James Latham has now released their interim results for the year ending 2019.

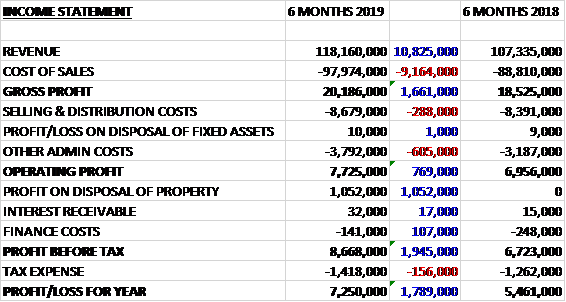

Revenues increased by £10.8M and cost of sales grew by £9.2M to give a gross profit £1.7M higher. Selling and distribution costs grew by £288K and other admin costs were up by £604K which meant that the operating profit increased by £769K. The group made a £1.1M profit on the disposal of a property and finance costs declined by £107K before tax expenses grew by £156K to give a profit for the period of £7.3M, a growth of £1.8M year on year.

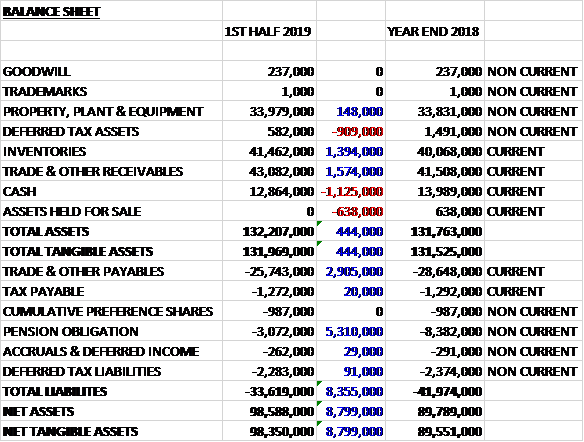

When compared to the end point of last year, total assets increased by £444K driven by a £1.6M growth in receivables and a £1.4M increase in inventories, partially offset by a £1.1M decline in cash, a £909K decrease in deferred tax assets and a £638K decline in assets held for sale. Total liabilities decreased when compared to the end point of last year due to a £5.3M fall in pension obligations and a £2.9M decline in payables. The end result was a net tangible asset level of £98.4M, a growth of £8.8M over the past six months.

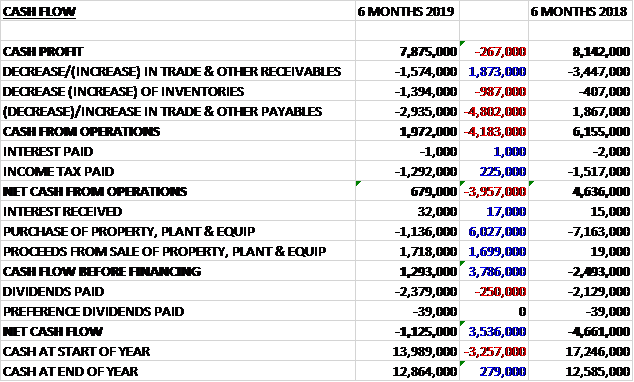

Before movements in working capital, cash profits declined by £267K. There was a cash outflow from working capital and despite tax payments reducing by £225K the net cash from operations came in at £679K, a decline of £4M year on year. The group spent £1.1M in capex but recouped £1.7M from the sale of a building to give a free cash flow of £1.3M. This did not cover the £2.4M paid out in dividends so there was a cash outflow of £1.1M and a cash level of £12.9M at the period-end.

Volumes increased by 1.5% and product prices were up 7.8% with increased sales of lower volume, higher priced products. Warehouse costs were up nearly 5% due to the increased cost of operating from the two new depots. Selling and distribution costs were 3.4% higher and transport costs per tonne were up 3% due to increases in fuel costs. Admin costs were higher due to an increase in bad debts.

The effect of a judgement confirming that pension schemes are required to equalise male and female guaranteed minimum pensions is still being assessed but is likely to increase pension liabilities by around £1M.

The second half of the year has started well with revenues continuing to grow. Margins, however, are slightly down with price rises being more difficult to absorb by the market. Customers remain busy though and are reporting good order books. The outlook is affected by the uncertainty caused by Brexit negotiations and the group will obviously suffer from any slowdown to the UK economy. They have reviewed their key European suppliers and have put plans in place to hold more stocks for a period of time in H1 2019 in order to mitigate any supply issues over that period. They are continuing to invest with extensive racking projects started at the Purfleet and Thurrock depots and the planned redevelopment of their Gateshead site in order to make the most efficient use of the space.

At the current share price the shares are trading on a PE ratio of 11.1 which falls to 10.8 on the full year consensus forecast. After an increase in the dividend, the shares are yielding 2.7% which remains the same for the full year forecast.

Overall then this has been a decent period for the group. Both profits and net assets increased but the operating cash flow deteriorated. This was exacerbated by working capital movements and the free cash flow did not cover the dividends. Volumes were up modestly but it is the pricing which has caused the profit to improve. So far in the second half, revenues continue to rise but margins are being squeezed as cost increases become harder to pass on. In addition, Brexit is looming large. The forward PE of 10.8 and yield of 2.7% look pretty good but there is real uncertainty here if the economy nosedives. Could be worth a punt at these levels.

On the 15th February the group announced that it had acquired Abbey Wood, an Irish timber merchant and the official distributor of Accoya Wood in the country. They paid an initial €1.8M with a further payment of €300K to €400K due for the net assets subject to completion accounts. In addition, an earn out of up to €400K is payable to the vendors subject to turnover targets being met. EBITDA for the business was €379K last year and it operates from sites in Dublin and Cork.

On the 21st March the group released a trading update. Revenue and profit for the year are expected to be in line with market expectations and the integration of Abbey Woods is going well with encouraging results so far.