Orosur Mining has now released their final results for the year ended 2017

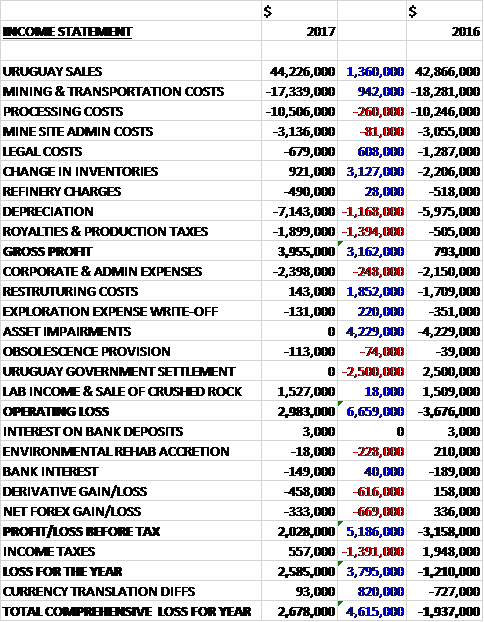

Revenues increased by $1.4M when compared to last year. Mining and transportation costs were down $942K, legal costs fell by $608K and there was a $3.1M positive movement in inventories but processing costs were up $260K, depreciation increased by $1.2M as the SGW UG mine started production in December, and royalties and production taxes grew by $1.4M after last year’s exemption, which meant that the gross profit increased by $3.2M. Admin expenses grew by $248K and there was no Uruguay government settlement which brought in $2.5M last time but restructuring costs declined by $1.9M and there were no asset impairments, which cost $4.2M last time to give an operating profit $6.7M improved on last time. There was a $616K derivative loss relating to a forward contract for up to 6,000 ounces, and a $669K net forex loss with a $1.4M reduction in tax receipts, relating to less deferred tax recognised, all of which meant that the profit came in at $2.6M, an improvement of $3.8M year on year.

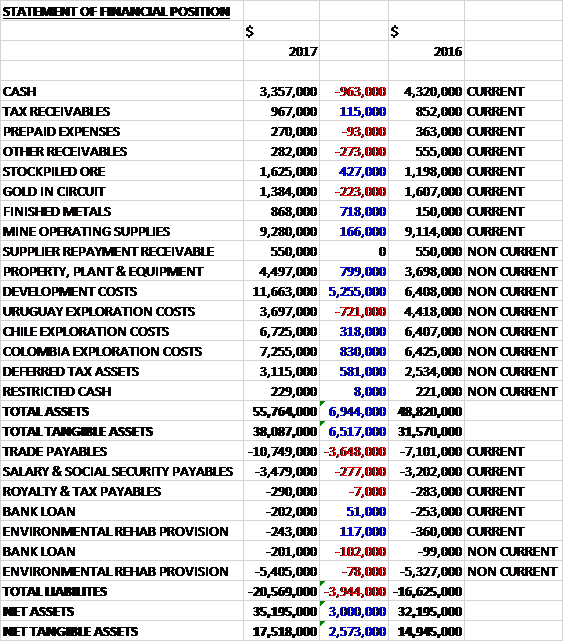

When compared to the end point of last year, total assets increased by $6.9M driven by a $5.3M growth in development costs, mainly relating to underground development, an £830K increase in Colombian exploration costs, a $799K increase in property, plant and equipment and a $718K increase in finished metals inventory, partially offset by a $963K decrease in cash and a $721K decline in Uruguay exploration costs which were transferred to tangible assets. Total liabilities also increased, due to a $3.6M growth in trade payables. The end result was a net tangible asset level of $17.5M, a growth of $2.6M year on year.

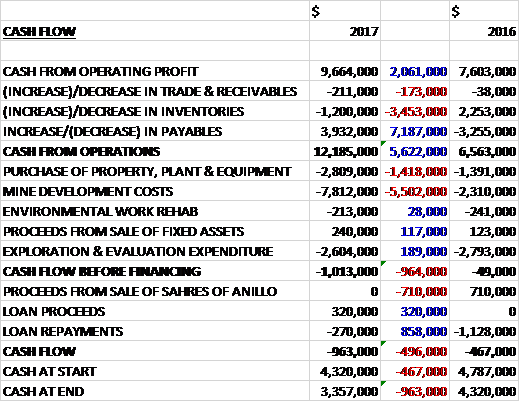

Before movements in working capital, cash profits increased by $2.1M to $9.7M. There was also a cash inflow from working capital due to an increase in payables, partly relating to a legal provision of $700K related to labour claims and a huge increase in activity in Q4, and the cash from operations was $12.2M, a growth of $5.6M year on year. Unfortunately this did not cover the $7.8M of mine development costs representing the construction of the SGW UG ramp, access and ventilation shaft along with the construction of phase 4A of the tailings dam during the year, the $2.8M of property, plant and equipment expenditure and the $2.6K of exploration costs so there was a cash outflow of $1M before financing. The group took out a small net loan so there was a cash outflow of $963K for the year and a cash level of $3.4M at the year-end.

During the year, 978,529 tonnes of ore was processed at a grade of 1.21g/t with recovery averaging 93.41% compared to 1,013,104 tonnes at a grade of 1.19g/t with recovery averaging 92.54% last year. A total of 4,088,407 tonnes was mined, comprising 3,154,434 tonnes of waste and 933,973 tonnes of ore with an average grade of 1.24g/t. This compares to 3,209,063 tonnes comprising 2,283,480 tonnes of waste and 925,583 tonnes of ore with a grade of 1.24g/t.

Production for the year was 35,371 ounces of gold, at the bottom end of the stated guidance of 35,000-40,000 and slightly below the 35,773 ounces produced last year, although there was a significant increase to 10,748 ounces in Q4. The average gold price realised for the year was $1,258 per ounce, an increase of 9% over last year. Cash operating costs for the year were $829 per ounce, a reduction of 6% due primarily to lower operating costs related to lower tonnes transported and processed at higher recoveries during the year. All in sustaining costs were $1,228 per ounce compared to $1,069 per ounce. This increase was due to the additional development capex associated with the SWG underground mine, including ramp, access and ventilation work as well as the royalty exemption from last year expiring.

The SGW UG mine made a gross profit of $4M compared to $793K last year with the improvement mainly due to a higher realised gold price and lower overall costs of sales.

The San Gregorio West Underground mine started full production at the end of November, following a transition period. Construction this year included horizontal development of 2,179m, including 771m of mineralized development and a ventilation shaft, with raise boring having completed in December. This represents about 59% of the total development planned at the mine. The project was approved by the Ministry of Finance in January which allows the group to benefit from certain tax programmes available in Uruguay to promote domestic investments.

In Colombia the group finalised a geological model of its high grade Anza gold project to determine the exploratory potential with the assistance of Mine Development Associates. The project includes a gypsum mine which has environmental and mining permits granted by the Colombian authorities. The gypsum permits can be readily expanded for additional tonnage, providing the ability for the group to fast track permitting for future gold mining operations. The group is preparing to start a 15,000m drilling campaign at Anza.

In June the group granted Asset Chile an extension to decide whether it will proceed with Phase 2 at Anillo. They have until the end of December to make that decision. In exchange, Asset Chile agreed to pay care and maintenance costs of the Anillo property and the related office costs in Chile and have no objection to the group presently entering into discussions with third parties for the purpose of farming out the property should Asset Chile decline to further participate. Asset Chile has to complete its required contribution to Phase 2, up to $1.25M to fund 5,500m of RC drilling, in order to earn into a 32.5% interest in the group’s share in Anillo. In the event that they don’t complete the Phase 2, they will forfeit their earn-in achieved to date.

At Pantanillo, Anglo and the group signed in May the re-purchase of the properties by Anglo in line with the decision made to discontinue with the project. The group has therefore given the mining concessions of the project back to Anglo in June. At Talca in Chile, the group conducted a property review to try to generate value from the asset. Some field work was undertaken to obtain relevant information and the property was presented to potential investors.

At Noiletir in Uruguay, the parties are waiting for the government’s grant of new mining licenses in order to continue with the exploration campaign. At Minerales Cala in Uruguay, the group elected not to contribute to phase 3 expenditures and its interest in the project was reduced to a Net Smelter Return Royalty of 2%.

In August 2016, Gladiator announced their intention to dispose of their current interest under the Option Agreement and in September notified the group of an offer received proposing to purchase all of their interest. The group has concluded that the offer is not compliant with the Option Agreement and therefore can’t be accepted in its current form. Gladiator went ahead anyway and in December executed a binding agreement with a third party to dispose of its interests in the project, and in February, without the group’s consent, they completed the sale to Metamila, a Belize-based company. The group considers this a breach of contract and intends to take all steps necessary to remedy the situation.

Obviously the group is very susceptible to movements in the gold price, even more than most. They stand to gain/loose $4.4M of profit for every 10% movement in the gold price. They are also somewhat susceptible to exchange movements between the Peso and the US dollar, with the Peso appreciating by 9% during the year.

After the year-end, in August, the group raised gross proceeds of $3.2M through a placing and subscription of 16,740,502 new shares at a price of 24.1c per share, together with a grant of unlisted warrants over new shares on the basis of one subscription warrant for every two shares. The net proceeds are intended to be deployed for drilling and associated activities at the Anza gold project in Colombia.

The group expects production from the San Gregorio mine to be between 30,000 and 35,000 ounces of gold with operating costs of $800 to $900 per ounce compared to 35,371 ounces achieved this year at $829 per ounce. At current gold prices this will allow the group to continue to focus on expanding its resource base in Uruguay both from underground and surface operations, with the aim of increasing mine life and increasing production by utilising the spare capacity in the San Gregorio plant.

At the current share price the shares are trading on a PE ratio of 9.8 which falls to 3.1 on next year’s consensus forecast.

Overall then this has been a decent period for the group. They are now profitable, having made a loss last year, net assets increased and the operating cash flow improved, although there is still no free cash due to the investments made in SGW UG, which seems to have started up with little in the way of issues. There was less ore processed which meant less gold produced but the profit was due to an increase in the gold price and a reduction in costs. Going forward the group is expecting to make slightly less gold in 2018 which, to me, suggests the forecast PE of 3.1 is a little low and the current PE of 9.8 is probably a bit more likely.

Tricky one, the group as it stands is just about self-sufficient as far as cash is concerned but needs to tap up the market for investment in order to further its other assets. I’m tempted but I feel there is little immediate prospect of shareholder returns at the moment. This would change with a significant hike in the gold price though.

On the 21st September the group announced an update covering exploration and development in Uruguay. In the half year total production was 12,600 ounces of gold and the current remaining probable reserves are 34,633 ounces, which doesn’t sound like much. They are currently on track to meet their 2018 production guidance.

Three Uruguay exploration activities are planned to be further developed in 2018. The plan is to increase the amount of drilling next to the existing CIL plant and within the 100km long greenstone belt which they control in Uruguay with the aim of increasing mine life and increasing production by utilising the spare capacity in the plant. In addition to these underground projects, they are also planning to drill out projects beyond San Gregorio such as Veta A.

Vita A represents a potential project for a new underground mine. Historically it was a relatively small high grade open pit, located next to the San Gregorio tailings dam which was in operation until March 2008. The open pit produced around 29,000 ounces at average grades of 3.1g.t. As open pit mining progressed, the mineralised body appeared to run underneath the tailings dam. When operations approached this physical barrier, mining was halted and the pit was backfilled. Probable reserves in the zone are 9,440 ounces. A re-evaluation of the body below the dam is currently underway.

An updated geotechnical study of the deposit was performed during the quarter. Results indicate that, providing required preventative measures are undertaken, there are no subsidence, liquefaction or any other negative interactions between the closed tailings dam and potential future underground mining operations.

In parallel, a drilling campaign provided encouraging preliminary results. Of the four holes drilled, each intersected mineralisation, confirming the extension of the mineralised body for a minimum of 140m downhole. This indicates the strong potential for an increase in the volume of mineralised structure which may materially increase current reserves. Further drilling continues in order to confirm and expand its reserve base.

Given the data available and the underexplored nature of the Isla Cristalina Granite Greenstone Belt, the group believes there is scope to make material discoveries in excess of 100,000 ounces of reserves. The San Gregorio trend by itself has produced more than 1.4M ounces of gold.

On the 2nd October the group announced they will be starting their drilling campaign at Anza in Colombia in October.

On the 19th October the group announced the arrival of the second diamond drill rig at Anza in Colombia which commenced drilling on the same day. Preliminary geological reconnaissance of the core indicates geological features similar to previous drilling and is considered a promising host rock. This tends to coincide with historical drilling in the sector which yielded high gold grade intersections. Core sampling will be done as soon as the drill hole is logged.

Ten drilling platforms completed with access roads have been constructed and are ready to be drilled in sequence over the coming months. The group plans to drill around 35m per day per rig and aims to have four holes drilled and ready for analysis by the end of October.