Utilitywise has now released their interim results for the year ending 2017.

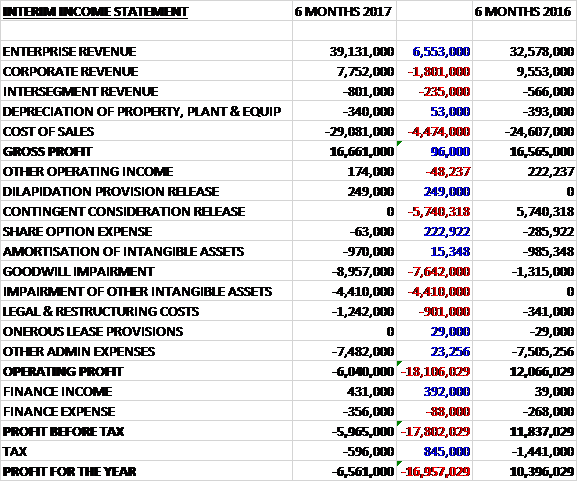

Revenues increased when compared to the first half of last year as a £1.8M decline in corporate revenue was more than offset by a £6.6M growth in enterprise revenue. Cost of sales also increased to give a gross profit that was broadly flat, up just £96K. We then see a £249K dilapidation provision release and a £223K decline in share option expenses but there was no contingent consideration release which brought in £5.7M last time, there was a £7.6M increase in the goodwill impairment and a £4.4M impairment of other intangible assets. There was also a £901K increase in restructuring and legal costs but other admin expenses remained flat. The finance income increased by £392K and the tax charges fell by £846K which meant that the loss for the period was £6.6M, a detrimental movement of £17M year on year.

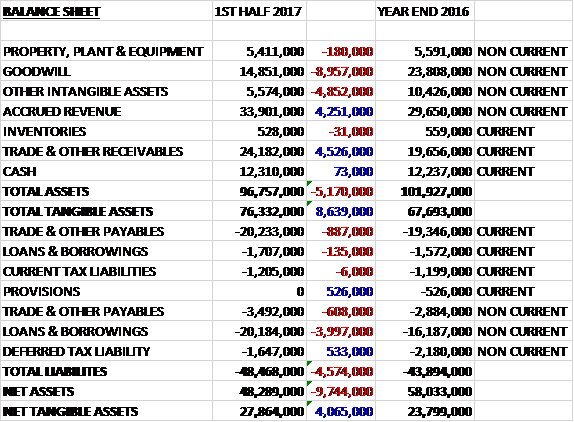

When compared to the end point of last year, total assets declined by £5.2M driven by a £9M decrease in goodwill and a £4.9M decline in other intangible assets, partially offset by a £4.5M growth in current receivables and a £4.3M growth in accrued revenue. Total liabilities increased during the period as a £526K fall in provisions was more than offset by a £4.1M growth in borrowings and a £1.5M increase in payables. The end result was a net tangible asset level of £27.9M, a growth of £4.1M over the past six months.

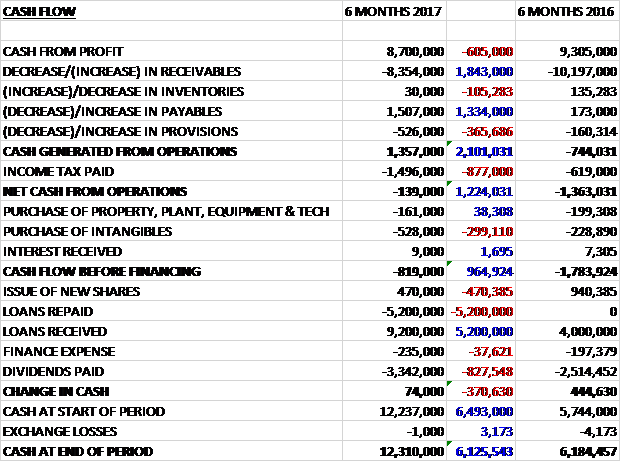

Before movements in working capital, cash profits declined by £605K to £8.7M. As usual there was a large outflow of cash due to an increase in receivables but this was less than last year and after the tax payments increased by £877K there was a net cash outflow from operations of £139K, an improvement of £1.2M year on year. The group spent £161K on tangible assets and £528K on intangibles to give a cash outflow of £819K before financing. The group paid out £3.3M in dividends and paid for it by taking out a net £4M of new loans to give a cash flow of £74K and a cash level of £12.3M at the period-end.

The adjusted profit in the Enterprise division was £7.8M, a growth of £1.9M year on year. The total number of customers increased in the UK and Ireland by 13% and in Europe by 32% equating to an overall increase of 16%. The UK business also delivered a growth in EBITDA of 13% with the European business also contributing with a maiden £400K EBITDA. Enterprise revenue added to order book increased by 24% to £50.2M from an increase in energy consultant headcount of only 6%. Significant progress has been made with staff attrition issues and turnover fell from 39% last time to 25% in the period.

Previously the group negotiated terms with certain suppliers to accelerate cash payment terms in respect of same supplier renewals. Whilst this renegotiation has accelerated a proportion of those terms, on average same supplier renewals typically have longer dated billing profiles than acquisition contracts. Same supplier renewals made up 23% of the division total revenue which has contributed to the increase in the accrued revenue.

The adjusted loss in the Corporate division was £79K, a detrimental movement of £1.4M when compared to the first half of last year with revenues falling by 19%. This was primarily due to the Energy Services element of the business which saw a fall in revenues of 30% due to delays in the rollout of technology across certain customer retail sites as well as the prior year having the benefit of £600K of revenue from the ESOS which did not recur. The corporate procurement element of the business saw revenue fall by 2%. The fall in EBITDA was also impacted by investments to position the business for growth which started in the second half of the prior year.

Entering the second half of the year, the group now offers an intelligent platform that can provide customers with a single gateway and control over every operational system within their building. Two major high street retailers, for example, have been able to reduce their energy consumption by 15% and 23% respectively as a result of the solution provided by the group with a payback period of less than a year. Going forward the group’s investment in technology will provide it with a growing channel through which to engage with new customers and cross sell their services.

Exceptional charges in the period comprise an impairment charge in connection to the cost of t-mac and charges in relation to various legal, restructuring and other costs. Exceptional income in the period relates to an adjustment to a historic dilapidations provision. As a result of a significant shortfall in financial performance against previous expectations, an impairment was identified in t-mac. The pre-tax value of the impairment loss was £13.4M which was first allocated against goodwill and then the rest of the assets.

In order to strengthen the group’s commercial prospects the board has taken the decision to discontinue the practice of taking cash advances from suppliers which will have an impact on net debt and make the earnings look even more dubious. Last year these cash advances totalled £10.4M but the group apparently has to maintain commercial independence from its suppliers which is apparently what is behind this decision – I am not sure how this practice affected independence.

This means that the group will not seek previously planned cash advances totalling £9.2M during the second half and will actually repay a further £4.5M as the assumed volume of contracts delivered by the group for certain suppliers will not be met. This will obviously affect cash flow in the second half of the year. I fear we are not being told the whole story here and this is very disappointing.

There have been a lot of board changes recently. In October 2016 Brendan Flattery joined the board as CEO, replacing Geoff Thompson who took up the position of executive chairman. Richard Feigen stepped down as non-executive chairman on that date, remaining on the board as a non-executive director. In November, Simon Waugh jointed the board as a non-executive director. In January 2017, Richard Laker replaced Jon Kempster as CFO, in February Kathie Child-Villiers joined the board as a non-executive director and in April, Geoff Thompson took up the position of non-executive Chairman.

For what its worth at the current share price the shares are trading on a PE ratio of 8 which falls to 6.9 on the full year consensus forecast. At the period-end the group had a net debt position of £9.6M compared to £5.5M at the year-end. After a 5% increase in the interim dividend (that they can’t really afford) the shares are yielding 5.1% which increases to 5.3% on the full year forecast.

Overall then this has been a bit of a disappointing period for the group. If we ignore the impairments and various provision releases, the profit fell modestly but net tangible assets increased. The operating cash outflow improved but this was due to working capital movements and the cash profits declined. Needless to say, no free cash was generated. The Enterprise division seems to be ticking along OK with more customers and the European business now contributing but the corporate business fared less well with delays in the rollout of technology to a customer and now ESOS revenue.

The T-mac acquisition looks to have been a disaster and seems to have been considerably impaired but the real disappointment for me is the reversal of the decision to take some cash payments upfront from suppliers. Indeed, the group are actually paying some back. It seems to me that they have failed to meet targets with one supplier in particular. This is a real blow as it means the group is going to continue to fail to generate any cash. It therefore seems strange that they persist in paying a dividend which now stands at 5.3%. The forward PE looks cheap too, at 6.9 but these profits don’t seem real to me and I am not touching this until they can prove that they can generate cash.

On the 29th June the group announced that it had been made aware of a material level of under consumption in certain contracts placed with one of the major energy companies dealt with by the group. They have agreed to make repayments of commissions, previously paid to the group, totalling £7.6M before December 2020. As a result of changes in internal controls the board is confident that contracts placed after August 2016 will show more normal levels of consumption over the lives of the contracts.

The board feels it is prudent to reflect the full impact of the payments in the financial statements of the group at this stage but they believe they will receive some of the cash back from the energy company at the conclusion of the contracts. They will recognise an accounting charge for £11.2M in their income statement this year, of which £7.7M is an exceptional item and £3.5M will reduce the underlying profits.

This, sadly, seems to be another consequence of the opaque nature of profits at this company and the £3.5M hit to underlying profits in particular is a big concern. I have no desire to buy in here.

On the 31st July the group released a trading update covering the year. Based on trading in July to date and under the existing revenue recognition policy, the group now expects that its revenue for the year will be around £4M below previous management expectations. The shortfall mostly comprises revenue from same supplier renewals contracts which form a substantial proportion of the revenue secured by the group in the final months of the year. Substantially all of the shortfall in revenue will impact on profits.

They are also adopting a new accounting standard regarding revenue from contracts with customers, as a result of which they will change their accounting policy in respect of timing of recognition of revenue related to renewals contracts. Had they adopted this standard last year, the fall in signed renewals contracts against expectations would not have materially impacted group revenue or profits this year.

They currently recognise revenue on the signature by a customer of a renewal contract with their existing supplier. Furthermore, they currently recognise revenue upon the start of a new customer contract. Under the new standards, revenue in respect of renewal contracts will be recognised at the start of the contract rather upon signature.

Whilst the profit warning is clearly disappointing, the new revenue recognition standards are a step in the right direction, although more could still be done in my view.

On the 24th August the group released a trading update covering the year as a whole where they performed in line with the revised expectations. They expect to report group revenue 3% higher but pre-tax profits 40% lower than last year, primarily due to an adjustment recognised in respect of projected under-consumption of contracts and the deferral of certain significant renewals contracts.

The enterprise division delivered a strong underlying operating performance despite the issues. Additions to the gross order book totalled £99.2M, an increase of 17% as a result of a number of planned productivity improvement initiatives which included enhanced operational management and a reduction in sales force headcount. The order book also increased by 17% on a like for like basis. The European operation performed well with an increase in revenue and operating profit compared to the prior year.

The corporate division saw a decline in revenue but the profit of the division in H2 was broadly in line with H1 as the business continued to build a pipeline of future work.

The board expects net debt to be around £19M compared to £5.5M at the end of last year. The main reason for the increase during the year was the decision to discontinue the acceptance of advance cash receipts from certain energy suppliers in respect of new business not yet written. The year-end net debt is lower than expectations due to £1M of legacy supplier cash advances that remained outstanding which is now expected to be repaid during 2018.

On the 17th January the group released an update. After a review their results will reflect a change to the accounting policy of the group regarding the estimation and recognition of revenue on contracts. The proposed change will reduce the initial revenue recognition value of new contracts which would then positively impact the final revenue adjustment value at the end of the contracts. It will have no impact on the cash flows of the group. Work is ongoing with the auditors to finalise the value of amendments in respect of 2017 and earlier years.

The cumulative impact of the non-cash accounting adjustments is expected to have a material negative impact on group equity but it is not yet known whether there will be a material impact on the profit for the group in 2017. There is likely to have a material impact on reported revenue and profit in 2018, however.

The group’s lender is aware of all related developments and discussions are ongoing with the bank. It may become necessary to obtain waivers of breaches and amendments to the group’s banking covenants.

To be honest this should hardly come as a surprise as the group has been over-aggressive with its revenue recognition policies for years. In fact it should actually improve the reporting of the group. I am not rushing to buy quite yet, until we can see the actual impact and what the bank decides to do.