Easy Jet has now released their interim results for the year ending 2018.

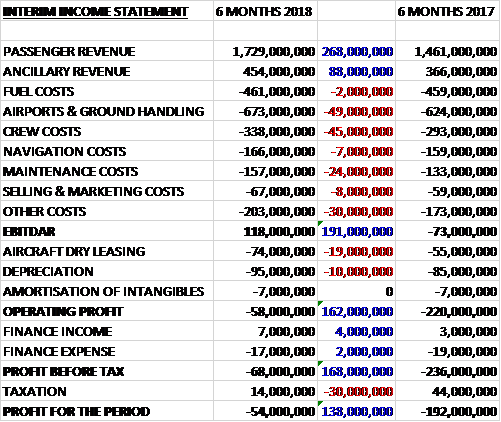

Revenues increased when compared to the first half of last year due to a £268M growth in passenger revenue and an £88M increase in ancillary revenue. Fuel costs were broadly flat but airport and ground handling costs increased by £48M, crew costs were up £45M, maintenance costs increased by £24M and other costs grew by £30M to give an EBITDA £191M ahead of last tome. Dry leasing costs increased by £19M and depreciation was up £10M which meant that the operating profit grew by £162M. There was a modest reduction in finance costs but tax charges were up £30M to give a loss for the period of £54M, a £138M improvement year on year.

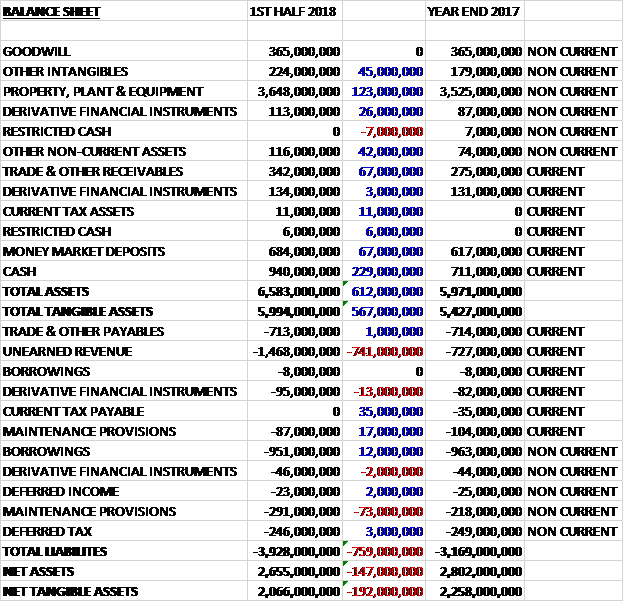

When compared to the end point of last year, total assets increased by £612M driven by a £229M growth in cash, a £123M increase in property, plant and equipment, a £67M growth in money market deposits, a £67M increase in receivables, a £45M increase in intangible assets and a £42M growth in other non-current assets. Total liabilities also increased during the period was a £35M reduction in the current tax payable was more than offset by a £741M increase in unearned revenue and a £56M growth in maintenance provisions. The end result was a net tangible asset level of £2.066BN, a decline of £192M over the past six months.

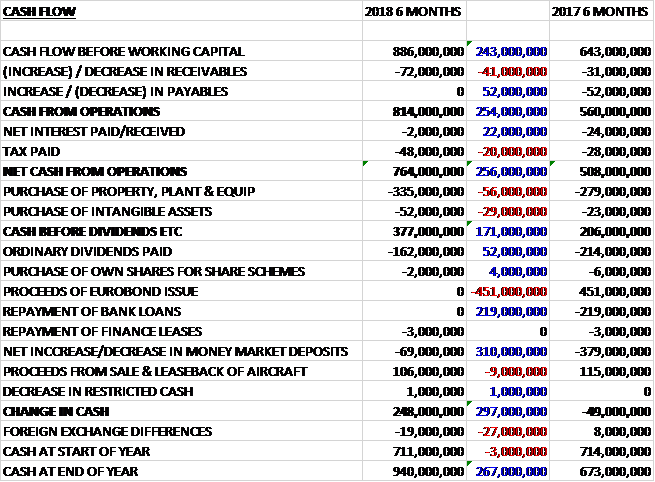

Before movements in working capital cash profits increased by £243M to £886M. There was a cash outflow from working capital but this was slightly less than last time. A £22M reduction in interest payments was mostly offset by a £20M growth in tax payments to give a net cash from operations of £764M, a growth of £256M year on year. The group spent £335M on fixed assets and £52M on intangible assets to give a free cash flow of £377M. Of this, £162M was spent on dividends and £69M was paid into money market deposits. The group received £106M from the sale and leaseback of aircraft which meant the cash flow was £248M and the cash level at the period-end was £940M.

Revenue per seat grew by nearly 11%, reflecting a strong underlying performance and the Air Berlin acquisition. Excluding Tegel operations, revenue per seat grew by 9.5% at constant currency. This was driven by a 4.6% increase in capacity, focused on growth in the French regions, further consolidating positions in core UK airports and continuing to grow in Basel and Venice; an increase of 1.7 percentage points in the load factor; lower market capacity following the bankruptcy at Monarch and Air Berlin and the winter withdrawal of Ryanair from the UK domestic market.

Other drivers of the increase in revenue per seat have been the partial movement of Easter to Q2; a strong performance on ancillary revenue per seat, increasing by 14%, due mainly to an improved bag proposition, smarter bag yield algorithms and further benefits from the Hands Free product.

Total cost per seat was broadly flat as the benefits of the group’s cost focus and lower fuel price offset a negative forex impact. At constant currency, the cost per seat reduced by 1.5%. Excluding fuel and the Tegel operation, constant currency costs increased by 1.3% as lower airport charges, lower navigation charges and the up-gauging of the fleet offset disruption from severe weather, increased crew pay, higher ground charges, the sale and lease back transaction and costs associated with the higher load factor.

During the year the group focused its growth on maintaining market share in the UK and Switzerland and growing in regional France. This included the opening of a new base in Bordeaux, where they are now already the number one airline. They also invested capacity growth in its city strategy: in Venice to consolidate their number one position, and in Amsterdam where the airport is now at full capacity. Further capacity growth was deployed in their lean bases to increase their scale and leverage their cost advantage. In March they closed their Hamburg base and now have 29 across the network.

The group is looking at a number of future opportunities to drive growth. They are focusing on transforming their holiday business, creating a more compelling business passenger proposition and driving loyalty. They expect to invest both capital and operational expenditure with the majority of investment occurring in 2019 with a delivery of increased profit per seat in 2020.

They see a significant opportunity to transform their holidays proposition. Currently only 500,000 passengers book a hotel with them out of an addressable market of 20M so they see an opportunity to add significant value by forming a dedicated business unit offering a clear and attractive proposition. Improving the business offering will mostly focus on capabilities such as building a new online portal to allow small and medium size businesses to book more easily with them, automating invoicing and more direct contracting with their corporate customers.

During the period the on time performance was up one percentage point to 81%. This was despite the severe weather and regular third party strike activity which led to a 39% increase in cancellations and delays.

In December the group completed the partial acquisition of Air Berlin’s operations at Berlin Tegel and progress to date has been in line with expectations. The group operated a winter schedule with a fleet of mainly wet leased aircraft in order to retain its slot portfolio. As expected, this start up phase has resulted in lower than average load factors (63%) and revenue per seat (£35.97) due to the short lead times to sell flights and a mainly inherited schedule. Higher than normal cost per seat (£48.02) reflects the expensive nature of interim wet leasing arrangements while they introduce their own fleet. This has led to a headline loss of £26M with non-headline costs of £24M.

As usual there were a number of “non-underlying” items. There was sale and leaseback charges of £19M which represents an £11M loss on the disposal of ten old A319 aircraft and an £8M maintenance provision catch up. There was £4M of Brexit-related costs associated with the new AOC in Austria due to the cost of re-registering aircraft. There was a £24M cost relating to the Tegel integration comprising £9M of engineering costs to align the technical specs of ex Air Berlin aircraft with the rest of the fleet, £7M of dry lease rental costs incurred prior to these aircraft becoming operational, and £8M of consultancy and legal fees.

In May the Civil Aviation Authority confirmed that the group had been awarded a new UK Air Operator Certificate. They plan to transfer their UK-based fleet across to the AOC in June and their Luton based group operations will continue to support all three standalone AOCs in Austria and Switzerland as well as the UK.

Going forward, capacity excluding Tegel is planned to grow by around 5% in H2. Ex-Tegel revenue per seat should be slightly higher, reflecting the improving capacity environment and the ongoing strikes at Air France. They expect the Ex-Tegel cost per seat excluding fuel to increase by 2% for the full year reflecting the expected higher employee incentive costs due to the strong operational performance.

At Tegel they now expect to deliver a headline loss of £75M to £95M reflecting a £15M adverse impact from the increase in fuel price, recent security charge increases in Germany, as well as a lower average gauge than planned on some of the wet leased aircraft. In addition this reflects uncertainty regarding summer revenue while the group flies the sub-optimal Air Berlin schedule. This is expected to be offset by a combination of trading benefits from Schonefeld, which benefits from the improved Berlin customer proposition, and savings in the non-headline implementation costs which are now expected to be £60M due to lower than expected lease costs. The board expect the Tegel operations to be earnings enhancing in 2019.

It is estimated with jet fuel remaining between $680 and $740 per tonne, the fuel bill is likely to decrease by around £65M. Exchange rate movements are likely to have a £25M positive impact on profits and the board expect the reported headline pre-tax profit for 2018 including Tegel to be £530M to £580M. The group has hedged 56% of next year’s fuel requirements at $549 per tonne.

At the current share price the shares are trading on a PE ratio of 21 which falls to 10.4 on the full year consensus forecast. The shares are currently yielding 2.5% but this increases to 3.4% on the full year forecast. At the period-end the group had a net debt position of £238M compared to £413M at the prior year-end.

On the 18th July the group released a trading update covering Q3. They had a strong performance with robust customer demand driving outperformance in their revenue growth. Disruption across Europe continues to be an industry wide issue and is having an impact on revenue, cost and operational performance with the main drivers being European industrial action and air traffic restrictions. Despite this increase in disruption the group has increased its headline pre-tax profit guidance for the year to between £550M and £590M.

Total revenue increased by 14% and ancillary revenue was up 21%. Passenger numbers increased by 9.3% driven by an 8.9% increase in capacity and a 0.3 percentage point increase in load factor. Total revenue per seat excluding Tegel increased by 4.8% at constant currency driven by a benign competitor environment with unfilled Monarch capacity and challenges in France; continued positive underlying trading with a strong May due to the timing of public holidays; an increase in ancillary revenue with more customers choosing allocated seating and adding bags; offset by a £40M negative impact of Easter moving partially into the first half of the year. The board now expect H2 revenue per seat to increase by low to mid-single digits.

Operational performance for the quarter has been significantly impacted by external factors, in particular the sustained ATC industrial action in France as well as the impact of severe weather. The group experienced 2,606 cancelled flights in the period compared to 314 in Q3 last year. As a result of the disruption the OPT was 73% compared to 78% last year.

The group’s underlying cost performance has been solid. Headline cost per seat excluding fuel at constant currency increased by 4% reflecting increased disruption costs, the accrual of expected employee incentive payments due to the strong financial performance, and costs relating to increased loads, crew costs and underlying inflation. Mainly as a result of the increased disruption, the group now expects full year cost per seat to increase by 3%.

At Tegel load factors are increasing and are now consistently over 80% and have reached 86% for June. Revenue per seat is weaker than previously guided due to recent additional capacity in the Berlin market and as a result, headline losses are expected to be £125M instead of the £95M previously guided. The group is now targeting a break-even position in 2019.

For the year as a whole, excluding Tegel, the group is expecting capacity to grow by 4.5%, H2 revenue per seat to increase by low to mid-single digits, full year headline cost per seat excluding fuel to increase by 3%, full year unit fuel bill likely to be £65M lower, and forex movements to have a £20M positive impact. The Tegel operations are expected to deliver a headline loss of £125M and a non-headline loss of £50M. Headline profit for the year, including Tegel, is expected to be between £550M and £590M, up from previous guidance of £530M to £580M.

Overall then this has been a good period for the group. Losses (the first half is always loss making) improved, net assets declined (again due to seasonality) and the operating cash flow improved with a decent amount of free cash being generated. The revenue per seat was strong, aided by both capacity increases and load factor improvements and also problems at other airlines such as Monarch. Costs per seat were flat during the period. Things are not all going Easy Jet’s way, however, the Tegel operations are taking longer to turn a profit than expected and there has been a huge amount of disruption due to strikes causing cancellations but with a forward PE of 10.4 and yield of 3.4% I am happy to hold on here. I am tempted to buy more.

On the 28th September the group released a trading update covering the year as a whole. They will deliver a strong performance in Q4 with robust customer demand driving outperformance in both their passenger and ancillary revenue growth, and strong profitability. Disruption across Europe continues to be an issue and is having an impact on revenue, cost and operational performances with the main issues being European industrial action and air traffic restrictions. They have seen an improved performance in Tegel reducing the expected headline loss to around £115K along with further savings in non-headline integration costs to around £45M.

Despite the impact of disruption, the group expects to deliver full year headline pre-tax profit of between £570M and £580M, in the upper half of previous guidance.

Passenger numbers in the full year excluding Tegel are expected to increase by 5.4%, driven by an expected increase in capacity of 4.2% and a 1 percentage point increase in the load factor to 93.6%. Total revenue per seat excluding Tegel at constant currency is expected to increase by 5%, at the higher end of previous guidance and the expected revenue is expected to be nearly £5.9BN.

The headline cost per seat excluding fuel and Tegel at constant currency is expected to have increased by around 3.8%, higher than previously expected due to sustained high levels of disruption. Underlying cost control remains solid and in line with expectations. They experienced an increase in cancellations due to third party industrial action, air traffic control restrictions and severe weather across Europe. The headline cost excluding fuel and Tegel is expected to be around £4.135BN. The total fuel cost for the year including Tegel is expected to be around £1.185BN including an expected additional £15M cost compared to previous guidance as a result of US forex exchange impacts and carbon emission trading costs.

The group is progressing well with implementing its operational delivery and building market presence in Berlin, whilst flying an inherited inefficient schedule that had the biggest impact in the peak summer season. Headline losses for the Tegel operations for the year are expected to be around £115M, an improvement on previous guidance. Load factors remain relatively strong at around 85% in Q4, highlighting positive customer uptake. The group expects a further reduction in non-headline costs for the year to around £45M. The expected total loss for Tegel operations has now improved to be in line with the original guidance of £160M.

Over the past three years the group has been investing in its commercial IT platform which has delivered revenue benefits through significant improvement in the customer facing website and seating capability as well as improvements in underlying resilience and control systems. They have now made the decision to change their approach to technology development, however, through better utilisation and development of existing systems on a modular basis rather than working towards a full replacement of their core commercial platform.

As a result of this change of approach, they are recognising a non-headline charge of around £65M relating to IT investments and associated commitments that they will no longer require. They will continue to invest in their digital and e-commerce layers that will enable them to continue to offer a leading innovative, revenue enhancing and customer friendly platform.

The outlook including Tegel for the year is that capacity will grow by about 10%. Around half of this represents the annualisation of Berlin flying as well as the benefit of fleet up-gauging in the summer. H1 revenue per seat is expected to decrease by low to mid single digits. This reflects a continuation of positive trading offset by a number of one-off revenue benefits from H1 2018 such as the bankruptcies of Monarch and Air Berlin, as well as the impact from Ryanair’s winter flight cancellations. The benefit of Easter will shift from H1 into the second half of the year.

Full year headline cost per seat excluding fuel at constant currency is expected to be flat, which represents an expected decrease in underlying cost per seat offset by inflationary airport and crew pay deals and investment in the business. The full year fuel bill is likely to be £55M to £105M worse than this year. Forex movements are expected to have a £10M net negative impact on profits. The group is targeting a break even in Berlin.

Overall the group expects to deliver a strong performance in both Q4 and the full year, driven by better than expected growth in passenger and ancillary revenues as well as reduced losses at the Tegel operation. They now expect their headline profit for the year to be between £570M and £580M, at the top of their guidance range. It is worth taking into account that they have benefited from a number of one-off events in 2018, however.

On the 31st October the group announced that it had submitted a revised expression of interest for a restructured Alitalia. The submission, which is in response to the new government’s ongoing sales process, is consistent with the group’s existing strategy for Italy.