Cambria Automobiles has now released their interim results for the year ending 2017.

Revenues increased when compared to the first half of last year due to a £15.1M growth in used vehicle revenue, a £12.6M increase in new car revenue and a £3.3M growth in aftersales revenue. Cost of sales also increased to give a gross profit £2.9M above that of last time. We also see no profits on the disposal of branches, which brought in £1.1M last time and other admin expenses increased by £2M to give an operating profit £386K lower year on year. After finance expenses fell by £155K the profit for the six month period came in at £4.3M, a decline of £224K year on year.

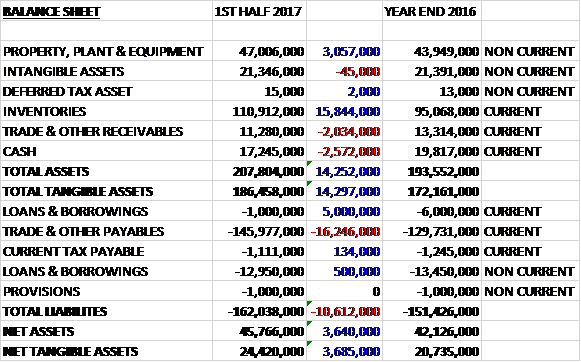

When compared to the end point of last year, total assets increased by £14.3M driven by a £15.8M growth in inventories and a £3.1M increase in property, plant and equipment, partially offset by a £2.6M decrease in cash and a £2M decline in receivables. Total liabilities also grew during the period as £5.5M decrease in borrowings was more than offset by a £16.2M growth in payables. The end result was a net tangible asset level of £24.4M, an increase of £3.7M over the past six months.

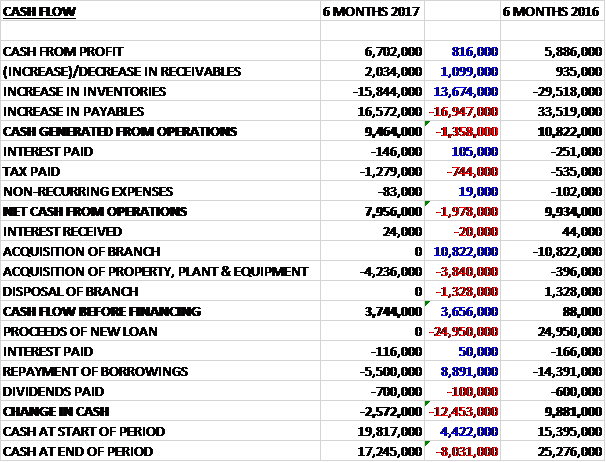

Before movements in working capital, cash profits increased by £816K to £6.7M. There was a cash inflow from working capital but this was less than last time and after tax payments increased by £744K, the net cash from operations was £8M, a decline of £2M year on year. The group spent £4.2M on property, plant and equipment to give a free cash flow of £3.7M. This was used to pay the £700K of dividends and repay £5.5M of borrowings to give a cash outflow of £2.6M for the half year and a cash level of £17.2M at the period-end.

The gross profit in the new vehicles business was £11.2M, a growth of £2.4M year on year. New vehicle revenue increased by 9.6% but total new vehicle sales volumes were down 4.6%. The average profit per unit sold soared by 34% reflecting a combination of like for like increase and the strengthening mix from the JLR and Aston Martin business acquired which sell at higher price points.

On a like for like basis, new volumes reduced by 12% with profit increasing by £700K as profit per unit increased by 24%. The like for like volume reduction was partly attributed to the reduction in unit sales from the Barnet JLR site during the disruptive building project, and partly attributable to reductions in unit sales from certain volume manufacturer partners. The achievement of annual new car volume related bonuses for the year has had a positive impact on the profit per unit.

The group’s sales of new vehicles to private individuals was 4.7% lower at 4,604 units as anticipated. New commercial sales reduced by 28% to 342 units and new fleet sales increased by 32% to 433 units. The new vehicle registration data showed continued growth in registrations which were up 5% in the period.

The gross profit in the used vehicles business was £11.6M, an increase of £300K when compared to the first half of last year. Revenues increased by 12% whilst the number of units sold decreased by 1% primarily as a result of the closure of Swindon Motor Park which was a high volume used car operation. The profit per unit sold increased by 3.5%. On a like for like basis, used car volumes increased by 1.3% and profit per unit increased by 2.3%.

The group have continued their focused strategy in the used car department to increase the efficiency which they source, prepare and market their used vehicles in order to drive the velocity trading principles. This has produced good results, increasing the number of units sold and the profitability of the used car department.

The gross profit in the aftersales business was £13.3M, a growth of £200K when compared to the first half of 2016. Revenues increased by 10% with like for like revenues up 2% but profits down £300K. The fire that took place in October at the Jaguar and Aston Martin aftersales workshop in Welwyn Garden City has had a significant impact on the profitability of that site, and whilst they have attempted to maintain a service level of their customers by utilising the Land Rover dealership, the constraint on both operations has been evident. The business interruption insurance claim has not been included in the figures and will not be recognised until they have finalised the claim. The site redevelopment is now ongoing and they will be back in occupation of the workshop by mid-June.

During the period there has been £4.2M of capex incurred and a number of other development projects initiated. The major redevelopment of the Barnet JLR site began in February and will complete by the end of May. There has been a number of other site refurbs progressing in the period. The Swindon JLR development will start in May with the aim of being in occupation before March 2018.

The development of the Barnet property began in February 2016. As a result of some small delays in the programme, the group took the decision not to take occupancy of the showroom in the plate change month of March, with occupation of the facility in April. There are still some ongoing external works to the site which will be completed in May. There has been a significant amount of disruption to the operation of the business during the building project as they have maintained the sales business on the development plot with the contractors working around them. Whilst the building work has significantly impacted the profitability of the site, it has remained profitable. The total build cost for the site is £7M, £700K of which is still to be paid on completion.

The planning process for the delivery of the new Swindon development has been ongoing for some time whilst they have been working with the Highways and Environment Agency to ensure that the development of the site integrates with other major developments that are taking place around the area. The planning process has taken much longer than anticipated, however, but they are now nearing the end and intend to have contractors on site by the end of May. It is their intention to be operating in the completed facility by February 2018 and the anticipated cost of the work is £6M.

The group are in the process of acquiring land in the Welwyn Garden City territory for the development of the new JLR and Aston Martin facilities, and in Solihull for the new Aston Martin business. The total purchase and development cost expected for the Welwyn Garden City site is £16M and the Solihull site is £4.5M. The group are aiming to complete these developments befre the end of 2018.

During the period the group concluded the closure of its Swindon Motor Park operation. Whilst there was no formal sale of the business, the associated that were employed directly in the SEAT business that occupied the site were transferred to another local dealer under TUPE. The closure of this business makes the land previously occupied by it available for the development of the new JLR facility.

The board anticipated that with the weakening of sterling there would be some downward pressure on the new car market this year but the March registration data showed the largest number of registrations since 1999. They were assisted by some pull forward of demand as a result of the changes to Vehicle Excise Duty from April and the April registrations were significantly down year on year.

They are still cautious on the consumer outlook this year and do not believe that the growth in new car registrations in the first half accurately reflect the level of retail consumer demand in the market. While the board remains cautious, the group’s performance in March and April was in line with the previous year and they are confident that full year results will be slightly ahead of current market expectations.

At the current share price the shares are trading on a PE ratio of 9.6 which falls to 8.2 on the full year consensus forecast. After a 25% increase in the interim dividend the shares are yielding 1.3% which increases to 1.4% on the full year consensus forecast. At the period-end the group had a net cash position of £3.3M compared to £300K at the same point of last year.

Overall then this has been a relatively decent period for the group. Whilst profits were down this was due to no profits from branch sales in the period and underlying profit increased. Likewise, whilst the operating cash flow deteriorated, this was due to changes in working capital and cash profits rose with some free cash being generated. The new vehicle business seems to be performing well as a better mix and some like for like price rises mean the increased profit per vehicle more than offset the reduced volumes, not helped by the disruption surrounding the building work.

The used vehicle business seems to be performing fairly well and although the aftersales business only saw modest increases, this was not helped by the fire. Going forward there will be a lot of capex being spent on the JLR sites and the building work is likely to lead to more disruption. Also, I don’t believe the full brunt of Brexit is being felt in this market yet. Despite these misgivings, the forward PE of 8.2 suggests a share that is pricing quite a lot of this in and it might be worth a punt?

On the 5th September the group released a trading update for the first eleven months of the year which was in line with expectations and ahead of the prior year. The board remain cautious on the consumer outlook and the trading environment in the period after March has been more challenging, particularly in the new car arena. The weakening in Sterling has led to inflation in the landed cost of imported vehicles which, combined with a level of consumer uncertainty in the market, has led to the reduction in new car sales. The performance in the period between April and July has been weaker than the prior year as a result of these market conditions.

Used vehicle sales continued to perform well and whilst unit sales were 5.5% down following the closure of Swindon Motor Park, the reduction in units has been more than offset by improved profit retention with gross profit per unit on both a total and like for like basis continuing to increase. This performance has grown the profit from the used car segment of the business.

The aftersales operations increased revenues by 1.7% on a like for like basis but like for like profitability decreased by 1.3%. This performance was impacted by a fire at the Welwyn Garden City JLR workshop in October. The work to rebuild the workshop was completed in June and they have since resumed normal operation. The business interruption insurance claim has been submitted and will be included in the full year results which will bring aftersales like for like profit in line with the prior year.

Whilst new vehicle unit sales for the period were down 17.6% on a like for like basis, the gross profit per unit in this department improved and the gross profit in the department improved. The reduction in volume was partly attributed to the reduction in unit sales from the Barnet JLR site during the disruption caused by the new building project, and partly attributable to reductions in unit sales from certain volume manufacturers. The achievement of annual new car volume related bonuses for the 2016 calendar year and Q1 2017 has had a positive impact on the profit per unit and therefore offset any reduction in the overall gross profit (although this is unlikely to continue going forward).

Heading into the important September trading period, the new car order book is building in line with their expectations in the current market conditions. Overall things don’t seem too bad here but tougher times seem probable over the next year.