Easyjet has now released their final results for the year ended 2017.

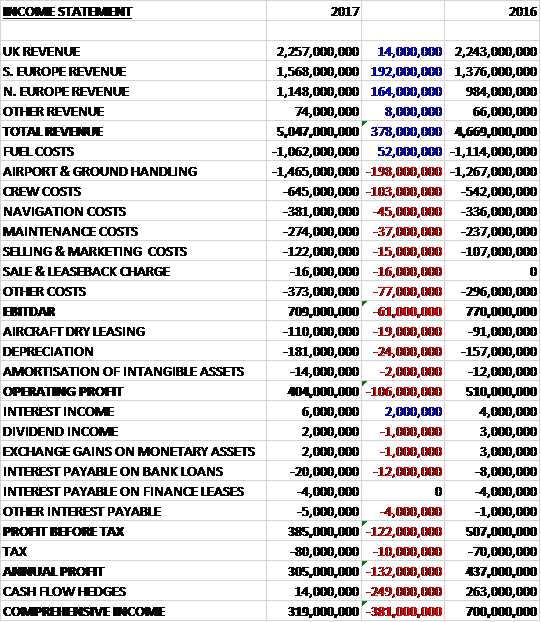

Revenues increased by £378M when compared to last year due to a £192M growth in Southern European revenue and a £164M increase in Northern European revenue. Fuel costs declined by £52M but airport and ground handling was up £198M, crew costs increased by £103M, navigation costs were up £45M, maintenance costs grew by £37M, selling and marketing costs increased by £15M, there were sale and leaseback charges of £16M and other costs increased by £77M to give an EBITDA £61M lower than 2016. Aircraft dry leasing was up £19M, depreciation increased by £24M and amortisation grew by £2M which meant that the operating profit was £106M lower. We also see an increase in bank interest and tax charges up £10M to give a profit for the year of £305M, a decline of £132M year on year.

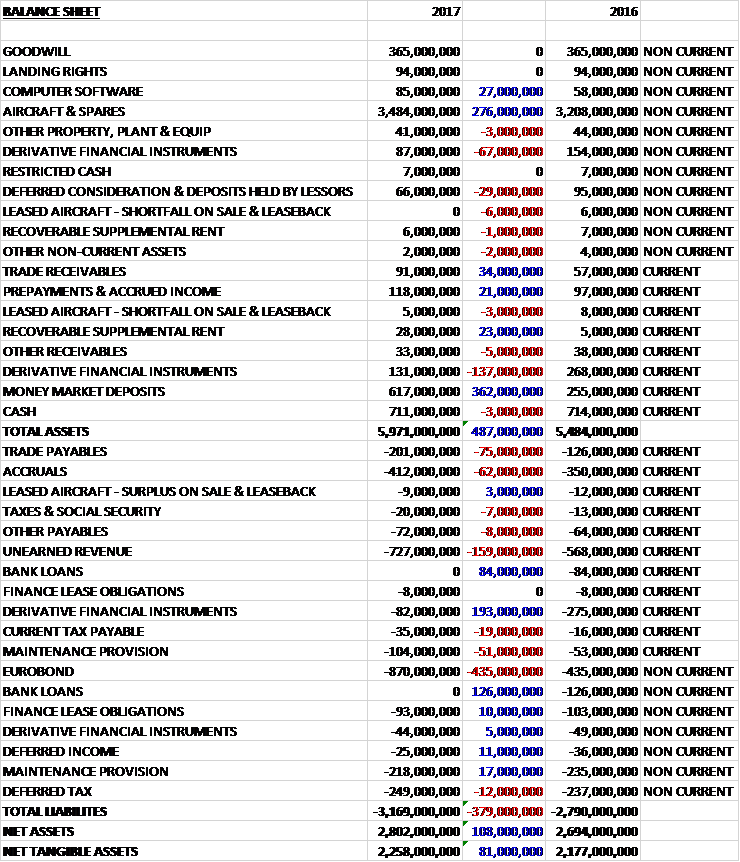

When compared to the end point of last year, total assets increased by £287M, driven by a £362M increase in money market deposits, a £276M growth in aircraft and spares and a £34M increase in trade receivables, partially offset by a £204M decline in derivative financial instruments. Total liabilities also grew during the year as a £198M reduction in derivative financial liabilities, and a £210M fall in bank loans was more than offset by a £435M increase in Eurobonds, a £159M growth in unearned revenue and a £75M increase in trade payables. The end result was a net tangible asset level of £2.258BN, a growth of £81M year on year.

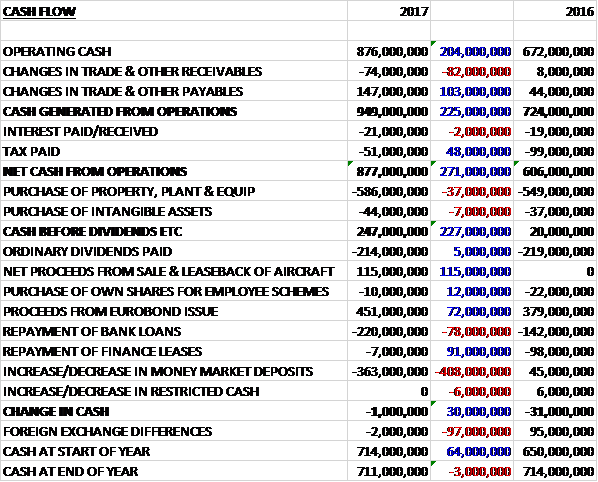

Before movements in working capital, cash profits increased by £204M to £876M. There was a cash inflow from working capital and tax payments declined by £48M to give a net cash from operations of £877M, a growth of £271M year on year. Of this, £586M was spent on property, plant and equipment and £44M on intangible assets so the free cash flow was £247M. The group spent £214M on dividends and shifted some money around with the £451M proceeds of the Eurobond issue and £115M from the sale and leaseback of aircraft used to pay back £363M of money market deposits and £220M of bank loans which gave a cash outflow of £1M for the year. The cash level at the end of the year stood at £711M.

Overall pre-tax profit declined by £86M due to unfavourable forex movements. At constant currency, profits would have increased by £15M. Seats flown grew by 8.5% but total revenue per seat fell by 0.4% to £58.23, or by 4.5 at constant currency. Headline profit per seat decreased by 23.8% to £4.71. The average load factor increased by one percentage point to 92.6%

Revenue per seat was down 4.5% but was broadly flat at constant currency driven by high levels of market capacity growth due to the low fuel price environment, and an aggressive pricing environment that saw new ticket revenue per seat fall by 7.8% at constant currency, offset by ancillary revenue growth of 17.8% as high load factors and consumer-focused initiatives helped to offset pricing pricing pressures. Non-seat revenue increased by 9.3% supported by strong inflight sales of the enhanced product offering.

Within ancillary revenue the group has seen excellent early results from new initiatives in their baggage strategy as well as continued strong pick-up in allocated seating. In September they launched their WorldWide platform, leveraging their network and schedule in Europe’s main airports, offering connections with long haul partners as well as a channel for third party partner sales. The group also has opportunities to build on their partnerships with Europcar and Booking.com and is exploring other value channels with a number of projects in the pipeline over the next year.

In May they launched their hands free bag proposition which has sold over 420,000 bags. further products such as pre-order meals, entertainment and car parking will be integrated over the course of 2018.

Headline cost per seat increased by 2.4% to £53.52 driven by an adverse headline forex impact of £3.56 per seat and the costs of disruption, which remains a major industry challenge. At constant currency, the headline cost per seat decreased by 4.4% as the group continued to benefit from its hedged fuel position. Fuel costs reduced by 19.2% per seat, lean initiatives also helped reduce costs along with the up-gauging off the fleet with the delivery of an additional 21 A320 and two A320neo aircraft.

This helped offset a continued increase in the combined impact on cost from disruption of EU261 claims and an increasingly congested European aviation infrastructure; investments in resiliance including an additional light aircraft in Milan Malpensa, additional spare parts distributed across the network and three wet leased aircraft to add flexibility to the schedule; and inflationary cost increases such as agreed crew deals and start-up costs relating to the introduction of a new ground handling company, DHL, at Gatwick. The group remains on track to deliver flat headline cost per seat excluding fuel at constant currency from 2015 to 2019, excluding Air Berlin.

During the year the group took the decision to close its base in Hamburg in March 2018 with greater returns available by redeploying those aircraft elsewhere. They have grown market share in the UK, Switzerland and Italy. Growth in market share was more robust in France and the opening of a new base in Bordeaux will create the sixth base in the country.

In the UK the group increased its capacity by 8% with significant growth targeted at maintaining their share of the London market through Luton and Gatwick, and increasing capacity at Edinburgh, Bristol and Manchester. In France they increased their capacity by 11%, significantly ahead of the overall market, to consolidate their presence in Paris and increase their share in the regions.

The group increased capacity in Italy by 7%, further increasing investment in Venice, Naples and consolidating their position in Milan Malpensa. In Switzerland they increased capacity by 11%, increasing share inn both Geneva and Basel against overall market growth of 8%. In Germany, the group has decided to close one of its two bases in Hamburg, to focus on Berlin where they invested in maintaining their strong market position. The transaction with Air Berlin will secure a leading position in the city.

In the Netherlands the group increased capacity by 8% as they began to annualise the high growth from the previous two years, focusing on adding frequencies to existing destinations and capturing first wave demand from business passengers. They increased their capacity in Portugal by 14% as they continued to establish their position in both Lisbon and Porto. In Spain, in March they opened their first seasonal base in Palma Mallorca which has been a major success which has the potential to be replicated elsewhere. Overall they increased their capacity in Spain by 13% as they continued to build their presence at both Palma and Barcelona.

During the year, cancellations and delays decreased by 4% but on time performance decreased by one percentage point to 76%. The challenges of working at Gatwick, where the group outperforms most of their competitors, continue to have an impact on the rest of the network. The group was affected by severe weather at peak times of the year, strikes around the network including French ATC, Italian and Berlin ground handling; reduced capacity as French ATC performed systems upgrades in Bordeaux; and capacity limitation events at Gatwick such as disruption caused by a burst tyre on an Air Canada flight in July.

The group are undertaking a number of initiatives to attempt to improve their on-time performance. They have set up a second light aircraft at Milan to ensure engineers can fix aircraft more quickly, saving £6M in the summer and spare parts have been distributed around the network more quickly; they have consolidated Gatwick into the North terminal; they have improved customer communications and introduced further automation to the compensation claims process; they have introduced breaks to their schedule and increased block times to ensure the delivery of a more robust schedule, with three additional aircraft being wet leased as cover; and have employed new technology.

Following the upgrades at North Terminal at Gatwick, queue times at manual bag drops have declined with 90% of customers waiting less than five minutes. The terminal now processes 600 passengers per lane per hour compared to 170 last year which has seen customer satisfaction increase. The Autobag drop has now been rolled out to six further airports. Looking ahead the next phase will focus on the boarding process, using facial recognition technology to reduce queueing time and improve the efficiency of turn arounds. Trials of these new innovations will start in Gatwick and Luton in 2018.

There were a number of non-headline items in the year. There was a sale and leaseback charge of £16M relating to the sale and leaseback of the group’s ten oldest A319 aircraft. There was a £10M loss on disposal and a £6M maintenance provision catch-up upon entering the lease. The implementation of an organisational review has resulted in costs of £6M which involves redundancy costs and associated third party adviser fees. It is expected that a further £3M will be incurred in 2018 in the final phase. These changes are expected to realise annual savings of £15M.

Following the Brexit vote, the group is in the process of setting up a European AOC based in Austria. This helps secure flying rights for parts of the network which remain wholly between EU member states. This year the cost was £2M relating to set up costs. Following the award of their AOC and operating license in Austria the European airline will be operating with more than ten aircraft by the end of 2017 and is in the process of registering more aircraft over the next year. A resolution will be proposed at the AGM to update the group’s Articles of Association relating to shareholder ownership controls to ensure compliance with EU ownership requirements.

The group is contractually committed to the acquisition of 143 Airbus A320 family aircraft with a total list price of $14BN for delivery up to 2022. Capital expenditure is predicted to nearly double inn 2018 to £1.2BN with the spend predicted to be £900M in 2019 and £1BN on 2020. In the first half of next year, 82% of the fuel requirement is hedged at $512 per tonne with 75% hedged at $514 per tonne for the full year and 45% hedged at $533 per tonne in 2019. During this year the average market jet fuel price increased from $415 per tonne to $501 per tonne.

After the year-end the group signed an agreement with Air Berlin’s administrators, as part of which they will enter into leases for up to 25 A320 aircraft at Berlin Tegel, offer employment to former Air Berlin flying crews and take over other assets including slots for a purchase consideration of €40M with completion expected to close in December 2017. Based on current assumptions, the group expects to incur headline losses of around £60M on their activities at Tegel in 2018 using wet lease aircraft with initially lower loads and yields. In addition, one-off costs associated with the transaction are expected to be around £100M in 2018 representing the parallel ramp up of a dry lease operation, including fleet conversion and staff recruitment and training costs as well as transaction costs. The acquisition is expected to be earnings accretive by 2019.

They also completed the sale and leaseback of ten A319 aircraft in the year. Cash proceeds were $137M but due to the age of the aircraft and the maintenance provision accounting policies, a one-off charge of £20M was recognised in the year. The next tranche of ten has now also completed which will result in another non-headline charge of £20M in 2018.

Going forward the group plans to grow capacity by around 6% next year, excluding Air Berlin. Forward bookings are ahead of last year at 88% for Q1 and 26% for Q2. Revenue trends in Q1 have been encouraging, primarily as a result of some capacity leaving the market. Revenue per seat growth at constant currency in Q1 is now expected to be positive by low to mid-single digits and reflects a degree of short term benefit as well as an underling improvement. Revenue per seat in H1 is also expected to be positive by low to mid-single digits reflecting the move of Easter from Q3 but visibility for the second half is very limited.

Total headline cost per seat is expected to decrease by around 2% next year, excluding the impact of Air Berlin costs. Headline cost per seat excluding fuel and at constant currency is expected to increase by up to 1% due to underling crew and ground handling cost inflation. The total expected forex impact for next year is expected to be a headwind of around £5M but headline profit is expected to grow in the year.

At the current share price the shares are trading on a PE ratio of 20.6 which falls to 12.6 on next year’s consensus forecast. After a 24% decrease in the total dividend, the shares are yielding 2.6% which rises to 3.1% on next year’s forecast. At the year-end the group had a net cash position of £357M compared to £213M at the end of last year. After adjusting for the impact of operating leases adjusted net debt decreased by £11M to £413M.

On the 16th October the group submitted an expression of interest in certain assets of a restructured Alitalia.

On the 10th November the group announced the appointment of Johan Lundgren as CEO. He has spent the last year with TUI where he was group deputy CEO.

On the 15th December the group announced that it has acquired part of Air Berlin’s operations at Berlin Tegel airport. The acquisition will result in the group operating 25 aircraft from the airport and includes them leasing former Air Berlin aircraft, taking over other assets including slots and offering employment to former Air Berlin flying crew.

On the 23rd January the group released a trading update covering Q1. They delivered a strong start to the year with a significant growth in revenue in part driven by an increase in passengers flown and strong growth in inflight and ancillary sales. They have generated £28M in savings in the quarter and completed their acquisition of part of Air Berlin’s operations in Berlin.

Total revenue grew by 14.4% reflecting an increase of 1.4 million passengers, a 6.6% increase in revenue per seat, a strong increase in ancillary revenue and a benefit from forex movements. The increase in passengers was driven by a 5.5% increase in capacity and a 2.1 percentage point growth in load factors. Aiding these results has been recent capacity reductions brought about by the bankruptcies of Monarch, Air Berlin and Alitalia as well as the impact from Ryanair’s flight cancellations.

Ancillary revenue performed well. The momentum from last year’s product and pricing initiatives, particularly for bags and allocated seating, is continuing into this year and it is benefiting from both higher loads and further product offerings brought to the market.

Headline cost per seat, including fuel, improved by 1.6% due to low fuel prices and an ongoing focus on cost control. Excluding duel, cost per seat at constant currency increased by 1% as underlying unit cost improvements were offset by underlying inflation and the impact of disruption, mainly due to severe weather and industrial action. The group experienced 1,051 cancellations compared to 512 in Q1 last year with the biggest number due to adverse weather conditions in December.

The group completed the acquisition of part of Air Berlin’s operations at Berlin Tegel airport in December and started its flying programme in January, operating a reduced winter schedule with a fleet of mainly wet lease aircraft. The group currently expects the headline loss from the 2018 flying operation to be around £60M. The transition process for the main part of the operations is also progressing well. Leases on Air Berlin aircraft have been secured and the registration and conversion process has begun. The first ex-Air Berlin crew has now completed training and there is a strong recruitment pipeline over the next few months. The expected non-headline financial cost is expected to be around £100M.

Other non-headline costs included a charge of £19M relating to the sale and leaseback of ten A319 aircraft, costs of £1M associated with the group’s Brexit plans, and £1M of reorganisation costs.

Going forward the group’s seat capacity excluding Tegel is planned to grow in H1 by around 5%. Revenue per seat in Q2 is expected to increase by mid to high single digits which reflects a good underlying revenue performance, lower market capacity growth and the timing of Easter, which will have a negative impact in Q3. Headline cost per seat excluding fuel at constant currency is expected to increase by around 1% for the full year.

It is estimated that at current exchange and with jet fuel remaining within a $620 to $680 per tonne range, the group’s fuel bill in the first half is likely to decrease by between £60M and £65M and exchange rate impacts are expected to have around a £5M positive impact for the full year.

Overall last year was a pretty mixed one for the group. Profits declined, mostly due to unfavourable forex movements, but also due to intense competition driving down the revenue per seat. Net assets grew, however, as did the operating cash flow, with plenty of free cash being generated. The current year has started strongly, with a reversal of the forex pressures and several competitors entering administration. With a continued benign fuel price environment and a forward PE of 12.6 and yield of 3.1% these look decent value to me.