Dechra Pharmaceuticals has now released their final results for the year ended 2017.

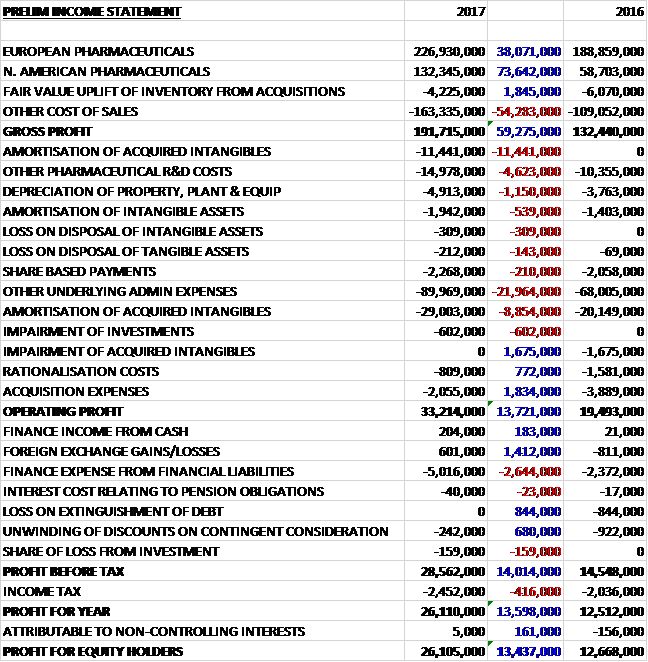

Revenues increased when compared to last year with a £73.6M growth in North American sales and a £38.1M increase in European sales. Cost of sales also grew to give a gross profit £59.3M higher. The amortisation of acquired R&D intangibles increased by £11.4M and other R&D expenses were up £4.6M. Depreciation was up £1.2M and other underlying admin expenses increased by £22M. We also see an £8.9M increase in other amortisation of acquired intangibles which offset last year’s £1.7M impairment. Rationalisation costs were down £772K and acquisition expenses reduced by £1.8M to give an operating profit £13.7M higher than last year. There was a £1.4M positive swing to a forex gain and no loss on the extinguishment of debt but finance expenses from financial liabilities increased by £2.6M and the tax charge grew by £416K to give a profit for the year of £26.1M, a growth of £13.4M year on year.

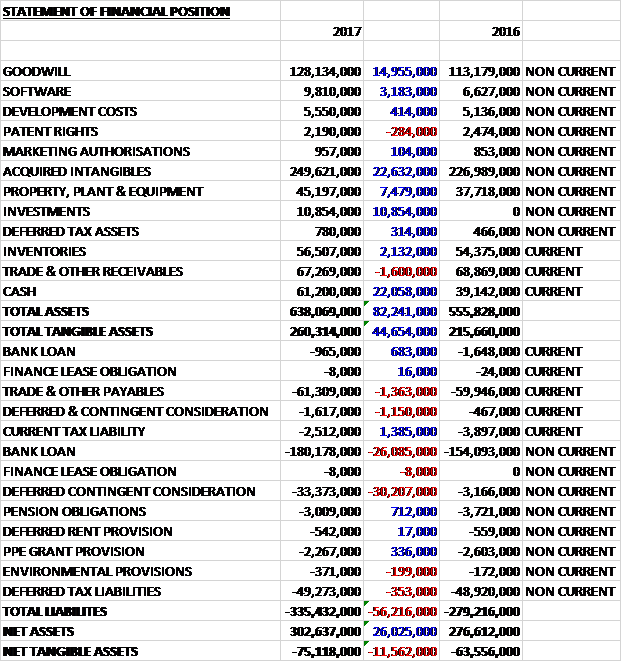

When compared to the end point of last year, total assets increased by £82.2M, driven by a £22.6M growth in acquired intangibles, a £22.1M increase in cash, a £15M growth in goodwill, a £10.9M increase in investments, a £7.5M growth in property, plant and equipment and a £3.2M increase in software. Total liabilities also increased during the year due to a £25.4M increase in bank loans and a £30.2M growth in deferred consideration. The end result was a net tangible asset level of -£75.1M, a detrimental movement of £11.6M year on year.

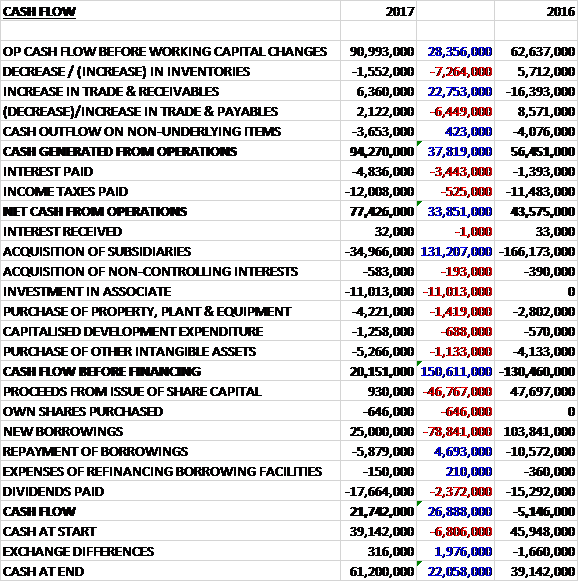

Before movements in working capital, cash profits increased by £28.4M to £91M. There was a cash inflow from working capital but interest payments increased by £3.4M and tax payments were up £525K to give a net cash from operations of £77.4M. This covered the £35M of acquisitions, the £11M of investments in an associate, £1.3M of development expenditure, £5.3M of other intangible asset purchase and £4.2M of other capex to give a free cash flow of £20.2M. This covered the £17.7M of dividends but the group still took out a net £19.1M of new loans to give a cash flow of £21.7M and a cash level of £61.2M at the year-end.

The operating profit in the European Pharmaceuticals division was £60.7M, a growth of £9.1M year on year, of which £4.7M came from acquisitions. Like for like revenues, excluding third party contract manufacturing increased by 5.3%. Third party manufacturing revenues declined by 9.7%, representing a conscious strategic move as the group start to implement an efficiency improvement plan.

Companion animal product sales were the predominant driver of revenue growth in the core EU business with farm animal and equine also delivering growth of 1.3% and 0.7% respectively. The UK, France and Germany performed well and there was also strong revenue growth in Italy and Poland. After a slow start, the recently formed subsidiary in Austria started hitting expectations. Companion animal revenue increased by 9%, driven by a strong performance of Zycortal, the endocrine product launched last year, and from established products such as Cardisure, Vetoryl and the analgesia and anaesthesia range.

The farm animal portfolio has delivered its second successive year of growth, albeit modest. This performance is set against a historical decline in antibiotic sales due to concerns over antimicrobial resistance. Despite this, the group is beginning to see signs of a recovery in sales of their water soluble antibiotics. They believe that their Solustab range is now well positioned to provide vets with a robust portfolio of suitable options for prudent use of antibiotics in the treatment of the majority of infectious diseases in pigs and poultry.

The first of the poultry vaccines developed for the EU, Avishield, was launched in Germany, the Netherlands and Belgium. Although they do not yet have a full range to offer customers, they were still able to gain a market share of about 15%.

The equine portfolio growth has predominantly been driven by Osphos, although they believe that sales are a long way from reaching full potential and will continue to grow as vets gain a better understanding of this treatment. Generic competition to Equipalazone, a long standing product in the portfolio, partly offset the sales growth in this category.

The nutrition and diets market continues to be very competitive. They are maintaining sales of their brand Specific, following historical supply issues and are initiating a number of projects that they hope will re-invigorate the range in the near term. They have, towards the end of the year, launched two new hypo-allergenic wet diets for dogs and cats.

The overall business benefited from a full year’s contribution from Genera and eight months contribution from Apex. Apex is performing well with the recently modernised factory achieving regulatory approval from the Australian authorities in April.

Good progress has been made on the integration of Genera. Significant cost savings have been delivered from the staff layoffs and major improvements have been made in the solid close and liquids manufacturing facilities, into which new products are being transferred to benefit from this low cost location. The primary reason for the acquisition was to access their range of poultry vaccines for broilers and the first of these has now been launched. The next five are in registration and progress is being made with a further four products.

The operating profit in the North American business was £43.2M, an increase of £25.7M when compared to last year, of which £18.7M came from acquisitions. Like for like sales were up 16.5% with the US and Canadian businesses both performing well. The principal drivers of the growth are companion animal and equine products with excellent sales of Zycortal, Vetivex and Osphos.

A number of new products were launched in the year including Amoxi-Clav, the first major product approval from Putney; three new extensions to the Vetivex range; Carprovet flavoured tablets to increase their companion animal pain management range; and two topical dermatology products in a new mousse format.

Overall the division benefited from a good performance by Putney. The integration has been implemented well, significant cost savings have been delivered, new sales channels opened and sales synergies from the enlarged team have been delivered to both Putney and existing product ranges. The Mexican business, Bovel, acquired in January last year continues to focus on the registration of Dechra products with initial approvals having been received. A new management team was appointed during last year and there has been a notable improvement in performance.

During the year, the most significant approval was for a generic antibiotic tables, Amoxi-Clav. Other significant registrations have been Revozyn, a cattle antibiotic for mastitis, in the Netherlands, UK and Germany with applications having been made for a further ten European markets; Cyclospray aerosol and Vetoryl 5mg in Canada; Cardisure, Zycortal, Osphos, Doxy paste and Benazapril oral solution in Australia; Osphos in Mexico; Isathal and Canaural in Korea; Domidine, Atipam and Sedator in Thailand and South Africa; and Altidox, a water soluble antibiotic, in 13 EU countries.

They have also signed three agreements to conduct proof of concept studies on new and potentially material pharmaceuticals for the veterinary market and have licensed a range of companion animal generic tablets form a key partner for Europe, a dental and dermatological product from Kane Biotech for the US and Canada, and a dermatological product from Premune for the EU.

In March the group acquired a 33% interest in Medical Ethics for £11M. They also announced that they had entered into a long term IP licensing agreement with Animal Ethics, who are an Australian-based company focused on developing ethical pain relief products for animal health. This agreement gives Dechra the rights to sell and market Animal Ethics’ product Tri-Solfen for all animal species in all markets except Australia and New Zealand. Tri-Solfen is a topical product that is sprayed onto wounds which relieves pain, controls bleeding and protects against infection for routine treatments in farm animals.

In October 2016 the group acquired Apex Labs, a veterinary pharmaceuticals company based in Australia. The cash consideration was £34.2M and the acquisition generated goodwill £9.9M and other intangible assets of £21.3M. The business contributed £1.1M to group pre-tax profits and had the acquisition been completed at the start of the year, it would have generated £2.1M. The business is reporting in the EU segment. Clearly Dechra are following the same definition of Europe as Eurovision! The principal reason for the acquisition was to provide the group with direct access to the Australian markets.

Towards the end of the year the group established a new business unit, Dechra Veterinary Products International. To focus on increasing their international presence. Currently sales outside their core markets are farm animal based and the group believe that their products in the pig and poultry markets will provide them with an entry opportunity into markets where quality meat consumption is increasing strongly. In the longer term they are targeting companion animal markets which are beginning to gain growth momentum in several developing countries.

As mentioned above the group are reducing third party manufacturing contracts. This was historically important business to utilise capacity in the factories but the increased scale of their own production is now being hindered by a number of these low margin contracts. They will therefore be exiting most of these contracts over the next five years, only retaining a few significant, high volume partnerships. Following the recent acquisitions, in-sourced production accounts for about 50% of all product sales. They have identified opportunities to reduce the complexity of their supplier network by working with preferred partners and bringing more of the outsourced production in-house.

The group continue to focus on the implementation of the Oracle ERP solution which had fallen behind schedule. They now believe that good progress has been made and they are confident that a go live can be implemented prior to the end of 2018.

Going forward, current trading is in line with board expectations and they anticipate delivering their strategic objectives in the new financial year.

At the current share price, the shares are trading on a PE ratio of 69.8 which falls to 26.6 on next year’s consensus forecast, no doubt ignoring the slew of intangible amortisation that the “underlying accounts” don’t include. After a 16% increase in the dividend the shares are yielding 1.1% which remains the same for next year’s forecast so these shares are definitely not cheap. At the year-end the group had a net debt position of £120M, an increase of £3.4M year on year.

On the 4th September director Richard Cotton purchased 8,481 shares at a value of £167K which seems like a decent purchase.

Overall then this seems to have been another year of progress. Profits increased along with the operating cash flow with a decent amount of free cash being generated. The issue I have is the deteriorating tangible asset base which is now considerably negative. The European business performed fairly well, driven by improvements in companion animal sales, and the North American division also performed well due to companion animal and equine products. The shares are not cheap, however, with a forward PE of 26.6 and yield of 1.1% but there has been a director purchase and I am holding on for now.

On the 20th October the group released a trading update covering Q1 where they stated that their performance was in line with management expectations with continued growth across all markets.

On the 9th January the group released a trading update covering the half year which was in line with management expectations. Reported group revenue increased by 10.5% at constant currency. The European pharmaceuticals segment reported revenue increased by 5.5% at constant currency. Excluding third party contract manufacturing and treating Apex on a like for like basis, revenues were up 4%. North American revenues were up 20% at constant currency.

New product registrations were achieved in the period. In Europe, this included Avishield IBH120, the second EU-registered poultry vaccine; and a number of minor registrations were achieved in the international division following its formation in July. In North America, they have now launched all the dosage sizes of Amoxi-Clav tablets in the US and Vetoryl and Osphos in Mexico.

In December the group completed the acquisition of RxVet, a small CAP business in New Zealand. They have been the group’s distributor in the country since 2010 with revenues of $1.4M, half of which were Dechra products.

Following the passing into law of the Tax Cuts and Jobs Act in the US, the group is in the process of reviewing its effect. Overall, an initial provisional assessment indicates that the effect is expected to be modestly favourable on an ongoing underlying basis. A material one-off non-cash credit will arise due to the revaluation of deferred tax balances. Overall this all seems fine.

On the 25th January the group announced the acquisition of AST Farma and LE Vet for a total consideration of €340M to be satisfied approximately 75% in cash and 25% in new Dechra shares. AST Farma is one of the leading companion animal pharmaceutical companies in the Netherlands, focused on generic products. Le Vet has focused on the European markets outside the Netherlands and together the two companies hold around ninety product registrations.

The group has also announced the placing with institutional investors of 5,121,952 new shares at a price of £20.50 per share, representing around 5.5% of the group’s existing share capital. The proceeds will be used to fund the acquisition along with existing resources and the issue of 3,670,625 new shares to the vendors.

The group has worked with both businesses for a number of years since the acquisition of Eurovet in 2012. In more recent years the relationship has expanded through further distribution agreements for certain products and was further enhanced when Dechra acquired Genera. Dechra is already distributor for AST Farma and Le Vet’s products in the UK, Ireland, France, Italy, Norway, Sweden, Denmark, Spain, Portugal, Poland, Slovenia, Croatia, Bosnia, Serbia, Macedonia and Kosovo, representing around 13% of their turnover.

The board believe the acquisition will provide critical mass in the Netherlands and enable to the group to access the direct to vet model, eliminating the need from distributors. The acquisition also provides access to over thirty products in the pipeline, including eight already submitted for EU registration. It is expected to be materially earnings enhancing for 2019 and to deliver returns in excess of the cost of capital in a timely manner.

Strangely the manufacturing and product development activities are not included in the sale and will still be owned by the vendors which means the group will still have to source from them. AST Farma made pre-tax profit of €8.9M last year and LE Vet €2.3M. The businesses don’t own much in the way of assets so the acquisition will be generating goodwill of €331.9M.

Overall this looks like an interesting acquisition, albeit rather costly in my opinion. I am also a little concerned about the increasingly flimsy balance sheet but I will continue to hold for now.