Northern Petroleum have now released their final results for the year ended 2016.

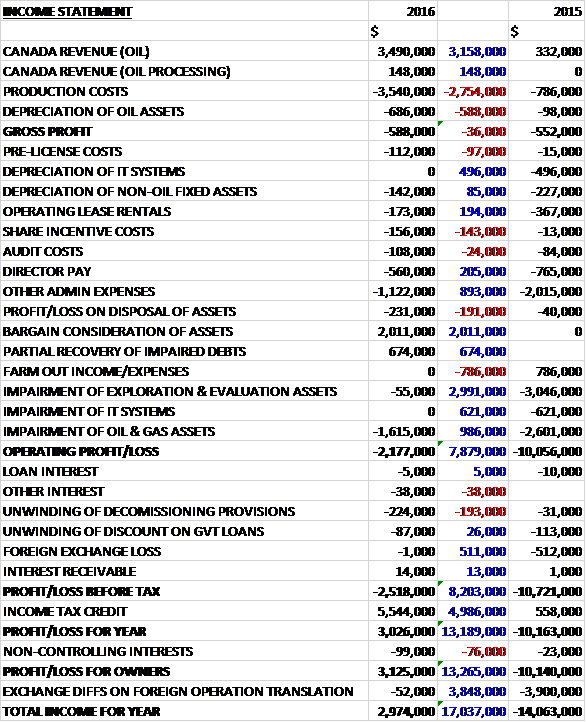

Revenues increased by $3.3M when compared to last year but depreciation was up $588K and production costs increased by $2.8M to give a gross loss $36K higher than last time. There was no depreciation of IT systems which cost $496K last time and other admin expenses also declined. The group also benefited from a $2M bargain consideration for assets and a $674K recovery of impaired debts. There was no farm out income, which brought in $786K last year but also impairments were down $4.6M to give an operating loss which improved by $7.9M. The forex loss declined by $511K and there was a $5M increase in tax credits mainly relating to the recognition of old tax losses, which meant that there was a profit of $3.1M, a positive movement of $13.3M year on year.

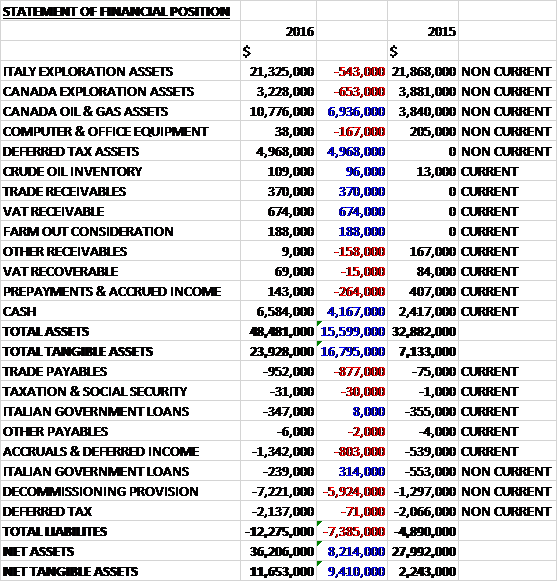

When compared to the end point of last year, total assets increased by $15.6M driven by a $6.9M growth in the Canadian oil and gas assets following the Rainbow asset acquisition, a $5M increase in deferred tax assets and a $4.2M growth in cash. Total liabilities also increased due to a $5.9M increase in the decommissioning provision, an $877K growth in trade payables and an $803K increase in accruals and deferred income. The end result was a net tangible asset level of $11.7M, a growth of $9.4M year on year.

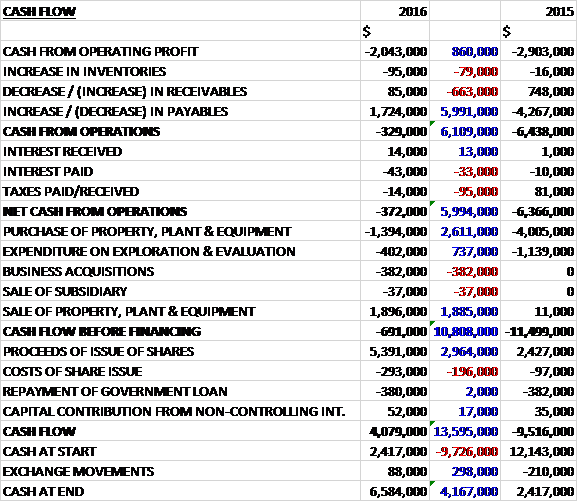

Before movements in working capital, cash losses improved by $860K to $2M. There was a cash inflow from working capital due to an increase in payables which meant that the net cash outflow from operations was $372K, a $6M improvement year on year. The group also spent $1.4M on property, plant and equipment; $402K on exploration and $382K on acquisitions. They did take in $1.9M from the sale of fixed assets, however to give a cash outflow of $691K before financing. The group issued new shares that brought in $5.4M and after share issue costs and $380K repaid on the government loan, there was a cash inflow of $4.1M and a cash level of $6.6M at the year-end.

In January 2016 the group acquired a number of Rainbow area leases in Alberta where the fair value of the assets acquired exceeded the cost of purchasing the assets by $2.7M which is referred to in the accounts as a bargain consideration. The transaction also generated a deferred tax liability of $719K in relation to this, although this was netted off the newly recognised deferred tax asset relating to previous tax losses. Since the acquisition the Rainbow assets have consumed $1.3M of cash.

During the year, two work programmes focused on the Rainbow Assets were undertaken returning ten wells to production that had been previously shut in due to mechanical issues. These work programmes increased total production from about 150boepd at the beginning of the year to 400boepd at the completion of the programme, resulting in a total average production for the year of 290boepd.

Total production for the year amounted to 106,000boe with operating expenditure reduced during the year due to a combination of having acquired two production facilities as part of the Rainbow Asset acquisition significantly reducing third party processing fees, and an industry wise reduction in service company costs reflecting the lower oil price environment. There were two minor reportable oil spills which have been cleaned up.

As a result of the capital raised by the group at the end of 2016, activities in early 2017 have been focused on a winter work programme aimed at working over 20 wells to increase production by 300boepd. These wells had originally been shut in due to mechanical or near well bore issues in the Rainbow area. By the end of Q1, the programme had been completed with the production targets achieved. Planning has now started for an extended summer work programme, which aims to increase production by a further 300boepd.

In Italy, appeals lodged by the Puglia region against these awards were rejected by Italian courts during 2016 allowing the group to continue to plan the seismic programme and work with the Ministry to turn the applications into permits. Subsurface work conducted during 2016 identified the Medusa deep exploration prospect is analogous to the Giove discovery. As a result, subject to ministry approval, the group is proposing to combine the work programmes for permits F.R39 and F.R40 which will allow one well to move both permits into the second licensing period.

The group has drafted an appraisal well EIA for Giove to be submitted during 2017 to drill a well 12 to 18 months after submission. All offshore permits are currently held in suspension pending approvals for the next stage of the work programmes.

In onshore Italy, Shell has made good progress on the exploration work programme at Cascina Alberto with the reprocessing of existing 2D seismic data. They have decided that additional 2D seismic needs to be acquired to provide further imaging of the exploration prospect and establish the most favourable exploration well location. They have now started initial consultations before submitting the EIA for the acquisition programme. The EIA is expected to be submitted to the authorities during 2017.

The oil price hit a low of $27 per barrel early in the year but by the end of the year it was at $53. As of the end of May it was hovering around the $48 mark.

In March 2017 the group received a payment of $674K in respect of a debtor arising from the drilling of the Savio 1x well in Italy. The debt had been written off, transferred to intangible assets and then impaired in 2014 as the recoverability of the debt was uncertain. Due to the strong performance of the Rainbow assets since acquisition and the raising of new finance to further develop these assets, the group recognised their remaining Canadian deferred tax assets in respect of tax losses of $5M.

Although impairments did fall, there still were some this year. Following the receipt of a new reserves report which used lower short to medium term oil price assumptions, the 15-23 well in the Virgo area was impaired by a further $1.4M. The well produced increasing volumes of water in the first half of the year and was shut in pending further evaluation. The directors believe that the value of the well’s production can be enhanced by recompleting the well but this work is not included in the near term work programmes and the well was impaired to its estimated recoverable amount of $444K. The Virgo 11-30 well has also been impaired on the basis of a new reserves report. The well also produced high volumes of water and has been fully impaired by $566K to zero.

In December the group disposed of 25% of their interests in all their Canadian leases and other Canadian oil and gas asserts to H2P for a cash consideration of $2M plus $188K of consideration in kind in the form of well stimulation services provided by H2P’s affiliated company, Blue Spark. This slightly under the book value of the assets so the group booked a loss on disposal of $160K. There was a also a $37K disposal cost relating to transferring the Argentine subsidiary to the local director along with a $34K loss on disposing of computer software and hardware following the group’s decision to migrate to a cheaper solution.

They have agreed further disposals of 10% of their Southern Adriatic permits and applications in Italy for a consideration of $500K and 25% of their Australian license for $1. The regulatory approvals for these last two transactions had not been received by the year-end so they are not reflected in these accounts. H2P has the option to earn additional equity in the Southern Adriatic and Australian permit by fully funding a well in Italy, and seismic acquisition in Australia. They have an additional option to increase their interest in the Canadian assets to 50% if they pay $4M before the end of 2017.

In January 2017, after the year-end the group announced the open offer to shareholders and a further placing of shares which meant that 42,100,000 shares were issued at a price of 3.5p per share, raising a further $1.8M. In March 2017 the group announced the acquisition alongside H2P of six oil wells in the Rainbow area of Alberta. The wells acquired are near the existing ones and the consideration is the assumption of the $1.1M abandonment liability. At the end of March the group had a cash balance of $7.2M.

Overall then this was an important year but the group still haven’t managed to break even. There seems to be a profit due to the tax loss recognition but the underlying loss seems to have improved due to lower admin costs. Net assets increased, as would be expected given the equity raise, and the operating cash outflow also improved. The Rainbow assets seem to have been a good and necessary acquisition and by the end of the summer workovers the group should be producing around 1,000boepd I think which is a big improvement. There is not much happening in Italy and the current oil price isn’t much to get excited about but this company seems to be on the way to being a viable investment.

On the 8th June the group announced the acquisition of onshore production and development gas assets in Italy from Rockhopper. The acquisition comprises a 100% interest in the Aglavizza production concession which contains the producing Civita gas field and associated processing facilities and pipeline, a local operations base and the Scanzano concession (100%), Torrente Celone concession (50%), Monte Verdese Concession (60%), San Basile concession (85%) along with the Civita permit.

Cvita is tied into the national gas network and was commissioned in late 2015 with an average gas production of 130 barrels of oil equivalent per day. It is estimated to contain about 1bcf of recoverable gas. The group is reviewing the potential for the redevelopment of the Cupoloni field in the Scanzano concession and the further subsurface potential of the Vigna Nocelli field in the Torrente Celone concession.

The group will assume the abandonment liabilities of the production concessions which, excluding Aglavizza andf the two fields with redevelopment potential, are estimated to be about €3M and forecast to be incurred over the next ten years. Rockhopper will pay the group $1.6M on completion of the acquisition. The operating profit from the Cvita gas field in 2016 was $900K and represents the group’s first foray into the Italian gas market.

This actually looks to be an interesting acquisition and one which should bring Italy more to the fore. Hopefully it will not distract too much from operations in Canada.

On the 28th June the group announced that it had changed its name to Cabot Energy! This is the first I heard of this – very strange!