Gem Diamonds have now released their final results for the year ended 2017.

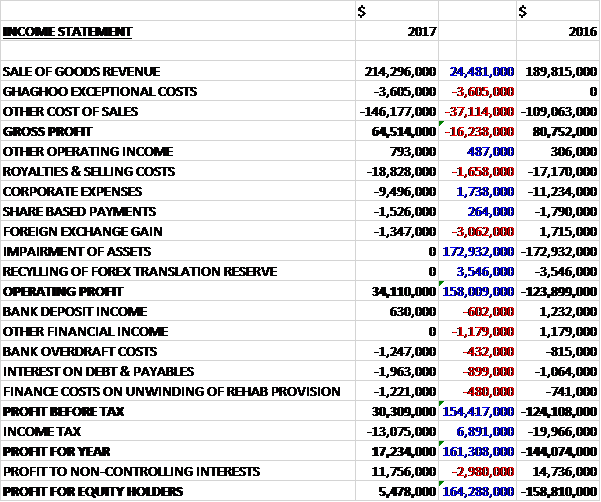

Revenues increased by $24.5M when compared to last year but underling cost of sales grew by $37.1M, mainly due to the strengthening local currency, increased waste amortisation and the fact that costs at Ghaghoo are now being expensed rather than capitalised, and there were $3.6M of exceptional Ghaghoo costs which meant that the gross profit was $16.2M lower. Royalty and selling costs increased by $1.7M and there was a $3.1M swing to a forex loss but corporate expenses were down $1.7M, there was no impairment, which accounted for $172.9M last year and no recycling of the forex translation reserve, which cost $3.5M in 2016. This meant that there was a positive swing of $158M to an operating profit. There was a $602K reduction in bank deposit income, a $1.2M fall in other financial income, a $432K increase in bank overdraft costs, an $899K increase in debt payables and a $480K growth in the finance costs on the unwinding of the rehab provision. Tax charges reduced by $6.9M which meant that the profit for the year was $5.5M, a positive movement of $164.3M year on year.

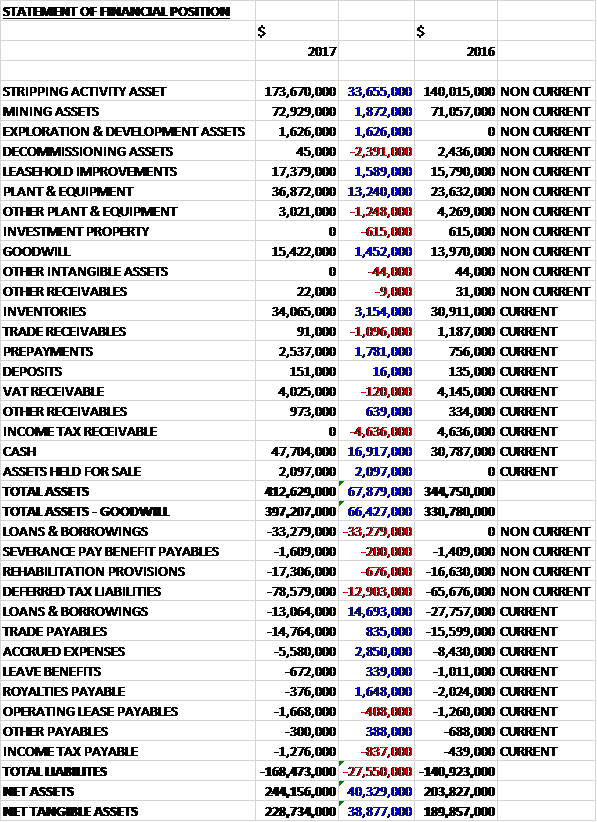

When compared to the end point of last year, total assets increased by $67.9M, driven by a $33.7M growth in the stripping activity asset, a $16.9M increase in cash, a $13.2M growth in plant and equipment, and a $3.2M increase in inventories, partially offset by a $4.6M decline in income taxes receivable. Total liabilities also increased during the year due to an $18.6M increase in borrowings and a $12.9M growth in deferred tax liabilities. The end result was a net tangible asset level of $228.7M, a growth of $38.9M year on year.

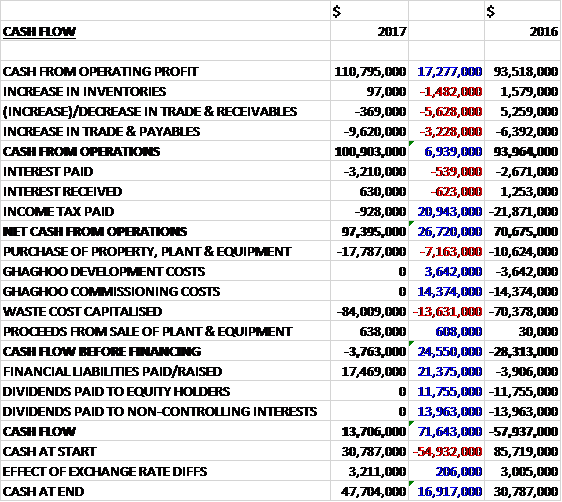

Before movements in working capital, cash profits increased by $17.3M to $110.8M. There was a cash outflow from working capital, mainly due to a decrease in payables, so the cash from operations increased by $6.9M to $100.9M. Interest payments increased somewhat but there was a $20.9M fall in tax payments so the net cash from operations came in at $97.4M, a growth of $26.7M year on year. The group spent $17.8M on property, plant and equipment, along with $84M of waste costs, to give a cash outflow of $3.8M before financing. The group took out $17.5M of new loans to give a cash flow for the year of $13.7M and a cash level of $47.7M at the year-end.

Overall the average value of $1,930 per carat achieved showed a decent increase over last year’s $1,695 per carat. Operating costs per tonne treated were 23% higher. The increase was driven by higher waste amortisation costs as a result of the different waste to ore strip ratios for the Satellite pipe ore. The increase in local currency waste costs per tonne mined of 8% was impacted by local currency inflation and longer haul distances to mine the waste cuts in line with the updated mine plan.

The second half of the year saw the group begin to benefit from the operational improvements implemented during the year with a significant improvement in the recovery of large diamonds from Letseng. The market for the mine’s large diamonds remained strong in the year, which continued into 2018. The focus on enhancing the efficiency of their operations identified a potential of $20M of annualised and one-off cost reductions at the end of last year. A target has now been set of obtaining $100M of cash savings by the end of 2021 with an ongoing target of $30M per year thereafter.

As part of the annual planning cycle, Letseng implemented an updated life of mine plan designed to reduce waste mined over the life of the open pit which resulted in a reduction of waste mined of 5MT and improved cash flows by $9M in the year. The year saw an increase in the amount of Satellite material mined in line with the updated plan. The mine treated 3% less tonnes during the year and the recovered grade of 1.69 was 3.4% higher than last year due to the greater percentage of Satellite pipe ore processed. Carats recovered were broadly flat at 108,513.

Both Letseng plants experienced a reduction in engineering availability in the first half of the year, negatively impacting ore tonnes treated. These were caused mainly by the increased downtime due to unplanned maintenance and maintenance overruns. A review pointed to deficiencies in the system and execution methodology that contributed to the lack of plant and system performance. The maintenance management system and processes have been improved and the availability of the plants improved over the course of the second half of the year. In addition, plant 2’s scrubber shell cracked in H2, necessitating a reduction in the feed rate and the design of a bypass system, which was installed in January and the installation of a new scrubber should take place in Q2.

A mobile XRT sorting machine was installed on a test basis in the second half of the year to re-treat previously generated recovery tailings. During the year, 3,298 carats were recovered from re-treating 25,404 tonnes of these recovery tailings. Based on the results, focus on operating the machine on a 24-7 basis has informed one of the initiatives which will contribute to additional throughput. The re-treatment of the recovery tailings will be concluded in 2018 and the machine will then be used to re-treat tailings generated from the Alluvial Ventures operation.

Letseng recovered seven 100+ carat diamonds during the year, two more than the prior year. The largest was a 202 carat Type IIa diamond recovered in November. There was also a 22% increase in the number of diamonds recovered between 30 and 60 carats but a slight reduction in 60-100 carat diamonds.

The construction of the relocating mining complex, which is required to make way for the expansion of the open pits, was 86% complete by the year-end and is expected to be completed in H1 2018 on time and within budget.

At Ghaghoo, during the year and earthquake occurred 25km from the mine. There was superficial damage to the surface infrastructure and the seal of the underground water fissure was damaged which led to a large influx of water into the underground workings of the mine. Water levels are being effectively managed with continuous pumping. In total $3.6M relating to the one-off costs of placing the mine on care and maintenance and the costs associated with the increased dewatering activities have been reported as exceptional.

The 13,021 carats on hand were sold during Q3, achieving an average price of $175 per carat and discussions are continuing with interested parties to dispose of the mine.

During the year progress was made on two key technologies which are in the process of being evaluated. The first of these is designed to identify locked diamonds within Kimberlite using PET technology. Due diligence work completed in the year has yielded positive results. The second is designed to liberate diamonds outside of the traditional processing technology using a non-mechanical crushing system, which utilises electrical power to fracture the kimberlite without causing damage to the diamond. The workstream is progressing well and during the year a prototype was tested in South Africa with further testing being conducted at high altitude at Letseng.

As part of the business transformation, the investment property in Dubai has been identified as a non-core asset to be sold and it is likely that this will happen within the year and is being held at a value of $615K. The directors also resolved to dispose of the aircraft which serviced the Ghaghoo mine. An offer was received from an interested party in September and a formal agreement was entered into in December. The sale was finalised after the year-end with the proceeds being $1.7M with a cost of sale of $400K.

The improved trend of recoveries of large diamonds continued into 2018 with seven 100+ carat diamonds being discovered including the 910 carat Lesotho Legend which sold for a spectacular price of $40M.

Going forward, the reduction in operating costs and improved recovery of large diamonds together with the impact of the business transformation programme offer the prospect of improved cash flows and give cause for optimism. Demand for large diamonds remains firm and the board are confident that the market for these diamonds will remain resilient for the foreseeable future.

At the current share price the shares are trading on a PE ratio of 35.6 but this falls to 5.8 on next year’s consensus forecast before rising to 14 in 2019. There are no dividends on offer here. At the year-end the group had a net cash position of $1.4M compared to a net debt position of $14.2M at the end of last year.

On the 19th April it was announced that the Lesotho PM announced their intention to renew the Letseng mining licence until 2034 (it had been due to run out in 2024).

On the 26th April the group released a trading update covering Q1 2018. During the period seven diamonds greater than 100 carats were recovered, including a 910 carat D colour Type IIa diamond which was sold in March for $40M ($43,912 per carat). In all, 32,412 carats were sold which achieved an average price of $3,276 compared to $2,217 per carat last quarter. There was an 8% increase in carats recovered.

A new scrubber shell is currently being installed in Plant 2. During this planned shutdown, additional maintenance will be done to the plant in an effort to further improve its availability. This shutdown is not expected to have a material impact on production. The mining services complex project was completed on time and under budget in April.

The business transformation four year target of $100M remains on track. Initiatives which have been implemented to date will contribute around $27M to the four year target and comprise $23M of cumulative recurring benefit and $4M of one-off savings. Of this, $15M will be from increased revenue generated from additional carats recovered from re-treated tailings through the mobile XRT sorting machine and the extension of the third plant operator’s tenure to mid-2020. A cost reduction of $8M Is mainly due to a reduction in blasting consumables through changing blasting patterns, explosive mix and charging practices. Cost reductions have also been achieved through reducing corporate office footprints and travel costs. One-off savings mainly comprise the sale of non-core assets.

At the period-end the group had a net cash position of $28.9M compared to $1.4M at the year-end.

Overall then the group seems to have turned a corner this year. Profits are down, excluding last year’s impairments, due to increased costs from stronger local currencies and increased waste amortisation, but net assets and the operating cash flow improved, although the group is not producing any free cash. The average price per carat is improving due to the higher number of large diamonds being recovered, including a truly huge one in Q1 2018. It seems unlikely that this will be repeated but it does seem that the initiatives the group is undertaking is improving recovery.

They are also bringing down costs and if the disastrous Ghaghoo mine can be sold, that would also help. This does mean that the group will become a one-asset entity which has its own inherent risks but I feel that now might be the time to take a little punt here.

On the 22nd May the group announced the recovery of a 115 carat, top white colour Type iia diamond. This is the ninth diamond of over 100 carats recovered in 2018, already exceeding the total recovered last year.

On the 3rd August the group released a trading update covering the first half of the year. During the period the Lesotho Legegend was sold for $40M which was the largest diamond found at the mine. In all they recovered ten diamonds greater than 100 carats in the period and sold 61,696 carats at an average price of $2,742 per carat, up from $2,061 per carat in the first half of last year. This led to record tender revenues of $169.2M. In July they recovered one more diamond over 100 carats.

The amount of ore treated declined by 8% but due to a 10% increase in the average grade recovered, the number of carats recovered remained broadly flat at 61,596.

A new scrubber shell was installed in plant 2 in Q2. The feed rate into the plant has reverted to normal levels since the shutdown was completed. The installation took longer than planned due to the concrete foundation of the scrubber requiring to be fully rehabilitated. As a consequence, the shutdown was extended by ten days which is the primary reason for the reduced tonnage treated.

At Ghaghoo the water fissure was sealed.