Somero has now released its interim results for the year ending 2017.

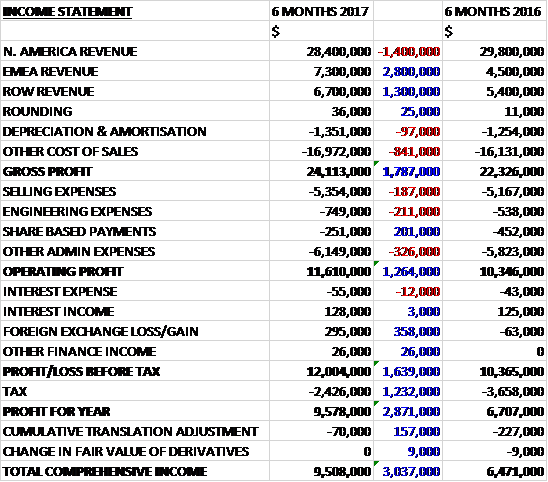

Revenues increased when compared to the first half of last year as a $1.4M decline in North America revenue was more than offset by a $2.8M growth in EMEA revenue and a $1.3M increase in ROW revenue. Depreciation was up $97K and other cost of sales grew by $841K to give a gross profit $1.8M higher. Selling expenses increased by $187K, engineering expenses were up $211K but share based payments fell by $201K with other admin expenses up $326K to give an operating profit $1.3M higher than last time. There was a $358K swing to a forex gain and tax charges fell by $1.2M which meant that the profit for the period was $9.6M, a growth of $2.9M year on year.

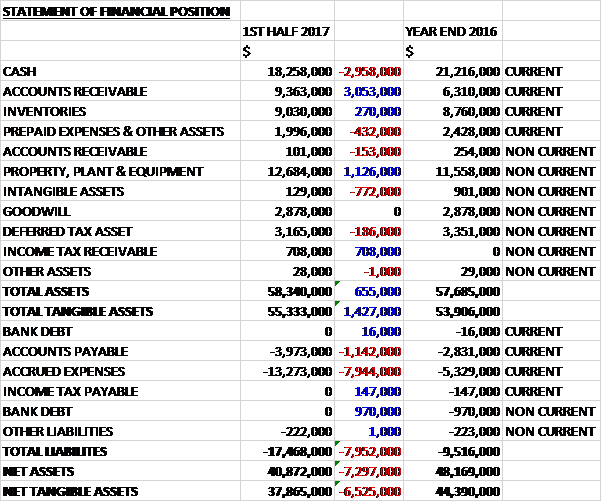

When compared to the end point of last year, total assets increased by $655K driven by a $3.1M growth in accounts payable, a $1.1M increase in property, plant and equipment, and a $708K increase in tax receivables, partially offset by a £3M fall in cash and a $772K decrease in intangible assets. Total liabilities also grew during the period as a $986K reduction in bank debt was more than offset by a $7.9M growth in accrued expenses and a $1.1M increase in accounts payable. The end result was a net tangible asset level of $37.9M, a decline of $6.5M over the past six months.

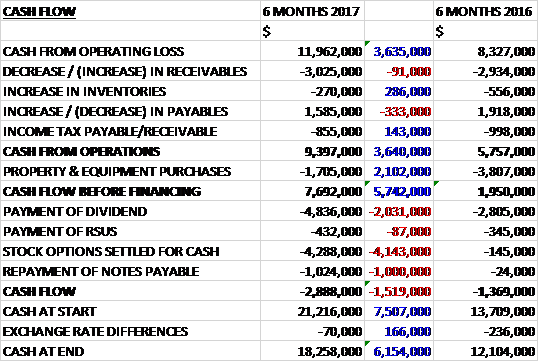

Before movements in working capital, cash profits increased by $3.6M to $12M. There was a cash outflow form working capital which was broadly similar to last time so the cash from operations was £9.4M, a growth of $2.1M year on year. The group spent $1.7M on capex to give a free cash flow of $7.7M. Of this, a massive $4.3M was spent on stock options, $1M was used to pay off debt and $4.8M went on dividends to give a cash outflow of $2.9M and a cash level of $18.3M at the period-end.

Despite the fall in revenue, the North American market remains healthy and customers continue to report extended project backlogs. The period ended with June at the highest levels of the year as weather conditions across the country improved and the heavy rains seen throughout the first half began to subside. There was a high level of activity in the market that has carried forward which supports management expectations for a solid H2.

The European market saw a strong performance in the period with sales more than doubling as the recovery in the region accelerated and economic conditions improved. The most significant contributions came from the UK, Germany and the Czech Rep.

In China, the slow start to the year saw sales decline by $1.1M to $2.7M but they ended the period on a positive note with June trading at the highest level of the year. They expect to build on this momentum and see improvements in the second half driven by marketing, sales execution, and lead generation activities focused on existing and new entry level products. In addition, experience with the China long-term financing programme remains positive and in line with previous reporting.

Latin America sales were strong, increasing by $1.5M to $1.7M driven by meaningful contributions from Mexico and Peru. In the Middle East, sales were down $600K to $800K but there was a solid pipeline of opportunities for the second half. Sales in the rest of the world grew by $1.5M to $3.4M with Korea and Scandinavia the most significant contributors to growth and with Australia and India also reporting sales increases.

During the period the revenue growth was in part driven by new products introduced late last year and early 2017, specifically the S-158C in China, the SP-16 Concrete Line Pulling and Placing System, and the next generation 3D Profiler System. Overall these products contributed $1.4M of growth.

In April the group completed the construction of the training facility in Fort Myers and launched the Somero Concrete Institute by holding the first training class through which ACI certification was offered to attendees.

In June the board approved plans to build a $1.3M expansion to the HQ to accommodate future growth. The building project is on track to be completed in H1 2018 with the majority of the spend to occur in Q1 2018. This investment is needed to support the future growth of the business and the planned hiring of additional sales, customer support and product development staff.

Going forward, the positive trading momentum experienced at the end of the period in North America has carried over to the second half and the board have confidence in their expectations for a solid performance in the region for the rest of the year. They also expect the trading momentum to continue in Europe and in China they expect to build off the improved trading in June and improve the performance in the second half. Overall, with the solid first half performance and healthy momentum carrying into the second half, the board expects the group to deliver a year of growth in line with current market expectations.

At the current share price the shares are trading on a PE ratio of 14.4 which falls to 13.1 on the full year consensus forecast. After a 10% increase in the interim dividend, and including the special dividend, the shares are yielding 6.7% which increases to 7% on the full year forecast. At the period-end the group had a net cash position of $18.3M compared to $20.2M at the year-end.

Overall then this has been another decent period for the group. The profit increased and the operating cash flow grew but at least half of the free cash was used for stock options. The balance sheet looks a little confusing, however, as the net assets took a dive. This was due to a growth in accrued expenses but there seems to be no mention of these anywhere in the report which is a little concerning (could be the special dividend perhaps?)

Operationally, North America was a bit sluggish but this seems to have improved later in the half and the second half is expected to be pretty decent. Europe looks very strong but China remains a bit tricky. Overall though the strong net cash position, forward PE of 13.1 and yield of 7% looks pretty good and I remain a holder.

On the 12th January the group released an update covering the whole year. The group has delivered strong, profitable growth and healthy cash generation since the end of the first half, exiting the year with its strongest trading month. As a result of the strong H2 performance, the board now expects 2017 revenues will be slightly ahead of market expectations of $84.7M, EBITDA will be comfortably ahead of expectations of $26M driven by the volume increase and effective operating cost management, while net cash is expected to be at least $18.5M, well ahead of market expectations of $16.5M.

Of the growth, $1M has come from new product revenues and $5M in net increased revenues from non-US territories with strong contributions from North America, Europe and ROW. In North America, H2 trading grew as the pace of boomed-screed sales increased and as sales of ride on screeds, 3D profiler systems and parts and accessories all contributed to growth. The high level of activity in the US reflects strength in the underlying commercial construction industry and the strong pipeline of projects that remain in front of the US customer base.

Europe contributed significantly to growth reflecting the region’s broad-based accelerating economic recovery and the group’s investments to increase sales coverage. The ROW region also contributed significantly to growth with India the most significant contributor which has been driven by the addition of in-country sales leadership. In China, trading grew driven by recent demand generation and marketing initiatives as the group works to gain traction in the market. In Latin America trading was down, as with the Middle East.

On a product basis, demand in H2 was balanced across the product range with particularly strong contributions from the boomed-screed and ride-on screed categories as well as from parts and accessories sales driven by a high level of utilization of the installed base of equipment world-wide. A key contributor to growth also came from new products, led by the SP-16 concrete line pulling and placing system.

The group expects its future US earnings and cash flows to be positively impacted by the recently enacted changes to US corporate tax rate from 35% to 21%. Included in the law change is a one-time deemed repatriation tax on cumulative foreign-sourced profits. While the analysis is not complete, the group expects this will not be material and more than offset by the benefit of lower US corporate tax. They are also reviewing the re-measurement of their deferred tax position which will be reflected in a one-off, non-cash charge included in the 2017 results.

Going forward, the board is confident of their ability to deliver another year of profitable growth in 2018 as the underlying market conditions in their core markets remain positive and as they continue to see significant growth opportunities in their other territories. Their confidence is further supported by recently enacted pro-growth US corporate tax law changes which are expected to stimulate increased economic activity in their largest market.

The board plans to review the group’s cash position alongside cash requirements for 2018 as part of their review for the final dividend for 2017. They have concluded the growth and increased complexity of the business necessitates an increase to the level of net cash to be maintained by the company to a minimum of $15M at the year-end each year going forward. A cautious approach but one I am comfortable with.