Wynnstay has now released their interim results for the year ending 2018.

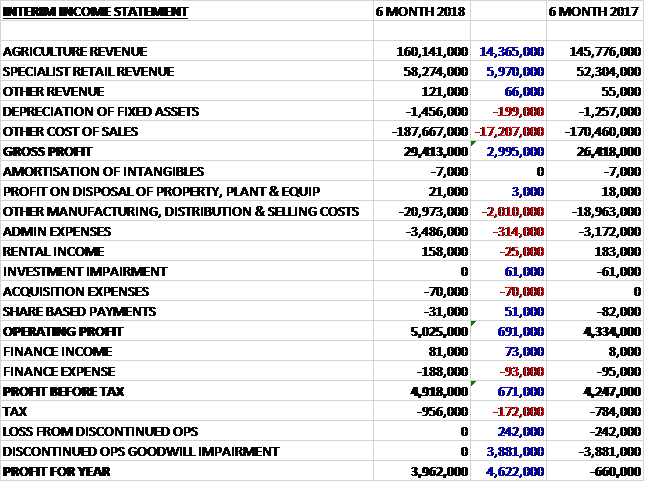

Revenues increased when compared to the first half of last year with a £14.4M growth in agriculture revenue, a £6M increase in specialist retail revenue and a £66K increase in other revenue. Depreciation was up £199K and other cost of sales increased by £17.2M to give a gross profit £3M higher. Manufacturing, distribution and selling costs grew by £2M and admin expenses were up £314K which meant that the operating profit grew by £691K. There was a modest increase in finance expenses and tax charges grew by £172K to give a profit for the period of £4M, a growth of £499K year on year.

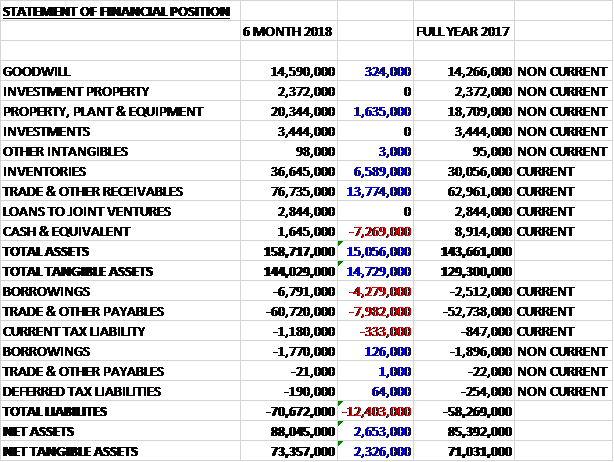

When compared to the end point of last year, total assets increased by £15.1M driven by a £13.8M growth in receivables, a £6.6M increase in inventories and a £1.6M increase in property, plant and equipment partially offset by a £7.3M decrease in cash. Total liabilities also increased due to an £8M increase in payables and a £4.2M growth in borrowings. The end result was a net tangible asset level of £73.4M, a growth of £2.3M over the past six months.

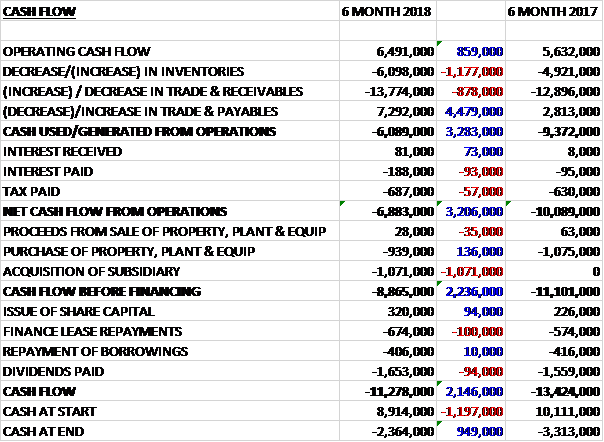

Before movements in working capital, cash profits increased by £859K to £6.5M. There was a cash outflow from working capital but this was less than last time and the net cash outflow from operations was £6.9M, an improvement of £3.2M year on year. The group spent £939K on property, plant and equipment along with £1.1M on acquisitions to give a cash outflow of £8.9M before financing. The group spent £674K on finance lease repayments, £406K on loan repayments and £1.7M in dividends to five a cash outflow of £11.3M and a cash level of -£2.4M at the period-end.

The profit in the Agricultural division was £2.1M, an increase of £513K year on year, helped by increased feed volumes. The trading environment across the sector began to recover during 2017, and stronger output prices for both arable and livestock farmers have driven a broad recovery in demand for agricultural inputs. Demand was strongest in the livestock sector where there was also a higher feed requirement as a result of the extended winter period. While the late spring led to delayed demand for arable inputs, sales were in line with last year. Grain volumes improved in the late spring period, although margins remain under pressure in a relatively flat market.

The feeds business benefited from strong demand for compound, blended and straight feed products, as improved output prices encouraged livestock farmers to return to more typical feeding regimes. Demand for ruminant feeds was also boosted by the long winter period, although some extra costs were incurred in meeting this demand. Bagged feed sales which are principally sold through the store network, reached record highs, also benefiting from the extended winter period. They also saw volume growth in monogastric feeds, with further expansion of feeds for free range egg production.

Glasson grain delivered a solid performance with an increase in volumes in all products, although there was some margin pressure in fertilizer. The Montrose mill acquisition positions the business as the second largest fertilizer blender in the UK. The manufacture of certain products for Youngs animal feeds has boosted the output of specialist corn milling activities and they are starting to see the benefits come through.

The late spring affected demand for arable products in the first half. April and May were very busy months, however, and on a year to date basis, arable product sales are now at normal levels. Demand for spring cereal seed has been very strong, partly reflecting a change in cropping pattern as some arable enterprises deal with blackgrass weed problems associated with autumn cropping. Herbage sales are currently at lower levels than last year, reflecting the general trend in the UK but the group expect an increase in demand later in the year, subject to autumn weather conditions. Inclement weather also reduced usage of agrochemicals and despite a strong demand in May, sales remain behind budget.

Improved grain prices stimulated trading activity and volumes for Grain Link have risen above the previous year. The previously subdued activity and flat market prices, however, have had a negative impact on margins. Forward grain prices remain strong which is an encouraging sign for arable farmers and bodes well for the sector.

The group have started work on a major warehouse expansion project at their arable site near Shrewsbury. This will enable them to increase production of processed seed in 2019 and they will also be enlarging their retail facilities at the same site.

The profit in the Specialist retail division was £3.1M, an increase of £188K when compared to the first half of last year. Sales across the network of Wynnstay stores increased strongly over the first half with like for like sales up 8%. Demand for feed was a key driver of this increase as farmers battled inclement weather, but increased spending was evident more broadly, including supplements and hardware products, reflecting the general improvement in sentiment at farm level.

The acquisition of a further eight stores was part of the expansion plan in the South West where they were underrepresented. The new outlets were previously loss making and will require investment to fully develop. The board anticipate them making a positive earnings contribution in 2019, however. With the addition of these new stores the network now stands at 60 outlets.

In November the group acquired a mill and related processing facilities in Scotland from Origin for £550K, all in deferred consideration, which represents the book value of the mill. Origin was required to dispose of the mill for competition remedy purposes. The mill contributed a profit of £159K in the half year so this looks to be a good acquisition.

In April 2018 the group acquired eight former Countrywide Farmers agricultural retail stores for £681K, which broadly represents the value of the stores. In addition the group completed a number of smaller acquisitions for £529, including deferred consideration of £189K. After the period-end, in May, Glasson Grain acquired Fertlink, a 50% joint venture fertilizer manufacturing facility established between Glasson and NW Trading. The acquisition will increase the fertilizer division’s sales volumes and allow it to better service the market on the East side of the UK. There was no consideration but due to the fact that there were net liabilities, the acquisition generated goodwill of £266K.

Ken Greetham retired in early July, after ten years as CEO. At the same time Gareth Davies, joint MD of Wynnstay Agricultural supplies was appointed as CEO designate.

Going forward, the improvement in output prices for farmers provides a robust backdrop for the UK industry. While Brexit negotiations remain underway, the full implications on some UK farming practices are difficult to predict but it is widely accepted that the existing financial support mechanisms provided as part of the Common Agricultural Policy will focus on output parameters rather than area and historical factors. The group expect an even greater emphasis on efficiency and productivity as farmers compete in a market with changing competitive dynamics.

Current trading is in line with overall budgets and despite short term costs associated with the integration of the newly acquired Country stores, the board believes that the group remain well positioned to meet current market expectations for the full year.

At The current share price the shares are trading on a PE ratio of 13.2 which falls to 11.8 on the full year consensus forecast. After a 5% increase in the interim dividend, the shares are yielding 3.1% which remains the same for the full year. At the period-end the group had a net debt position of £6.9M compared to £8.3M at the same point of last year.

Overall then this has been a good period for the group. Profits were up, net assets increased and the operating cash outflow improved. The outflow was entirely due to seasonal working capital movements and cash profits comfortably covered expenses. Both divisions fared well, benefiting from the improved market, especially for livestock feed. Going forward, conditions in H2 have started well and the forward PE of 11.8 and yield of 3.1% looks decent value. I continue to hold

On the 22nd November the group released a trading update covering the whole year. Trading across both the agriculture and specialist retail divisions has continued strongly with farmer confidence and spending patterns continuing to recover as output prices have strengthened. As a result the board bow expects to report pre-tax profit ahead of current expectations.

Strong feed sales, both direct to farm, and through the retail stores have been a key driver of this performance. Feed volumes and margins benefited from both the improvement in underlying market demand and the extended warm dry summer, which limited forage availability. Fertilizer volumes, which have been expanded through acquisitions within the Glasson business, were also boosted by weather conditions in Q4 and seed sales were also strong over this period. The integration and turnaround of stores acquired from Countrywide Farmers is proceeding to plan and they are expected to make a positive contribution in 2019.

The board believes the general agricultural and commodity outlook in the UK remains positive, and that the group is well placed to take advantage of the opportunities that are expected to present themselves.