Havelock have now released their interim results for the half year end 2013

Revenues for the group reduced across all business areas. The loss of discontinued revenue with the sale of the businesses was counteracted by a very similar reduction in cost of sales. Educational supplies revenue was broadly flat but the £3.3M fall in interiors revenue was very disappointing and was blamed on orders being more weighted to the second half of the year than usual – we will see if that is true at the end of the year. Admin expenses were well down, falling by nearly £2M which left operating profit £1.4M lower than in the first half of last year at £1.8M. A small finance cost was mitigated by a similar tax rebate and the loss for the year was £1.7M, which was £1.1M worse than in last year, not including £8M gained on the disposal of the subsidiary last year.

Total assets at the half year point were £8.3M lower than at the end of last year. The largest falls were the £9.2M reduction in trade receivables and the £1.7M fall in cash levels, this was only partially mitigated by a £2.3M increase in inventories as the group gears up for a more active second half of the year, which is where earnings are traditionally weighted. The £970K of assets held for sale relates to a property in Letchworth that is clearly deemed surplus to requirements. Liabilities were also lower, however, also down by £8.3M driven by a £6.6M reduction in trade payables and a £2.3M reduction in pension obligations as the value of assets in the pension scheme increased. These liability falls were slightly counteracted by a £746K increase in loans. The result of all this was that net tangible assets remained broadly flat from the end of last year at £10.1M.

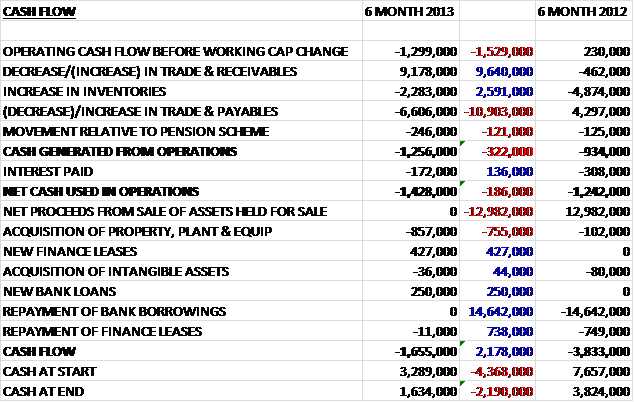

Things start off badly with the cash flow as the cash loss from the income statement was £1.3M, £1.5M worse than the first half of last year. The changes in working capital broadly cancel each other out with a decrease in receivables counteracted by decreases in payables and increased inventories. The increase in inventories was less than last year, however, and cash from operations was £322K worse than last year at a negative £1.3M. The interest paid on the loans was lower than last year and the net cash used in operations was only £186K worse at £1.4M. During the half year Havelock spent £857K on capital expenditure, which was mainly for the new laser cutting machine for the factory which it is hoped will improve efficiency going forward. This expenditure was partly paid for by a £427K new finance lease and a £250K increase in bank loans. At the end of the half year there was a £1.7M outflow of cash compared to a £3.8M outflow at this point last year. This is because last year the group paid off most of their debt. The cash levels now stand at £1.6M so the group can ill afford another half like this one.

Last year the group sold two businesses – the Showcard Print business, which was the point of sale division and Clean Air Ltd. The group received a cash inflow of £13M for the Showcard Print business and after taking into account the assets also disposed of in the sale, there was a gain of £8M. The Clean Air sale was much smaller and the group received a cash consideration of £563K with a gain of £50K. The discontinued operations actually turned a profit of £697K (mainly related to the Showcard Print business, profit from Clean Air was negligible) in the first half of last year and it seems the group has not yet been able to plug this gap.

The operating loss in the Interiors business increased to £1.1M, which is explained by their customers’ orders being more weighted than normal to the second half of the year. During the period there were some decent contract wins including a new framework with the Post Office to support its network refurbishment programme and the rebranding of Lloyds and TSB bank branches that starts in the second half of the year. The group have also undertaken a number of projects in Europe and the Far East and have recently been appointed lead partner for Marks and Spencer’s Far East activities. In addition, the group have also entered the supermarket sector with their first orders from a leading UK supermarket. The Education sector saw fewer programmes finalised in the period but recent announcements of further school building programmes suggest that activity may pick up again in the future. Havelock has increased their resources directed to student accommodation in order to secure larger projects in that area and they have also developed a new range of specialist healthcare furniture to win more business in that arena.

In educational supplies, margins remained steady and the segment reported a small loss (£100K) from a break-even point last year due to a change in the mix towards larger sound and light projects at Stage Systems.

Net debt at the end of the first half of 2013 was £4.8M, this was double the net debt position at the end of last year and is blamed on the build-up of inventories for the busier second half of the year and the capital investment of new equipment (shame the group is not in a position to use cash from operations for capital investment). Once again the board have not announced a dividend and the overall climate remains competitive. Going forward, the group is trying to improve margins through greater efficiency and value engineered products that cost less to produce. This half year was clearly difficult and the group have not been able to replace the lost contribution from the disposed businesses. Having said that, there are a number of interesting contract wins and the Lloyds/TSB and Supermarket contracts look particularly interesting, although it is not clear what the margins are like on these projects. It is difficult to make a good case for investment here but I am going to wait for the second half of the year to see if the board are correct and that it will make up for the slow first half. If not, I suspect I will be looking for an exit point.

On 8th November, the group announced that it had sold the leasehold property that was previously occupied by Showcard Ltd, which was sold by the group last year. They will receive £1.1M in cash that will be used to reduce debt but they will lose £150K of income a year that was the rent they charged Showcard. A shame to lose the income but I guess this is a sensible option to take.

I wouldn’t normally comment on the appointment of a new non-executive director but I feel that the announcement on 18th November that Andrew Burgess was appointed is noteworthy. Burgess has worked at Paragon Labels, MacFarlane Packaging and was Finance Director at Paragon Print & Packaging. Over the past few years Burgess has been buying up shares in Havelock and is now their largest shareholder. What his plans are long term are unknown.

On 29th January, the group issued a trading update covering the year to December 2013. It was stated that trading during the period was in line with expectations. The group had managed to widen its customer base and completed a project with a supermarket for the first time. It was also encouraging to see that there had been an increase in tender activity in both the UK and overseas. Despite this fairly good news, activity in the education sector was subdued and revenues here are expected to be lower next year but the group had made some progress in securing orders in student accommodation, which should filter through by 2015. After the sale of the property mentioned previously, there is now a situation where net debt is below £500K and within that there was £1M of capital expenditure. Overall, this is a fairly decent update.