Serabi Gold has now released their Q1 results for the year ending 2017.

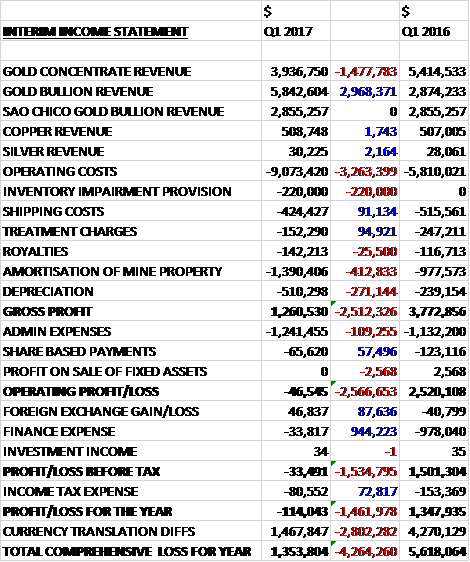

Revenues increased when compared to Q1 last year as a $1.5M decline in gold concentrate revenue was more than offset by a $3M growth in gold bullion revenue. Operating costs increased by $3.3M, there was an inventory impairment of $220K against the coarse ore stockpiles, amortisation was up $413K, reflecting the lower levels of inventory as the coarse ore stockpiles are depleted, and depreciation increased by $271K reflecting new equipment purchased and the strengthening Real, to give a gross profit $2.5M below that of last time. Admin expenses increased by $109K which meant there was a small operating loss, an adverse movement of $2.6M. Finance expenses declined by $944K, however, and after tax expenses fell by $73M the loss for the quarter came in at $114K, an adverse movement of $1.5M year on year.

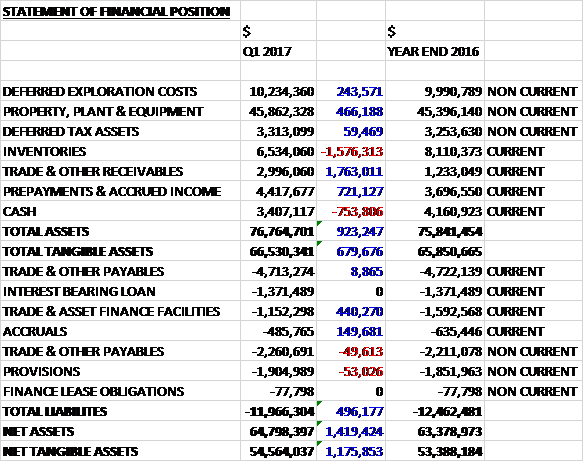

When compared to the end point of last year, total assets increased by $923K driven by a $1.8M growth in receivables, a $721K increase in prepayments and accrued income, a $466K growth in property, plant and equipment (aided by forex movements) and a $244K increase in deferred exploration costs, partially offset by a $1.6M fall in inventories due to a reduction in ore stockpiles. Total liabilities declined during the period due to a $440K fall in the trade and asset finance facilities along with a $150K decrease in accruals. The end result was a net tangible asset level of $54.6M, a growth of $1.2M over the past three months.

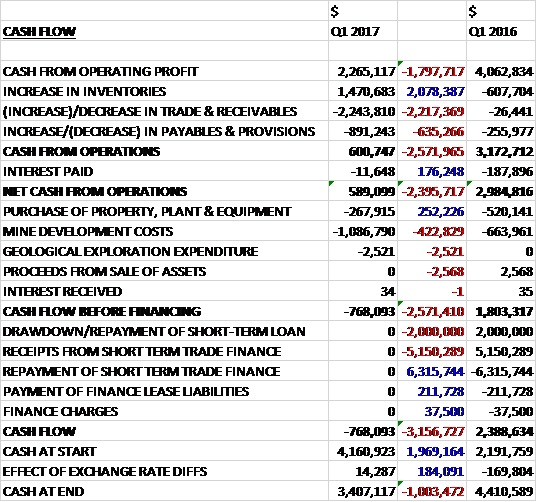

Before movements in working capital, cash profits declined by $1.8M to $2.3M. There was also a cash outflow from working capital and after interest payments reduced by $176K, the net cash from operations was $589K, a decline of $2.4M year on year. The group spent $1.1m on mine development costs and $268K on property, plant and equipment which meant that there was a cash outflow of $768K before financing. There was actually no financing arrangement changes during the quarter so this was also the total cash outflow for the period to give a cash level of $3.4M at the period-end.

The average gold price received reduced from $1,245 per ounce to $1,204. Conversely the AISC increased from $965 per ounce to $1,043.

In the quarter the group mined 36,918 tonnes of ore at a grade of 10.12g/t compared to 37,546 tonnes at 11.02 g/t in Q1 last year, although the grade was higher than Q2-Q4 2016. They milled 46,663 tonnes at a grade of 7.09g/t compared to 36,615 tonnes at 8.58g/t last time, with the increase reflecting the increased plant capacity, which produced 9,861 ounces of gold, a slight increase on the 9,771 produced in Q1 2016.

The main issue during the period has been a large increase in operating costs, over and above the growth in revenue. These costs have been severely impacted by the 19% strengthening of the Brazilian Real against the dollar. In addition, labour costs were affected by the 10% increase in salaries awarded in May as part of the national collective wage agreement and one-off termination costs of $417K following a reduction in headcount. There was also an increase in power costs following a decision taken that the group should use its own more expensive diesel generated power than rely on cheaper but less reliable grid derived power.

With the change in customer for the group’s concentrate during 2016, they no longer have need for the trade finance facility which was in place in Q1 2016. The convertible loan was settled in August and the group have not undertaken any hedging activity during the period.

Development of the Palito ore body is now well in advance of production requirements and as a result the group has been able to reduce development mining activity for a short period. As a result mine development of 1,669m during the quarter was about 13% lower than in Q1 last year allowing the company to use the surface ore stockpiles.

At Sao Chico, during the remainder of the year, management expects that monthly development and production rates will continue to stablise. They have been driving development galleries east and west towards additional ore shoots that have been identified by surface drilling. Management is confident that these shoots will provide additional mineable ore at Sao Chico. Underground drilling is being undertaken at Sao Chico for short term operational and mine planning purposes with a second parallel campaign being undertaken to test the deeper resource potential of the deposit.

As with the Palito ore body, development is significantly in advance of production so the group has been able to reduce the levels of development mining activity during the period with the result that 582m of horizontal development was completed compared with 1,025 for the corresponding quarter in 2016.

Milling rates of ore have increased by 15% from an average of 403 tonnes per day to 463tpd in Q1 2017. The introduction of the third ball mill at the end of June has had a significant effect on throughput rates. The increase in processing rates also reflects the improvements in operational efficiency of the process plant which has been assisted by the introduction of the gravity circuit and ILR for treating Sao Chico ore, reducing the levels of gold which would otherwise have been treated in the CIP circuit. The average daily process rates for the CIP circuit have increased by 14% to 518tpd.

The forecast gold production for 2017 is expected to be about 40,000 ounces and the cost guidance for the year is of an AISC of $950 to $975 per ounce. The cost profile is subject to change as a result of exchange rate variations and in particular the exchange rate between the Brazilian Real and the US dollar.

At the current share price the shares are trading on a PE ratio of 9.5 which apparently falls to 4.4 on the full year consensus forecast.

Overall then this has been a bit of a tricky period for the group. Operationally things have been fine with the increased capacity of the mill meaning that ore stockpiles are being run down. The group swung to a loss, however and the operating cash flow deteriorated with no free cash being generated. The reason for this is clear. Whilst the price achieved for gold sales was $1,204, down slightly, the costs have increased to $1,043 per ounce. The main reasons for this seem to be the strengthening of the Brazilian Real, the increased staff costs and the increased power costs as the group can no longer rely on grid power.

The forward PE of 4.4 looks very cheap but I have doubts as to whether this can be achieved. At $1,252 per ounce the gold price has improved slightly since the period-end and the Brazilian real has come off the boil somewhat in rec

On the 26th July the group released a trading update covering Q2. Overall production was 8,148 ounces of gold. Mine production totalled 42,075 tonnes at 7.8g/t of gold and 43,905 tonnes was processed through the plant for the combined mining operations with an average grade of 6.26g/t. Following a strong Q1 when the group produced nearly 10,000 ounces of gold, they had a satisfactory Q2 with further production of 8,148 ounces.

Mine production progressed well but grades were a little lower than scheduled for April and May, resulting in Q2 gold production being lower than Q1. The lower grades behind this were largely a result of an operational issue in the Sao Chico sector relating to a broken-down loader where planned higher grade stope production had to be replaced by lower grade development ore. Production improved significantly in June and the operational issue has now been fully resolved. The board therefore remain confident that full year production guidance will be achieved. At Palito, production remained steady.

At Palito the G3 vein has now been intersected on the -50mRL, the lowest level in the mine, with excellent grades being encountered. The other main vein is now being developed on the 30mRL, and it too is showing some good long term potential.

Overall then this has been a rather disappointing quarter but the situation seems to have improved in recent months so I am holding on for now.