Ashley House has now released its interim results for the year ending 2018.

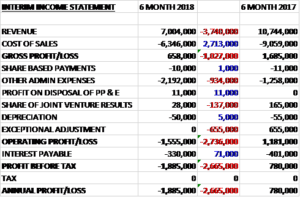

When compared to the first half of last year, revenues declined by £3.7M and with cost of sales only falling by £2.7M the gross profit fell by £1M. There was a £934K growth in admin expenses and joint venture profits fell by £137K. There was also no exceptional adjustment which brought in £655K last time. After interest payments declined by £71k the loss for the period was £1.9M, a deterioration of £2.7M year on year.

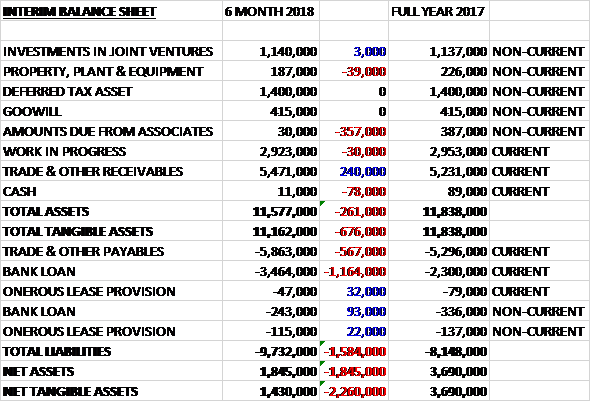

When compared to the end point of last year, total assets declined by £261K driven by a £357K fall in amounts due from associates and a £78K decrease in cash, partially offset by a £240K growth in receivables. Total liabilities increased during the period due to a £1.2M growth in the bank loan and a £567K increase in payables. The end result was a net tangible asset level of £1.4M, a decline of £2.3M over the past six months.

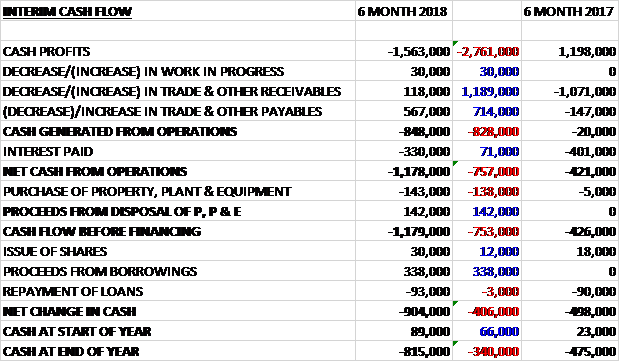

Before movements in working capital, cash profits declined by £2.8M to become a cash loss of £1.6M. There was a cash inflow from working capital and after interest payments reduced by £71K, the net cash outflow from operations was £1.2M, an increase of £757K year on year. The group spent a net £1K on capex to give a cash outflow of £1.2M before financing and after a net £245K was taken out in new loans the cash outflow was £904K and the cash level at the period-end was -£815K.

During the period no schemes reached financial close. This was principally due to the Government’s policy relating to the LHA cap. In October the government announced that it was dropping its plans announced in 2015 to cap housing benefit to LHA rates, enabling the business now to proceed with the delivery of its housing pipeline.

In December the group announced that it had signed a joint venture with Morgan Sindall, established as a 50:50 limited liability partnership which will trade under the name Morgan Ashley. The business will be able to push forward with delivering the housing pipeline that the group has built up over the last few years and is now working to growth the pipeline using relationships developed by both companies. In the last month the group has won a bid for a 54 apartment extra care scheme in Hampshire which will be delivered by the joint venture. The group has received £2.5M of consideration from the transaction and expects to receive the remaining £1.5M deferred consideration in the next few weeks.

In November the group advised that it had two housing schemes that would reach financial close over the coming weeks so these schemes were excluded from the joint venture. The first of these, in Scarborough should reach financial close this week and work continues on a smaller scheme in Peterborough which is being built in the factory via F1 Modular.

F1 Modular continues to build its pipeline. It has recently delivered a six house scheme for Cherwell District Council and an eight bungalow development on former council garage sites for a specialist developer in the North East. The prospective order book for the modular business is growing with two large schemes, one an extra care facility and the other a hotel, both well advanced. While it is still early days, on the assumption that this business is able to deliver these two key schemes, the board believes that it has a strong future.

The pipeline now holds 20 in the joint venture at a value of £203.3M; two housing schemes outside the joint venture with a value of £13.1M; two health schemes with a value of £5.4M with a further two on-site; and three F1 Modular schemes with a value of £13.1M.

In the last couple of months the removal of the threat of the LHA cap along with the establishment of the joint venture with Morgan Sindall were key events for the future of the group enabling it to press forward in the growth and delivery of its significant housing pipeline as well as the other activity in the business. Since the announcement the pipeline has now started to be unlocked but some residual risk remains on rent levels. The board remains confident that they will achieve its profits expectations for the full year but risk remains on the timing of closing of the schemes due to the inherent difficulties of dealing with public bodies.

At the current share price the shares are trading on a PE ratio of 88.2 which falls to 3.3 on the full year consensus forecast. There are no dividends on offer here. At the period-end the group had a net debt position of £3.5M compared with £2.4M last year.

Overall then this has clearly been a difficult period for the group. Losses widened, net assets declined and the operating cash outflow deteriorated. This was because there were no schemes reaching financial closure. The block seems to have been lifted now, though, with the removal of the LHA cap and the setting up of the joint venture. The forward PE of 3.3 looks too cheap and I’m not sure I can rely on it but these shares are finally starting to look interesting.

On the 9th May the group released a trading update covering the year ended 2018. They have achieved financial close on three further schemes. In Ashley House, contracts have been signed with the care provider HSN Care in Peterborough. This will provide specialist residential accommodation for twelve disabled young adults. The modular component of the development will be built by F1 Modular with the work already underway in the factory.

In Morgan Ashley, the scheme in Ryde has reached financial close. This comprises 75 extra care apartments with communal areas providing accommodation for older local residents with care needs, together with 27 affordable bungalows. The scheme will be operated by Southern Housing and owned and financed by Funding Affordable Homes. The scheme is part funded by a grant from Homes England. The business continues to push forward on further schemes and expects a care home in Yorkshire to be the next scheme to reach financial close in the coming weeks.

F1 Modular made a loss in its full year of ownership but it has recently signed contracts for the delivery of a 40 apartment extra care facility in Aberdare for the Housing Association Linc Cymru. This contract will provide activity in the factory for more than six months. The business is also currently delivering classrooms under the Education and Skills Funding Agency framework along with other smaller projects including work for retailers. The pipeline has increased significantly with work being undertaken on a growing number of upcoming schemes including a 148 bedroom hotel. This provides the board with confidence of a positive performance in 2019.

Overall the board expect pre-tax profit in 2018 to be in line with market expectations. The profit will include the write back of an impairment previously recognised against the carrying value of a loan receivable from an associated company. The performance of that business has improved in recent months, enabling it to start repayments more quickly than previously expected. It is thought that this will be fully repaid during the coming year.

The group had net debt of £1.5M at the year-end compared to £3.6M at the end of last year as related party loans have been repaid and the consideration from Morgan Sindall for the joint venture has been received.

This all seems rather positive and I am tempted to take a small nibble here.