Redrow has now released their final results for the year ended 2017.

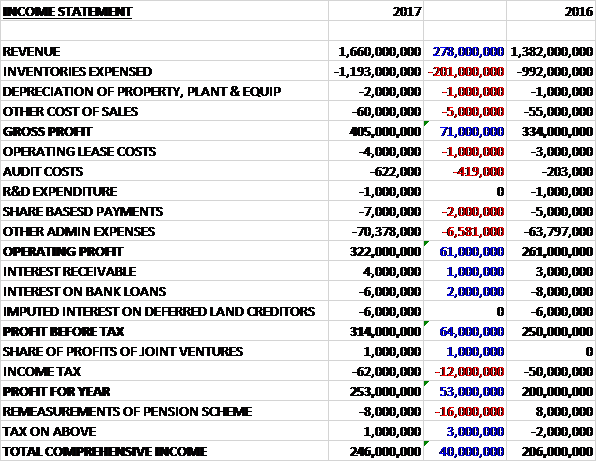

Revenue increased by £278K and inventory costs grew by £201M with a £1M increase in depreciation and a £5M growth in other cost of sales which meant that the gross profit was £71M higher. Operating lease costs grew by £1M, share based payments were up £2M and other admin expenses increased by £6.6M to give an operating profit £61M higher. Interest receipts increased by £1M and interest payments fell by £2M but tax charges grew by £12M which meant that the profit for the year was £253M, a growth of £53M year on year.

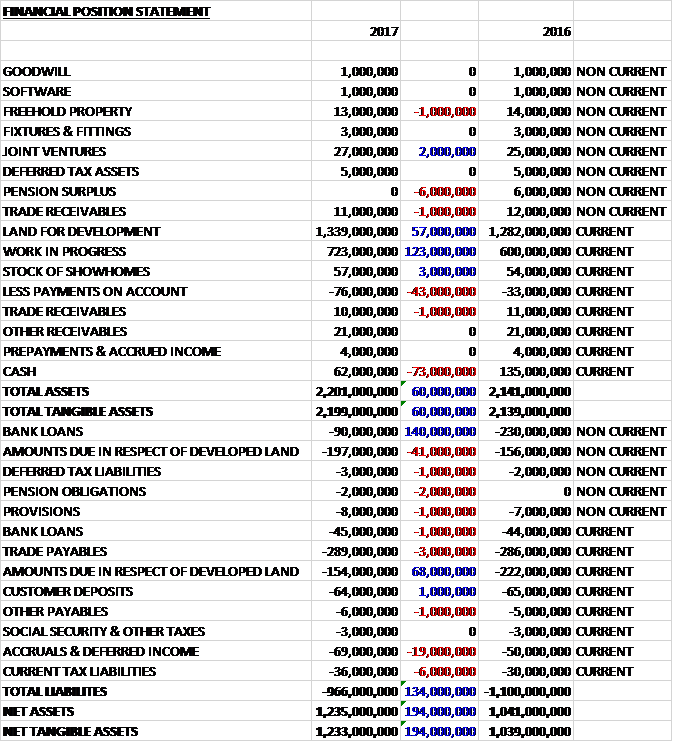

When compared to the end point of last year, total assets increased by £60M driven by a £137M increase in inventories, partially offset by a £73M decrease in cash. Total liabilities declined during the year as a £19M growth in accruals and deferred income was more than offset by a £42M decline in bank loans and a £27M fall in amounts due in respect of developed land. This all meant that net tangible assets came in at £1.233BN, a growth of £194M year on year.

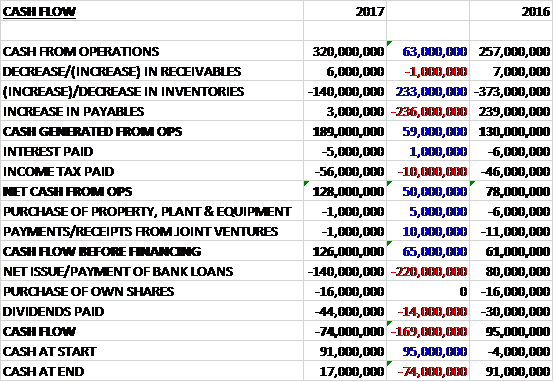

Before movements in working capital, cash profits increased by £63M to £320M. There was a cash outflow from working capital and after tax payments increased by £10M there was a net cash from operations of £128M, a growth of £50M year on year. The group spent just £2M on capex to give a free cash flow of £126M. This was used to pay back £44M of dividends, buy £16M of their own shares and to pay back £140M in loans to give a cash outflow of £74M and a cash level of £17M at the year-end.

Group turnover rose by 20% due to a combination of an increase in legal completions to 5,416 and a 7% rise in the average selling price to £310K. This was mainly due to the continued growth of the Southern business. Gross margin improved by 20 basis points to 24.4% and is now at close to normal levels as they have completed construction on almost all the sites purchased before the downturn.

Overall housing transactions in the UK have reduced as a consequence of the political uncertainty and increased cost of moving home such as stamp duty. Demand in the new homes market remains robust, however and the group has not seen any impact from recent political events. Mortgage availability is good and interest rates on mortgages have again improved. The Help to Buy scheme continues to support the new homes industry and this year 1,882 of the group’s private reservations used the scheme.

They have now substantially completed their high-end Central London developments. Significant volumes of completions are now coming from their outer London sites and these are set to increase materially as Colindale completions begin to come on stream later in the year. Overall he rate of growth is expected to moderate, however, as divisions reach optimal scale and scope for divisional expansion reduces.

In the year the group added 5,419 plots with planning and marginally increased their owned and contracted land bank to 26,100 plots. In the first half of the year, immediately following the Brexit vote, there were fewer opportunities in the land market and they also adopted a more cautious approach. In the second half, momentum returned to their land buying and they added 3,703 plots. Overall they increased the forward land bank to 26,400.

They saw planning improve following the introduction of the National Planning Policy framework in 2012. There are now signs this improvement has stalled, however, as local authorities fail to get Adopted Local Plans in place. This is adding to delays that continue to frustrate the detailed planning and technical approval process. They have also seen timescales for appeals extend which reduces the pressure on local authorities to make timely decisions.

The group’s caution in the land market in the first half combined with planning delays will inevitably impact on the timing of new outlets coming on stream. As a consequence outlets are only expected to marginally increase over the coming year but with their strong land bank and output per outlet continuing to increase, they remain on track to meet their growth plans.

In February the group acquired Radleigh Homes, a Derby-based regional housebuilder. This acquisition has allowed them to accelerate the opening of a new East Midlands division and has given a good pipeline of sites from which to expand. It has now been fully integrated into the group and has made a positive contribution in the second half.

The chairman, Steve Morgan, has announced that he is moving away from a full time role and will become a non-executive chairman.

Going forward, the group has started the new financial year with a record order book, up 14%. Sales in the first nine weeks are encouraging, up 8% on a strong comparator last year. They are therefore upping their medium term guidance with turnover in 2020 of £2.2BN and pre-tax profit of £430M. they expect the dividend in 2020 to rise to 32p per share which would equate to a yield of around 5.8% at today’s share price. Of course this is assuming market conditions don’t change..

At the current share price the shares are trading on a PE ratio of 7.9 which falls to 7 on next year’s consensus forecast. After a 70% increase in the total dividend the shares are yielding 3.1% which increases to 4% on next year’s forecast. At the year-end the group had a net debt position of £73M compared to £139M at the end of last year.

On the 12th September the group announced that Chairman Steve Morgan was selling 25.9M shares at a value of £152.8M. This represents around 7% if the total group share capital! He will still hold 33% of shares, however, and it should be noted that this coincides with him moving from executive to non-executive chairman so I’m not overly worried by this. It could be that he has seen the peak of the market or it could be just that he wants to take on new ventures. Time will tell.

Overall then this has been another year of good progress for the group. Profits were up, net assets increased and the operating cash flow grew with a decent amount of free cash being generated. The good performance has come both from an increase in average selling price, due to product mix, and an increase in the number of completions. Growth is likely to slow somewhat, and the macro environment is rather tricky but despite the hefty director sale, I think a forward PE of 7 and yield of 4% seems OK and I continue to hold.

On the 25th September the group announced that director Vanda Murray purchased 3,500 shares at a value of just under £20K.

On the 9th November the group released a trading update covering the first eighteen weeks of the year where trading was in line with expectations. The sales market was buoyant in Q1 but ongoing political and economic uncertainty has resulted in a slight slow down in sales in recent weeks in comparison with a strong sales market last year. Despite recent slower market conditions, net private reservations were 2% above last year but the sales rate per outlet was marginally down. The average selling price increased from £352K to £371K. The total order book remains strong and is currently 3% higher than last year at £1.2BN.

Net debt is currently £25M and despite a number of major land purchases is expected to be below £100M by the end of the year.