Newmark Security have now released their final results for the year ended 2018.

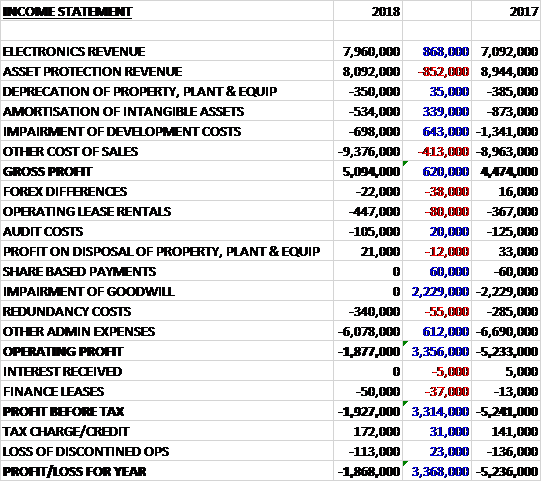

Revenues were broadly flat year on year as an £852K decline in asset protection revenue was offset by an £868K increase in electronics revenue. Amortisation was down £339K, impairment of development costs decreased by £643K but other cost of sales were up £413K to give a gross profit £620K higher. Operating leases increased by £80K but share based payments were down £60K. There was no impairment of goodwill, however, which cost £2.2M last year and but redundancy costs increased by £55K. Other admin expenses fell by £612K to give an operating loss that showed a £3.4M improvement. Finance lease costs increased modestly but tax charges came down to give a loss for the year of £1.9M, an improvement of £3.4M year on year.

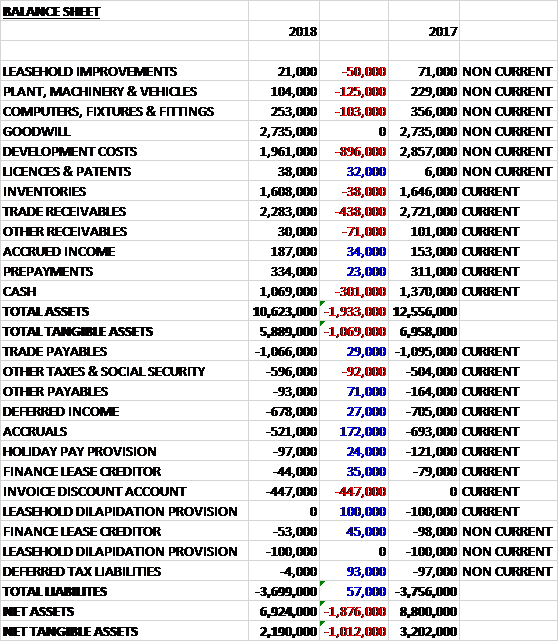

When compared to the end point of last year, total assets declined by £1.9M driven by an £896K decrease in development costs, a £438K decline in trade receivables, a £301K fall in cash, a £125K decrease in plant, machinery and vehicles, and a £103K decline in computers, fixtures and fittings. Total liabilities were broadly flat as a £447K growth in the invoice discount account was offset by a £172K decrease in accruals, a £100K fall in the leasehold dilapidation provision and a few smaller declines. The end result was a net tangible asset level of £2.2M, a decline of £1M year on year.

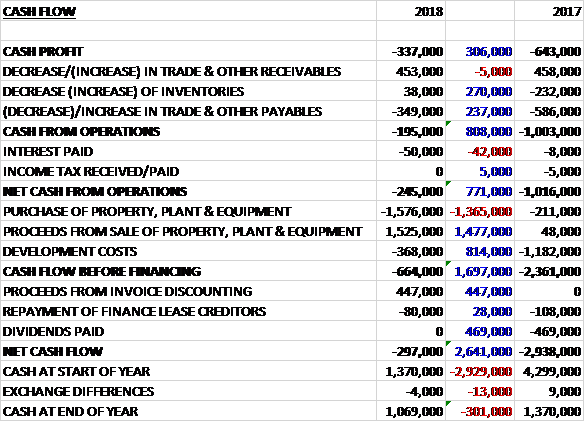

Before movements in working capital, cash losses improved by £306K to £337K. There was a cash inflow from working capital and after interest payments increased by £42K the net cash outflow from operations was £245K, an improvement of £771K year on year. The group spent £1.6M on fixed assets but recouped £1.5M from asset sales and after £368K was spent on development costs there was a cash outflow of £664K before financing. The group received £447K from invoice discounting but paid back £80K of finance leases which gave a cash outflow of £297K and a cash level of £1.1M at the year-end.

Overall revenue in the electronic division increased by 12% as the decline in the legacy Janus range of access control products was offset by the growth in the Sateon range driven by the release of the latest Advance variant in the second half of the previous year. Within this, sales of access control increased by just 1% but sales of workforce management increased by 25% driven by additional sales relating to announcements made regarding supply agreements to strategic partners and organic growth, particularly in the US.

Overall revenue in the asset protection division decreased by 10% with a 17% decrease in product sales mainly due to the lower revenue from time delayed cash handling equipment sales to the Post Office.

The electronic division saw revenues increase by 12.2%. This was a turn around year for the division. The investment made in product development has started to be repaid and this increase in revenue, combined with a reduction in overheads has delivered a significant reduction in Grosvenor’s losses. Several potential high volume supply agreements have been executed in HCM and although these did not play any major part in this year’s results, they are expected to contribute significantly towards the overall revenue ambitions for 2019.

Sateon Advance has continued the encouraging start it displayed since its launch in H2 last year and several more major opportunities for both Sateon Advance as a complete solution and the OEM variants of the Advance Access Control hardware are currently being investigated. Negotiations are currently underway with one of the UK’s largest security systems integrators and several US-based global Access Control providers. The product has delivered a large volume of new systems and displayed patterns of repeat business from customers throughout the UK.

The research into opportunities for aaS revenues in new markets, facilitated through the provision of the GT-10 Android terminal, has shown there is likely to be a higher return on investment in their existing markets by leveraging their core competencies. Both HCM, particularly in the US, and to a lesser degree Access control sectors, demonstrate a trend towards the downstream provision of cloud first and even cloud only services. Therefore, a decision has been taken to focus on their aaS development on existing products, services and sectors rather than diversified markets.

Within Access Control, the decision was made to retire the legacy Janus range with no new systems installed or operating licenses issues and consequently revenue declined by 32% to £1.3M. Market pricing for hardware for site extensions or replacements has been increased to reflect the higher costs of manufacturing and supporting legacy products in lower volumes and, therefore, it is expected that this product family will yield a greater gross margin contribution. Existing Janus systems will now require either an extended support agreement or upgrading to Sateon to ensure continuity of service to end users. The Janus to Sateon upgrade programme continues to help drive revenues for the latter.

Sateon has continued its robust growth trajectory with an increase of 32% to £2.6M. Sateon Advance has proven to be the most successful variant of the product to date and continues to grow in terms of both revenues and number of systems installed. During the year a review was conducted on Sateon to test its future set and technical stability versus market expectations and it was concluded that the product was mature and that all necessary development was complete. A final release including bug fixes was released in the first half of 2019.

Development work has continued to create non-proprietary variance of the Advance hardware range to allow it to be integrated with third party vendor’s software. By adopting an open protocol approach, incremental revenue is being generated as new channels are developed. A major European Workforce Management software provider has selected Advance as an OEM product to integrate with their proprietary access control solution. This partner’s spend increased 80% to £710K in the year. Negotiations are now underway with major global third party access control providers to supply this line as OEM products which would integrate with their various software platforms.

Grosvenor’s collaboration with US-based UniKey Technologies to launch a frictionless door experience was put on hold as their product development and delivery was slower than expected and failed to satisfy the board’s fiscal tests. The market for biometric credentials is dynamic, driven in part by consumer adoption of biometric technologies on smart devices. The business is taking an open protocol stance and is able to integrate any third party point of entry reader or device into either its Access Control or HCM range of products.

Across both the UK and US businesses, revenues from Human Capital Management products and services increased by 25%. In EMEA, HCM providers have a requirement for an Access Control offering as they seek additional revenues through diversification. In the US, however, it is recognised that the HCM sector generally and its sub sections, are large enough for software vendors operating in those markets to meet their revenue ambitions by crossing into immediately adjacent spaces, rather than follow the broader diversification seen in Europe.

The UK HCM business saw revenues grow by 18% to £2.9M. The Linux-based IT series sales increased 33% with organic growth being shown across the majority of clients. A new supply agreement with Workforce Software, helped bolster these figures although revenues from this client will not reach full potential until future years.

The GT-10 continues to provide new opportunities both in the UK and US. During the year a contract was signed to provide a variant of the GT-10 to a major European HCM partner and during 2019 this will become their flagship product. In the US, a supply agreement was reached with Ultimate Software to supply an OEM variant of the GT-10 which will be known as the UltiPro and will host Ultimate’s flagship SaaS solution that allows customers to access greater people management functionality in the cloud. Revenues came on stream in June. The US based business has also experienced good organic growth with increases in spend being seen in almost all of the client base so that revenues increased 46% to £1.2M.

In the Asset Protection division revenues decreased by 9.5% to £8M. Products revenue declined by 17% partly due to the decreased contribution from time delayed cash handling equipment sales to the Post Office so that cash handling equipment sales decreased by 42%. Overall revenue in all other product groups increased by 12%. The revenue in the year was characterised by numerous small projects with the absence of larger longer term high value projects and continued to be affected by branch closures in the banking sector. This was mitigated somewhat by staff reduction which resulted in cost savings.

During the year new products were developed with the focus on providing counter terror security equipment for staff and customer protection. The distribution agreement entered into with Gunnebo in the previous year to distribute their security doors and partitioning range within the UK increased exposure into new markets but sales have been disappointing to date. This complements the existing Safetell product range and the increased product offering allows entry into new market sectors. A three year fixed price supply contract with a financial institution ended in October but margins on this contract had been reduced due to imported component price increases directly related to the exchange rate.

A programme of product re-certification to the latest UK security standards which started in the previous year was continued which, when completed, will assist in moving the business forward as their focus is moved to the increased level of crime and threat of terrorism in the UK. The final element of the process will be completed in the second half of 2019.

Service revenue was 5% higher. Safetell continues to upgrade old legacy systems as customers invest in sites without the need to completely replace rising screens. TC105 control system upgrades will continue as customers decide to reinvest in the protection that rising screens provide.

In May the group acquired a new office property for £1.2M and after incurring refurb costs they entered into a sale and leaseback arrangement in September. The lease arrangement is for 15 years with increases in the annual rental rate at the five and ten year marks.

There were a number of exceptional items during the year. There were redundancy costs of £140K and impairments to development costs of £698K. In addition the remaining costs of the Hong Kong office closed last year came to £113K.

The group recognises that future access control revenues will be seen through sales of the current variant of the Sateon platform, the Janus C4 that will be introduced in the current year. They have therefore taken the decision to write off £698K which relates to sums capitalised for previous versions of the platform which have now been superseded. This is not the first time so it seems the group are not impairing their assets correctly.

The Janus upgrade programme has continued to contribute access control revenues as end users migrate to Sateon. Development work on Sateon has now been completed and a new access control platform is currently being developed with a third party supplier of security management systems to take advantage of the growing desire for fully integrated security and building management systems. It is expected that this new offering will be brought to market in H2 2019 and will sit alongside Sateon as two distinct platforms.

In Human Capital Management the GT-10 terminal continues to provide major opportunities with new and existing partners. Supply agreements have been executed in the year with two major software partners and a Linux port of the Android based terminal is currently being developed. The IT31 is to undergo a mid-life refresh which is expected to create new revenue opportunities and increase contribution with existing clients. During the year two new products were developed in the asset protection division with the focus on providing counter terror security equipment for staff and customer protection.

Going forward the board expects revenue growth in the electronic division following the completion of the two major supply agreements mentioned above, and recovery of sales in the asset protection division boosting both the current and future years. The development of the new access control platform being developed should also be completed in the year and the board expects improved financial results in the year. Whether they are expected to turn a profit is not mentioned, however.

As the group is loss making there is no point looking at PE ratios and there is no dividend on offer here. I can find no forecasts for the group.

Overall then this has been another difficult, but improving, year for the group. Losses and the operating cash outflow both improved but net assets deteriorated further. The Electronic division seems to be fairly healthy as the increased sales of the Sateon platform offset declines in Janus, and going forward the new supply agreements stand it in good stead. The asset protection division looks a little more flimsy, being affected by lower deliveries to the Post Office and banks, although again a recovery is being forecast.

I think the group may be on the cusp of real recovery but with no forecasts available to me and no current trading to base this on, I am going to have to stay out I think.