Serabi Gold has now released its Q3 results for the year ending 2016.

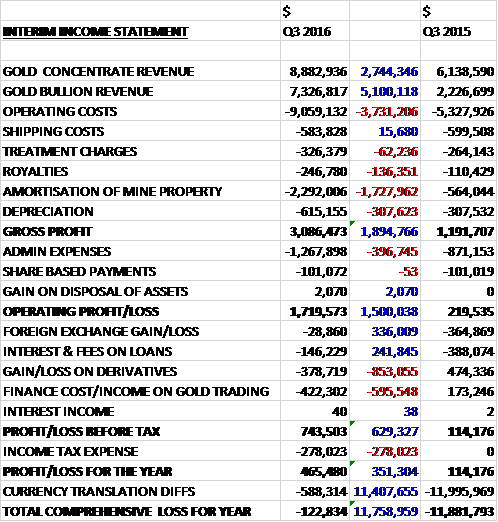

Revenues increased when compared to Q3 last year due to a $5.1M growth in gold bullion revenue due to an increase in Palito production and the fact that Sao Chico had not reached commercial production last year; and a $2.7M increase in gold concentrate revenue, in part due to the change in sales contract. Operating costs increased by $3.7M as Sao Chico’s costs were no longer capitalised and labour costs increased, amortisation charges grew by $1.7M both because Sao Chico entered commercial production and the new sales contract gave rise to a one-off amortisation charge due to the accelerated recognition of sales, and depreciation was up $308K to give a gross profit $1.9M ahead of last time. Admin expenses increased by $397K which meant that the operating profit grew by $1.5M. We then see an $853K swing to losses on derivatives relating to the Sprott and Fratelli call options and a $596K negative swing in gold trading costs relating to short term price differences between the contractual pricing arrangements with the end purchaser and the price ruling when the group draws down on the trade finance arrangement it has in place, along with a $278K tax charge which meant that the profit for the quarter was $465K, a growth of $114K year on year.

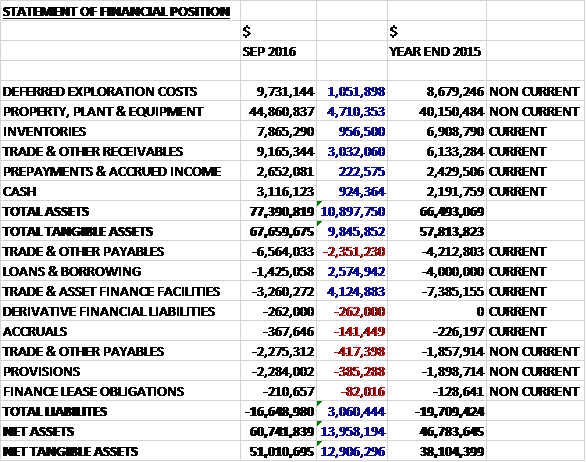

When compared to the end point of last year, total assets increased by $10.9M driven by a $4.7M growth in property, plant and equipment relating to both forex movements and additions, a $3M increase in receivables, a $1.1M growth in deferred exploration costs, a $957K growth in inventories and a $924K increase in cash. Total liabilities declined during the nine month period as a $4.1M decline in asset and finance facilities and a $2.6M fall in borrowings was partially offset by a $2.8M growth in payables relating to forex movements, higher production levels and increased salaries. The end result was a net tangible asset level of $51M, a growth of £12.9M over the period.

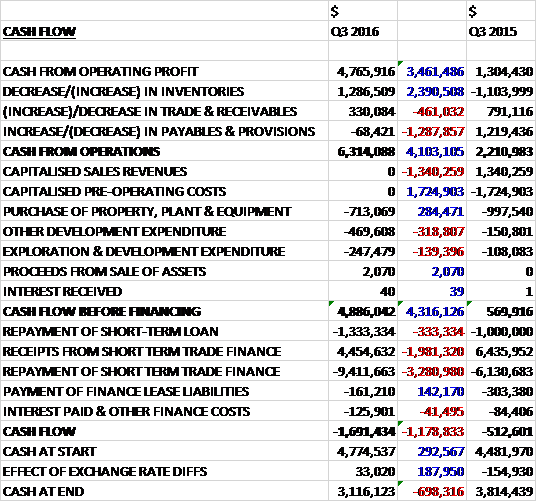

Before movements in working capital cash profits increased by $3.5M to $4.8M. There was a cash inflow from working capital, mainly due to a fall in inventories so the net cash from operations came in at $6.3M, a growth of $4.1M year on year. The group spent $713K on property, plant and equipment; $470K on development expenditure and $247K on exploration to give a free cash flow of $4.9M. They then repaid $1.3M of the loan and a net $5M of short term trade finance to give a cash outflow of $1.7M in the quarter and a cash level of $3.1M at the period-end.

During the first nine months of the year, the average gold price received was $1,256 per ounce. This compared to $1,156 received in the same period of the prior year. The average gold price in Q3 was $1,333 per ounce compared to $1,111 per ounce in Q3 last year). The total AISC of production was $951 per ounce compared to $894 last time. The group maintains its cost guidance for the full year of an AISC of $950 to $985 per ounce reflecting the continued strength of the Brazilian Real which has appreciated by 19% since March 2016.

During the quarter the group mined 43,133 tonnes of ore at a grade of 9.61g/t compared to 33,606 tonnes at 9.56g/t in the prior quarter. They milled 42,464 tonnes at a grade of 8.08g/t which produced 10,233 ounces of gold. This compared to 39,402 tonnes milled at 8.17g/t producing 9,896 ounces in Q2. The forecast gold production for 2016 as a whole is expected to be about 39,000 ounces. At Palito 31,916 tonnes was mined at 9.5g/t (25,198 tonnes at 10.48g/t in Q2) and at Sao Chico 11,217 tonnes was mined at 9.88g/t (8,408 tonnes at 6.81g/t).

At the end of the quarter, combined coarse ore stocks from the Palito and Sao Chico mines were about 11,000 tonnes with an average grade of 3.3g/t of gold compared to 14,800 tonnes at 3.66g/t at this point of last year.

At Palito, management expect that mine output for the year will be between 105Kt and 110Kt at an average grade of between 8.5g/t and 8.9g/t. During the year the group has focused on opening up new sectors in the mine as well as continuing to develop the existing sectors.

In September the group entered into a new contract for the sale of its copper concentrate. Under this new contract, the sale is recognised when the goods depart from Brazil whilst under the previous one the sale was only recognised when the goods arrived that the purchasers premises. Normally the group would recognise, on average, the sale of about 120 to 160 tonnes of concentrate per month but as a result of the new contract they recognised two shipments totalling 320 tonnes during September.

Further improvements were undertaken within the process plant during the year and a new carbon regeneration kiln is in the process of being installed and commissioned and will be operational during Q4. This kiln will regenerate fouled carbon reducing the need to purchase fresh carbon and is also expected to enhance gold recoveries.

Milling rates for ROM ore have increased by 23% to 438tpd so far this year. The introduction of the third ball mill at the end of June has had a significant effect on throughput rates with the average milling rate being 461tpd in Q3. The increase in processing rates also reflects the improvements in the operational efficiency of the process plant which has been assisted by the introduction of the gravity circuit and ILR for treating Sao Chico ore, reducing the levels of gold that would otherwise be treated in the CIP circuit. This improved efficiency has also allowed the rate of processing of the flotation tails to be maintained at similar levels to the corresponding period in 2015. The plant expansion is expected to provide sufficient extra capacity to process most of the stockpiled material of both coarse ore and flotation tails during the remainder of 2016.

At Sao Chico the main vein can vary from 1m to 8m wide but most commonly is a 2.5m alteration zone. The gold grades within the alteration zone are quite erratic and are hosted in three steeply plunging pay shoots. In these shoots the grades are often spectacular, in excess of 100g/t but outside the zones the vein is continuous but with low grades and as a result it is unavoidable that as the mine development passes between these areas, lower grade ore has to be mined. Whilst the alteration zone itself is readily identifiable the high grade zones are much less so therefore the mining operations require on-lode development at regular vertical intervals with regular channel sampling and in-fill drilling between these levels to best define the high grade gold mineralisation.

At Sao Chico, the mine develop has focussed on the central ore shoot of the main vein. The mine was primarily in development during 2015 and the early part of 2016 as the group sought to ensure that it secures a rolling medium production plan for up to two years into the future. It is only in the second half of 2016 that the level of stoping activity has begun to increase, and it is expected that the long term balance between development mining and stope mining rates will only be reached at the end of 2016 at which point management expect that monthly production rates will stabilise. The group is driving development east and west towards parallel vein structures that have been identified by surface drilling and they are confident that these ore shoots will provide additional mineable ore at Sao Chico.

Mine site geophysics studies undertaken during Q3 over the Currutela and Piuai discoveries and other areas close to the current Palito Mine have been designed to improve the drill targeting of a planned 2017 surface drilling campaign. Management feel that this campaign could provide sufficient confidence to justify the start of new mine portals and underground exploration drives to access and evaluate any new discoveries that are considered to be potentially commercially viable. In time these discoveries could become established as new near-mine satellite deposits adding incremental production.

All exploration has been on hold since the end of 2011 whilst the group concentrate its efforts ion bringing the Palito mine back into production. Whilst currently the immediate focus is to evaluate the near mine potential within two to three km of its existing operation, on a wider regional basis the group is developing plans to progress the evaluation of its whole tenement package. They have flown about 16,000 hectares of airborne VTRWM surveys but have limited funds and opportunity to follow up on many of the areas of interest. Conscious that the exploration tenements that they hold are only granted for limited terms, they are keen to implement, as and when adequate funding is available, a regional exploration programme to highlight those areas that should be prioritised.

It has always been the intention of the group to use cash flow generated from its production operations to advance its exploration opportunities. They will conduct DHEM in close proximity to the Palito mine and IP around Sao Chico during the second half of 2016 with the intention of using the results from these programmes to plan drilling campaigns that can be undertaken in 2017.

The group is paying off the Sprott loan and will repay the final $1.33M in Q4. In August Fratelli exercised their right to convert the outstanding $2M convertible loan – there is no more outstanding from that loan. During the period the group issued 42,312,568 shares following the decision of Fratelli to convert its $2M convertible loan into shares at a price of 3.6p per share.

The group made a loss last year so there is no current PE ratio but on the full year consensus forecast for 2016, the group is trading on a PE of 9.1.

On the 23rd January the group released an update covering Q4. In Q4, Palito produced 34,611 tonnes at a grade of 7.38g/t (down from 9.5g/t in the previous quarter) with Sao Chico producing 9,968 tonnes at 14.38g/t. 40,485 tonnes of ore was processed through the plant for the combined mining operations at a combined grade of 7.6g/t of gold which produced 9,413 ounces compared to 10,233 ounces in Q4 last year. At the year-end the combined surface stockpiles totalled 21,000 tonnes of ore at a grade of 4g/t. Despite the plant expansion to three ball mills, the easy and rapid ore development of the Senna vein due to its proximity to the surface, has meant increasing stock levels in the quarter.

At Palito the operation continues to perform steadily, although extracted mine grade during the quarter was lower than planned as a result of ore being cemented in two stopes. This ore is not lost and is being slowly recovered but not as fast as they had budgeted. The production shortfall was partially compensated by more development ore, albeit at a lower grade. The benefit of this is that the mine is now generating ore from four sectors with Senna playing an increasing role in the production plan. Production from stoping has not started there but in 2017 they will see a significant level of ore being produced from stoping at Senna.

At Sao Chico, ore production and development continued in line with plans and grades were excellent. The main ramp has now reached the 70mRL with the main vein intercepted.

In October and December the group suffered short-term breakdowns but were able to maintain throughput rates by having a third mill. An additional short term benefit of three mills operating has been the increased throughput capacity, allowing them to consume the low grade surface stock that had built up over the past three years.

At Senna, the results of the drilling were generally good, showing strong down-dip continuity in thickness and grade. Whilst this sector does not share quite the same high grades as seen in the main zone, the structure appears to be geometrically regular which benefits mining, and intersecting grades are in the 6g/t to 9g/t range over widths in excess of one metre. At Sao Chico, a total of 1,300m of down-dip drilling also gave satisfying results. In each case the main vein was intersected, confirming the strong structural continuity with a good range of grades being reported.

The quarter saw surface exploration re-start at Sao Chico. As reported last quarter, they acquired the exploration license to the west and south of the mine last year and they are very keen to test the potential continuation of the main vein into these areas. During the quarter they started a surface IP programme to the west and south, and although poor weather caused the work to be suspended it is expected that it will restart during Q2 2017. The purpose of the programme is to use IP to trace the trend of the main vein which has sufficient sulphides to provide a clear conductivity which in turn will be targeted by a subsequent drill programme.

Following the 39,390 ounces of gold produced in 2016 the board is forecasting 40,000 ounces in 2017 at an AISC of between $950 and $975 per ounce which is in line with the cost guidance of 2016.

Overall then this quarter has seen some pretty decent results. Profits were up, net assets increased and the operating cash flow improved with some free cash being generated. Both sales price and costs increased but the current price of $1,192 does not compare favourably with the $1,333 achieved in the quarter and is much closer to that of last year, although costs are not higher than in 2015 due to the Real appreciation.

The grade achieved at Palito has deteriorated due to ore being cemented in two stopes which meant that development ore at lower grades was used. Sao Chico saw the grade increase again, however, although how long this high grade seam will last I am not sure. The grades at Senna seem to be a little disappointing too, but with a forward PE of 9.1 the shares offer decent value. I am really torn here, I am minded to try and wait for the gold price to increase as I am worried about the increasing costs squeezing earnings.