N Brown has now released their final results for the year ended 2017.

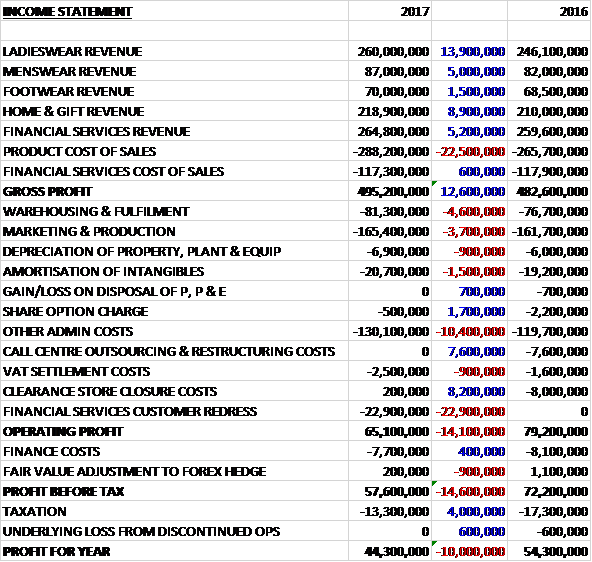

Revenues increased when compared to last year due to a £13.9M growth in ladieswear revenue, an £8.9M increase in home & gift revenue, a £5.2M growth in financial services revenue and a £5M increase in menswear revenue. Cost of sales also increased to give a gross profit £12.6M above last time. Warehousing and fulfilment costs increased by £4.6M, marketing and production costs were up £3.7M, depreciation and amortisation increased by £2.4M and other admin expenses were up £10.4M. There were no call centre restructuring costs, however, which accounted for £7.6M and no clearance store closure costs which were £8.2M last time. There was a £22.9M financial services customer redress, however, which cost £22.9M in the period to give an operating profit £14.1M below last year. Excluding those issues, operating profit was down £7M. Finance income was down £900K but tax charges reduced by £4M to give a profit for the year of £44.3M, a decline of £10M year on year.

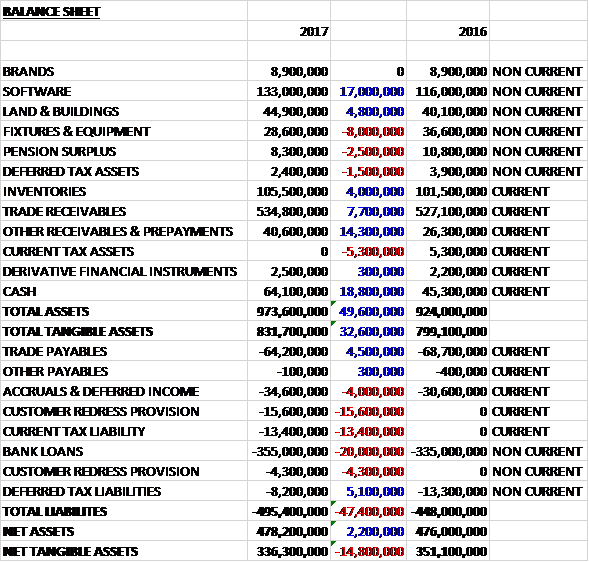

When compared to the end point of last year, total assets increased by £49.6M to £973.6M driven by an £18.8M increase in cash, a £17M rise in the value of software, a £14.3M growth in other receivables and a £7.7M increase in trade receivables, partially offset by an £8M reduction in the value of fixtures and equipment as £5.9M was reclassified at land and buildings. Total liabilities also increased during the year due to a £20M growth in bank loans, a £19.9M increase in the customer redress provision and a £13.4M growth in the current tax liability. The end result is a net tangible asset level of £336.3M, a decline of £14.8M year on year.

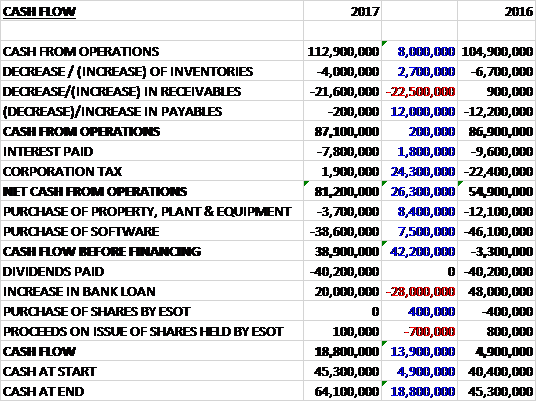

Before movements in working capital, cash profits increased by £8M to £112.9M. There was a cash inflow from working capital but this was less than last year so before tax and interest the cash from operations was broadly flat at £87.1M. Interest payments came down by £1.8M and there was a £24.3M swing to tax receipts so the net cash from operations came in at £81.2M, a growth of £26.3M year on year. They then spent £38.6M on software along with £3.7M on tangible assets to give a free cash flow of £38.9M. This didn’t quite cover the dividends of £40.2M but £20M of new loans meant that there was a cash flow of £18.8M for the year and a cash level of £64.1M at the year-end.

Ladieswear revenues were up 4.2% over the year but this masks a very good second half to the year with H2 revenues up 10.4% with significant market share gains. This has been driven by significant investments in improving the product ranges, strengthening internal design and increasing in-season flexibility. The menswear market share was flat.

The returns rate was down 70bp to 26.8% with the primary driver being the continued improvements in the product offering, including fit, quality and value for money. The ongoing increase in the proportion of cash customers also benefited the rate.

JD Williams revenue was up 4.7% with the JD Williams brand itself up 12% and Fifty Plus down 9%. They had particular success with their “The Cut” range, a collection of their best priced current season clothes which further reinforced their value for money credentials. Sales of these lines significantly exceeded expectations, up 72%. For Spring Summer they launched a new bridal range for JD Williams. The performance of Fifty Plus improved as they progressed through the year. In the first half, revenues were down 18% as they reduced marketing spend ahead of its migration into JD Williams. They then started the migration in Autumn which resulted in revenues up 1% in H2 with the migration due for completion by the start of the second half of 2018.

Simply Be had a strong performance with product revenue up nearly 10% with the number of active customers up 20%. The fast fashion sub-range continues to outperform significantly with demand up 67% in the second half, led by going out tops and the new under £30 party dress offer. Denim was a key category outperformer throughout the year with jeans up 14% in the second half.

Jacamo product revenue was up 4% at £65.3M with revenue performance strengthening throughout the year. Active customers grew double-digit year on year, although spend per customer was lower due to the subdued market backdrop, particularly in the first half. In late February they launched an unlimited next day delivery for £10 and customer take up has so far been encouraging. Strong AW16 product category performances were seen in denim, following the launch of their new range, and sportswear, driven by third-party brands and the relaunch of their own-brand Snowdonia.

Secondary brand revenue increased by 1.6%. Fashion World was the strongest performer, up mid-single digit year on year driven by increased spend per customer. Marisota, which is now predominantly used as a product brand focusing on fit solutions, saw a solid performance. Figleaves revenue was down slightly as they slowed marketing spend through the launch period of the new Demandware web platform which went live at the start of Autumn 2016. In February they hired a new CEO for the brand and the new management team will leverage the benefits of the Demandware platform and they expect this to improve the performance of the brand going forward. High and Mighty revenue was down as they continued to transition the brand from a predominantly stores to online model.

The traditional segment recorded revenue down 1.3% although this masked an improving trend as we progressed through the year with revenues down 4.2% in the first half but up 1.6% in the second half as actions taken to address performance worked well. These actions included a revamp of their marketing materials and the launch of new bespoke publications such as their Classic Detail catalogue. They also improved the product range. Looking forward the strategy remains unchanged – to hold overall revenues broadly flat through gaining share in this declining market.

At the start of 2017 the group added over 100 third-party brands across their categories such as Wrangler, Ben Sherman, Jack Wolfskin, Dune, Timberland, Ann Summers and Gossard. This also works the other way round and the group went live with a capsule Jacamo collection on ASOS in March with the very early performance being encouraging. Also, as part of a strategy to drive increased access to their brands, the group also announced a partnership with Tesco for Simply Be and Jacamo and capsule collections from both brands will be available through Tesco Direct and, on a trial basis, in store at a number of locations across Eastern Europe from May this year.

The international markets seem to be gaining traction with an operating profit of £1.9M compared to losses of £100K last year. US revenue was up 8.5% year on year but down 4.2% on constant currency terms. The operating loss increased by £300K to £1.3M as the performance in the second half was impacted by the launch of the new website, as expected. The majority of US customers are generated by the Simply Be brand but the performance of the JD Williams brand which launched in March 2016 has so far been encouraging. In Ireland, revenues were up 3.8% in constant currency terms and the increase in operating profit was driven by improvements in the product offering.

The performance of the store estate continues to be impacted by weak industry footfall. As a consequence they are not planning to open any new stores in the future. For the coming year some significant rate increases for some of the stores represent a further cost headwind. Overall the operating loss from the store estate increased by £1.2M to £2M.

The group had a good performance in Financial Services this year, driven by a significant improvement in the quality of the customer loan book. This resulted in revenue up 0.4%; within this interest payments were up mid single-digit whilst non-interest lines were down low double-digit. The improvement in the quality of the loan book is particularly reflected in the gross margin performance which was up 110bp to 55.7%.

Credit arrears were down 100bp driven by the improvement in the quality of the loan book and the credit provision rate was down even more, benefitting from several sales of high risk payment arrangement debt which the group sold for a slightly better rate than book value.

To date the group have introduced a new finance system, a new merchandise system, the Simply Be Euro foundation site and the new US website. The next release will be the High and Mighty website which remains on track for May. This release will also include the first go-live of the new financial services system so it is a significant milestone.

The group have made an adaptation to the rollout plan. Following the High and Mighty go-live, they have now decided that Fashion World will be migrated onto the new systems after peak trading in 2017. The pace of development will be unchanged, however, and new releases will be added to the High and Mighty and US websites on a monthly basis. They plan to migrate all brands onto the new platform by the end of Summer 2018 as previously guided and the overall programme costs and benefits and the timing of those benefits are all unchanged.

An exceptional charge of £22.9M was recognised reflecting the costs incurred or expected to be incurred in respect of payments for historic financial services customer redress payments. So far the group has paid out £3M in cash on this subject. There are two components of this cost, recompensing certain customers due to an error in the previous calculation for redress and the group’s estimate of the likely future costs arising from complaints relating to financial services products sold in the past. The cost of this second area increased during H2 due to a combination of the industry-wide deadline for complaints being a year later than previously indicated and a greater than expected volume of complaints due to wider public awareness of the deadline.

External costs related to tax are in respect of ongoing legal and professional fees which have been incurred as a result of the group’s ongoing disputes with HMRC regarding a number of historic tax positions. The board estimate that an unfavourable settlement of the tax cases could result in a charge to the income statement of up to £43.3M and a cash payment to HMRC of up to £16M. A favourable settlement of these cases would result in a repayment of tax of up to £54.1M and an associated credit to the income statement of up to £29M.

Going forward, performance in the new financial year has so far been encouraging and in line with board expectations. For 2018, the product gross margin is expected to fall by between 20 and 120bp with the key driver being increased input costs as a result of the depreciation of sterling. Financial services gross margin is expected to be flat to +100bp. Group operating costs are expected to increase by between 3.5% and 5.5% reflecting an element of IT double running costs. Net debt is expected to be between £300M and £320M reflecting the increased cash flow impacts of financial services customer redress payments coupled with further advance tax cash payments related to the ongoing disputes with HMRC.

At the current share price the shares trade on a PE ratio of 17.8 which falls to 12.7 on next year’s consensus forecast. After the final dividend was kept the same, the shares are yielding 5.1% which is also expected to remain the same next year. As of the year-end the group had a net debt position of £290.9M which represents a 0.4% increase year on year.

Overall this has been quite a tough year. Profits were down and net assets declined, although the operating cash flow did improve with some free cash being generated, although it did not cover the dividend payment. Most of the brands are doing well, with an improving situation throughout the year with the only real declines being at Figleaves and the US business which have both seen disruption due to the new systems being put in place. The stores are doing poorly, however, and are more loss making than last year. Financial services were broadly flat.

Trading seems to be doing Ok and improving then, but there are a number of one-off issues hanging over the group. The customer redress payments are growing and looking rather onerous, the debate with the HMRC rumbles on and seemingly could go either way and although it seems to have been handled well so far, the large scale IT systems upgrade is both costly and has the potential for disruption. With a forward PE of 12.7 and (uncovered) yield of 5.1% these shares look OK value but I am not sure they are cheap enough for the risk involved.

On the 20th June the group released a Q1 trading update. Group revenue was up 5.6% with product revenue increasing by 10.2% driven by strong ladieswear performance, and financial services revenue down nearly 5% as expected. In all, trading is on track to meet the board’s expectations for the year.

The strongest performance was from Simply Be, with revenues up more than 20% following the “We are Curves” campaign. Although Jacamo sales were only up 5.5%, this masks the fact that there was double digit growth in active customers which was offset by the reduction in sales of some larger ticket electrical goods. There was a 10.7% growth in the traditional segment reflecting the improvements made to product and marketing during the past two seasons, and JD Williams was up 12.7%. Even the poorest performer, Fifty Plus, still managed a 1.3% increase in sales.

International revenue was up 10% but down 2% in constant currency terms. Revenue from Ireland was up 9% at constant currency, driven by a strong ladieswear performance but revenue in the US was down 9% at constant currency. Following the delivery of the new technology platform, a step up in marketing investment is planned in Q2 to drive new customer recruitment going forward.

The group will be closing up to five Simply Be and Jacamo dual fascia stores. This decision takes into account weak high street footfall, together with significant future business rate increases for some stores. Together these stores accounted for the entire £2M operating loss of the store estate in 2017. The process will be completed by the end of August and the board expect an exceptional cost of between £10M and £14M, of which about 70% will be cash. During Q1, revenue from the store estate was slightly up year on year with the Simply Be/Jacamo stores recording mid-single digit growth and High and Mighty revenue down.

Revenue from the financial services business was down nearly 5%, in line with expectations. This was impacted by the lower interest revenue booked on payment arrangement debt due to the sale of some of this debt at the end of last year. Within the revenue performance, interest lines were down low single digits as a result of the debt sale whilst non-interest lines were down high teens percentage as a result of the better quality loan book which reduced admin fees.

The new High and Mighty website will go live shortly and the group remain on track to have all brands replatformed by the end of summer 2018 as previously disclosed. Aside from the exceptional costs in closing the underperforming stores, all other 2018 guidance is unchanged. Overall this update seems decent enough, steady as she goes.

On the 13th July the group announced that it had identified flaws in certain general insurance products which were sold between 2006 and 2014 following a review prompted by a recent industry-wide request from the FCA that firms ensure that general insurance products and add-ons offer value for their customers.

The group expects to incur an exceptional cost this year of between £35M and £40M but they anticipate that there may be mitigating actions to reduce the overall net costs. The cash flow impact of this is forecast to occur from 2019 onwards and they expect to fund the full cost of customer redress from existing resources. Other than this, they continue to demonstrate strong underlying trading performance in line with forecasts.

On the 1st December the group released a half-year trading update. Estimates indicate sales of around £109M and an operating profit of £38M. Over the first half they have seen sales and profit growth in all channels in constant currency terms with the momentum continuing throughout the period. These results are in line with expectations.