Somero has now released their final results for the year ended 2017.

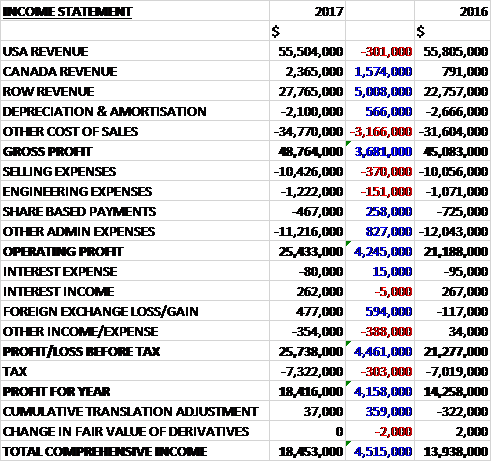

Revenues increased when compared to last year as a $301K decline in US revenue was more than offset by a $1.6M increase in Canadian revenue and a $5M growth in ROW revenue. Depreciation was down $566K but other cost of sales increased by $3.2M to give a gross profit $3.7M higher. Selling expenses increased by $370K and engineering expenses were up $151K but share based payments fell by $258K and other admin expenses were down $827K to which meant that the operating profit increased by $4.2M. There was a $594K positive swing to a forex gain but other expenses grew by $388K and tax charges were up $303K to give a profit for the year of $18.4M, a growth of $4.2M year on year.

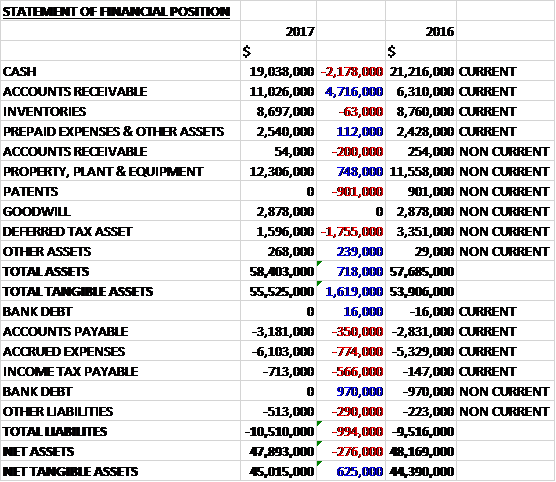

When compared to the end point of last year, total assets increased by $718K, driven by a $4.7M growth in accounts receivable, partially offset by a $2.2M decline in cash, a $1.8M decrease in the deferred tax asset and a $901K fall in the value of patents. Total liabilities also increased during the year as a $986K decrease in bank debt was more than offset by a $774K growth in accrued expenses, a $566K increase in income tax payable and a $350K growth in accounts payable. The end result was a net tangible asset level of $45M, a growth of $625K year on year.

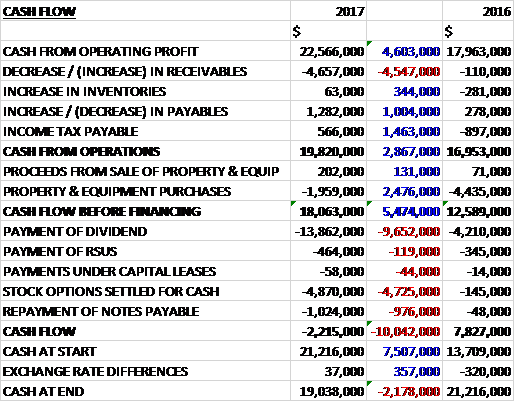

Before movements in working capital, cash profits increased by $4.6M to $22.6M. There was a cash outflow from working capital but also a $1.5M swing to a tax receipt to give a cash from operations of $19.8M, a growth of $2.9M year on year. The group spent a net $1.7M on capex which meant the free cash flow was $18.1M. Of this, $13.9M went on dividends, $4.9M went on stock options settled in cash and $1M was spent on paying back notes so there was a cash outflow of $2.2M for the year and a cash level of $19M at the year-end.

Sales in North America grew 2% with strong second half trading reflecting the strength in the underlying commercial construction industry and the strong pipeline of projects that remain for their US customer base. The high volume of commercial construction activity combined with a growing shortage of skilled labour added to the demand for the group’s equipment and the labour savings it provides.

In Europe sales grew 53% with well balanced demand across the region and particularly strong trading in the UK, Italy, Poland, Spain and the Czech Rep. Sales across their entire product range were also balanced with notable growth in the Boomed Screed and Ride-on screed product lines.

In China sales declined by 14% but second half trading improved year on year due to the positive impact from marketing initiatives. The market fundamentals in the commercial construction industry in the country remain positive and the group intends to continue its training and educational efforts to advance demand for high quality floors.

In Latin America, sales increased 35% driven by strong project activity in Mexico in the first half with good contributions from Chile and Panama throughout the year.

Sales in the Middle East were down 28%. Activity levels in the region were strong throughout the year despite several opportunities slipping into 2018. The countries with meaningful contributions were Turkey, the UAE and Saudi Arabia.

In the ROW region sales increased by 50% with the most significant contributors to growth being India, Scandinavia and Korea. For India, the positive results were driven by the addition of in-country sales leadership.

Previously the group announced that they had agreed plans to build a $1.3M expansion to their Fort Myers HQ with a target to complete in H1 2018 to accommodate planned future growth of the business. Following the high level of activity and potential site development requirements, they are reviewing the plans to ensure this expansion covers all of the anticipated business needs. With the significant growth experienced in Europe, the group is moving into a larger, leased facility in Chesterfield near the current leased site. The group expects the move will be completed by early Q2 2018, and the larger facility will better accommodate the added personnel and increased sales volume in the European region. They do not expect to incur material capex from the move or incur meaningful increase operating costs from the new facility.

From the start of 2018 the US Corporate tax rate was reduced from 35% to 21%. As a result of the change in the law the group expects its future earnings will be positively impacted. This has led to a revaluation of the net deferred tax asset that resulted in a one-off tax charge of $600K. In addition, the act includes a provision that will result in a one-off deemed repatriation tax on the group’s unrepatriated foreign profits primarily relating to historical profits earned by the UK entity. The group will have the option to pay the repatriation tax over an eight year period. They are still assessing the final amount of the tax but it expected to not exceed $800K and will be more than offset by tax savings from the lower tax rate.

Going forward, the high level of activity in North America during the latter part of 2017 has continued in 2018. The board continue to see strong interest in their equipment and remain encouraged by the positive non-residential construction outlook in the US for 2018. The expected positive impact from US corporate tax reform is an additional factor reinforcing their confidence in North American growth prospects.

In Europe, the strong performance is also expected to carry forward into 2018. Similar to conditions in the North American market, European interest in the group’s equipment remains strong driven by demand for replacement equipment, technology upgrades and new products. In China, healthy interest in the group’s products continues and the board expect to see further improvement in 2018 driven in part by the marketing and demand generation initiatives that gained traction in the second half of the year. Although it has taken longer than expected to gain significant foothold in the region the board see a sizeable opportunity in the market segment and plan to continue their market development efforts. In addition they will continue to grow their customer base by offering competitive entry level machines that target the productivity-oriented market and provide future upsell opportunities.

In Latin America, they expect solid performance from Mexico and growth opportunities from the other countries in the region. In their other regions, including the Middle East and their ROW territories, they expect to see significant opportunities in 2018 and beyond and are encouraged by the positive economic climate across this broad territory.

The board believe the company has many meaningful growth opportunities in 2018 across its broad portfolio of markets and products and is confident that the group is poised to deliver another year of profitable growth in 2018.

At the current share price the shares are trading on a PE ratio of 17.1 which falls to 14.8 on next year’s consensus forecast. After a 40% increase in the dividend the shares are yielding 3.4% which increases to 4.3% on next year’s forecast. At the year-end the group had a net cash position of $19M compared to $20.2M at the end of last year.

Overall then this has been another strong year for the group. Profits increased, net assets grew and the operating cash flow increased with plenty of free cash being generated. The North American market strengthened in the second half of the year, which continued into the next year. Europe was very strong, as was Latin America but the smaller markets of China and the Middle East struggled. With a forward PE of 14.8 and yield of 4.3% these shares aren’t quite the bargain they once were but I am happy to continue to hold.

On the 11th June the group released a trading update. North America and Europe remain healthy markets with robust activity levels and the board remain encouraged by the performance in China. They were also encouraged by solid activity levels in the Middle East, Latin America and the ROW territories. They have seen balanced contributions from each product category as sales of boomed screeds, ride on screeds and parts and accessories have all been key contributors to growth. They have made progress in developing a solution for concrete levelling in the structural high-rise market segment.

The constructive environment combined with solid margin performance and healthy operating cash flow generation means the group’s trading to date is ahead of the same period last year and in line with market expectations.