progress continued with the development of an environmental impact assessment for the drilling of the Giove appraisal well which is planned to be submitted before the end of the year. Onshore in the Po valley, Shell continued to evaluate the Cascina Alberto exploration permit in order to develop the additional seismic programme required to more thoroughly review the previously identified 300mmbls prospect. The group is carried by Shell for a 20% share of the Cascina Alberto permit, including seismic acquisition up to $4M and an exploration well up to $50M.

With production at the current level of about 400bopd, the group can sustain its financial position with an oil price of approximately $50 per barrel. As production grows, the Rainbow asset’s fixed cost base does not increase significantly so the operating cost increase per additional production barrel is less than $10.

The group is now developing a winter work programme to double production to 800bopd which will then provide free cash flow for investment. This will enable them to fund activities in Alberta and other areas such as the 3D seismic programme in Italy. Funding for this programme will be achieved through a combination of working capital, debt, a farm out and equity as is considered most appropriate at the time.

The group was loss making last year and the only forecast I can find has a loss this year too so PE ratio is not very useful.

On the 1st November the group released a Canadian reserves update following the acquisition of the Rainbow Assets and the investment programme undertaken to increase production. There are total proven plus probable reserves of 1.9mmboe with 1.3mmboe proven. Net present value of the proven reserves is about $16M with the total being $23M. This represents an increase in 2P reserves of about 30% since the last report with the increase in addition to the 0.155M barrels of production since the end of 2014 and a 20% reduction in forecast oil price.

On the 30th November the group released an update. They have agreed to divest some of their assets to High Power Petroleum for a consideration of $2.5M in cash and the application of $250K of well stimulation services. They have also announced a subscription to raise £5.1M at a price of 3.5p per share through a first tranche subscription of 124,047,017 new shares and a second tranche of 20,600,000. The issue price represents a premium of 12% to the closing price the day prior. They are also offering 21,500,000 shares to existing qualified shareholders top raise an additional £800K. Total funds realised from the disposal, the subscription and open offer will total up to $9.7M.

The disposal encompasses a 25% interest in all of the Canadian licenses, wells and facilities; a 10% interest in the group’s Italian offshore exploration permits and a 25% interest in their onshore Australian license.

They have also agreed to grant HP options to increase their interest in the assets with an increase to 50% of the Canadian assets for $4M before the end of 2017; an increase in the Italian assets to 50% by funding an appraisal well on the Giove oil discovery up to a cap of $15M; and increase to 50% in the Australian assets by funding $1M of seismic acquisition and processing.

The proceeds from the disposals, subscription and open offer will be used primarily to fund the group’s share of the forthcoming winter work programme in Canada and further production redevelopment in Canada in 2017 as well as the acquisition of 3D seismic in the southern Adriatic and the general working capital requirements of the group.

Overall then some progress actually seems to be being made here. During the period losses improved as did the operating cash flow, although this was only positive as payables increased. With the oil price around $50 the group can pretty much tread water but they now have a large injection of cash with which to develop some of the assets – they do seem to have given quite a bit away though. If all goes to plan, however, and production is upped to 800bopd then this is starting to look a bit interesting as a punt.

On the 1st February the group released an update covering the Canadian winter work programme, which has now started. About twenty wells that have been shut in for up to 18 years will be returned to production. The programme is expected to take two months and cost about $2.5M. The intervention work is focused on straightforward well operations, including the replacement of downhole pumps and rods, tubing upgrades and the re-perforation of existing zones. Two further wells have been chosen as recompletion candidates for the reinjection of produced water. Well stimulation using Blue Spark Energy WASP technology to improve production rates will be performed on selected wells with the programme overall expected to add more than 300bopd.

Average production last year more than doubled following the last winter work programme to 310bopd and current production is around 325bopd with five wells shut in for maintenance. The group’s cash balance at the end of January was $8.1M an additional $500K will be paid to them following regulatory approval of the sale of 10% of their Italian permits to H2P.

On the 1st March the group announced that Shell Italia has initiated a local engagement programme in relation to the Cascina Alberto permit. The programme is being undertaken in advance of the submission of an Environmental Impact Assessment necessary to conduct a geophysical survey. Field work for the seismic survey is expected to begin in 2018 following the approval of the EIA.

On the 2nd March the group announced that director Peter Stephens acquired 50,000 shares at a value of £19K. This is a drop in the ocean for him, however, as he now owns 1,513,500 shares in the company.

On the 8th March the group signed an agreement to acquire production wells and facilities located within the area of their existing Rainbow assets in Alberta. They will acquire 75% of the assets with High Power Petroleum acquiring the remaining 25%. The assets include six production wells, all shut in by the previous operator for being non-core; one water disposal well and injection pump; production facilities including which are tied into all the wells; two additional storage tanks; and direct sales and tie-in point to the Plains Midstream Pipeline network.

The first four wells to be brought into production either during the current winter work programme, if weather allows, or as part of a summer work programme. A further two wells will be considered for production reinstatement later in the year. The first four wells are expected to add a combined production rate of 75 barrels of oil per day initially.

The consideration for the acquisition is the assumption of the abandonment liability which is about $1.1M. The company therefore expects to deposit $700K which is forecast to be returned during Q3 as production increases. In addition, the vendor has waived the company’s liability in respect of a jointly owned well which is soon to be abandoned at a net cost of $22.5K. The processing facilities and sales tie-in point to the Plains Pipeline system will provide a useful second route to market to the existing sales tie-in point and can serve as backup if needed.

This seems like a decent, modest, acquisition.