Ricardo has now released its results for the half year ending 2014.

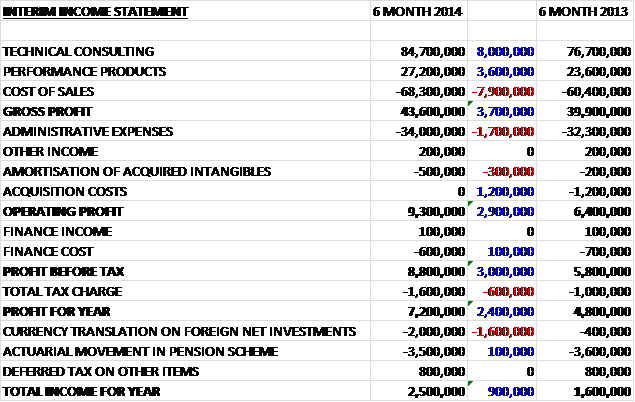

Revenues were up across both reporting segments, with Technical Consulting up £8M and Performance Products up £3.6M. Cost of sales also increased but not enough to prevent an increase in gross profit, up £3.7M. Admin expenses were up by £1.7M and there were no acquisition costs, which accounted for £1.2M last year so the Operating profit was up £2.9M to £9.3M. There was a slightly larger tax charge, as would be expected, so the profit for the half year was £7.2M, which was £2.4M higher than the same period of last year, but the increase was halved to a still decent £1.2M if the one-off acquisition costs from last year were removed.

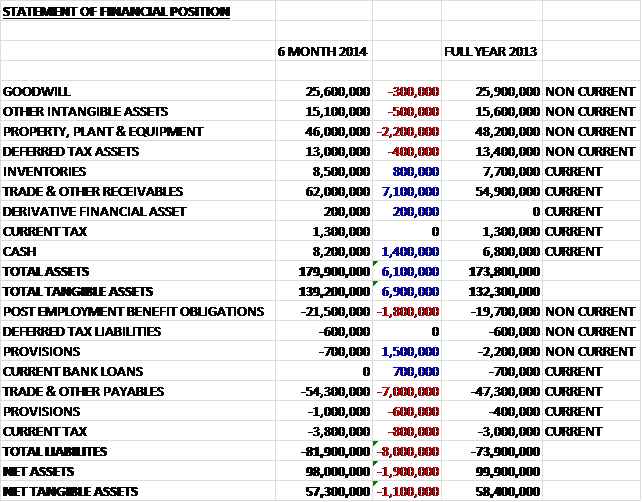

When compared to the end of last year, total assets at the half year point were up by £6.1M. This was driven by a £7.1M increase in the level of receivables, a £1.4M increase in cash and a £800K hike in inventories; somewhat counteracted by a £2.2M fall in the value of property, plant & equipment and a £500K reduction in other intangible assets. During the same period, we also saw an increase in liabilities, driven by a £7M hike in payables and a £1.8M increase in pension liabilities, somewhat mitigated by a net £900K fall in provisions and the elimination of the last remaining £700K of bank debt. Overall then, net assets fell by £1.9M, which is pretty much the amount of the pension liability increase.

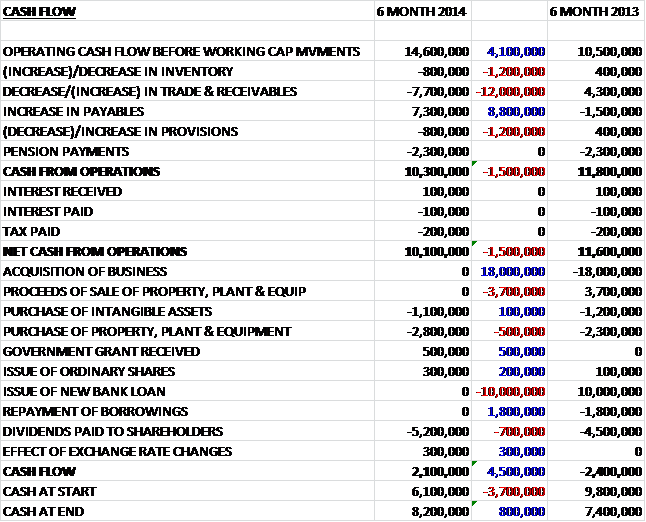

Before working capital movements, the cash flow for the half year was up by a fairly decent £4.1M. During the half year, both payables and receivables increased but at a broadly similar amount. Compared to last year, however, the increase in receivables was significant. The group also made £2.3M of pension payments and paid out negligible tax and a net of zero interest so the net cash from operations was £10.1M, £1.5M less than in the first six months of 2013 due to the increased receivables. As far as non-operational items are concerned, the only payments were a £5.2M dividend payment (up £700K), a £2.8M spend on property and equipment (up £500K), and a £1.1M spend on intangible assets. This time last year, the group also spent £18M on the acquisition of a new business and benefited from £3.7M of proceeds from the sale of fixed assets. It is impressive that the group has already been able to absorb those costs from cash flow as it has paid back all of the loans at the end of last year. Overall then, the cash flow was £2.1M at the end of the half, a decent amount given the small increase in capital expenditure and dividends.

Technical Consulting operating profit was £5.6M, up by £900K. The UK business continued to be the main driver of profits whilst the German and US businesses continued to face a challenging market backdrop and had a difficult start to the year. These businesses did gain traction in the second quarter, however, and the closing order book was very encouraging. In the motorcycle market the group are enjoying some success with new contract wins in China, Japan and Europe. The motorsport and high performance vehicle business also enjoyed a good start to the year with a number of large contract wins. In the passenger car sector, the group has experienced a good level of activity in Japan, China, the UK and US, along with emerging economies with the drivers coming from increased fuel efficiency and reduced emissions. The commercial vehicle market remained difficult but there were opportunities in China and Japan

The defence market seems to be continuing to perform well, with work in the UK and US continuing. The widely publicised reduction in US defence spending may have an effect going forward, however. The rail business continued to develop within a variety of territories with recent projects including engines, driveline, alternative fuels and strategic consultancy – natural gas as a fuel has been a particular engine for growth. The energy sector performed as expected with electrical energy storage a particular area for growth. The key area for growth within the marine market is the efficiency of propulsion systems to improve fuel consumption and the group has won a number of contracts to upgrade engines to run on alternative fuels such as natural gas. The group’s marine business is growing strongly in Europe, with increasing interest in Asia and North America. There was also a strong performance in environmental consulting and the group are looking to expand internationally there.

Performance Products operating profit was £4.2M, up by £600K. This performance was underpinned by increased motorsport activity and monorail transmissions, which offset a reduction in the delivery of defence vehicles. Production of the Porsche Cup transmission commenced in July, which marked the start of a long term supply agreement. The supply of engines to McLaren and clutch transmissions to Bugatti continued and as mentioned in the last update, a new contract with McLaren worth £40M per annum for the supply of engines will commence in 2016. In addition, products for formula 1 customers, Japanese Super GT and the Renault World Series continued. In Rail, the group continued to supply monorail transmission in Malaysia and received a new order for transmissions in Brazil. In Defence, the assembly of the Foxhound vehicles for the MOD continued but the final tranche has now been delivered.

Going forward, management has seen a steady increase in prospects in a number of key markets across Europe and North America and the Asian Pacific markets have remained hungry for technology transfer and new product development. The business will continue to benefit from the global trends in reducing carbon dioxide emissions, improving the efficiency of energy usage, the reduction of the release of pollutants and particulates and the addressing a changing global energy mix. The core areas of growth are in transport, security and energy.

Overall then, this is a good update – profits have increased across both areas and there seem to be a good number of new contract wins. Cash flow was good but net assets suffered a reduction, partly due to increased pension deficits. Going forward, there is a little bit of uncertainty in the defence market with reduced spending and the end of the supply of Foxhound vehicles to the MOD, so it will be interesting to see whether the group can absorb that. Management has declared an interim dividend of 4.3p per share, up from 4p last year, which gives an annual yield of 1.9% at the current share price. Net cash at the end of the half was £8.2M, up from £6.1M at the end of the last year. At these levels, I see the shares as a hold and am not going to add any more until the results of the lack of Foxhound deliveries can be seen.

On the 19th May the group released a management statement covering the first 10 months of the year. The order book at the end of April stood at £141M compared to £130M at the same point last year benefiting from a good level of orders from the US during April. Significant orders in the last four months included a large engine project for a major passenger car OEM in the US, a further DARPA order in the US and a commercial vehicle engine programme. Orders in the UK included further passenger car orders for large OEMs and in Performance Products, orders included the pre-production phase of he new McLaren project together with further motorport transmissions.

In the pipeline there are a number of projects for Chinese customers in the latter stages of negotiation and passenger car opportunities in the UK, US and Germany. In Performance Products, the group also signed a multi-year production supply agreement worth over £35M in revenues that will start in 2015. Revenues in the first ten months were up 3% on the same period of last year and profit was in line with expectations. Performance Products performed well but UK revenues in Technical Consulting was slightly lower than expected in Q3 due to delays to a project. Ricardo-AEA and Strategic Consulting continued to perform in line with expectations. The group are building momentum in the US and Germany with the order book in both locations ahead of that of the same period of last year. The group continued to have a net cash position despite working capital increases due to the changing mix of the customer base and the growth of performance products. Overall this was not a bad update but I am left a little disappointed at the slight slow down in revenue growth due to the delay to projects in the UK. Hopefully this will just have a temporary effect.

On the 17th July the group released a statement covering the final two months of the year. Customer activity in those two months was positive with a record year end order book and a good pipeline across multiple markets. Asia continued to perform well with orders being signed in China and Japan with further opportunities in the latter stages of negotiation. Profit performance for the year is in line with market expectations and revenue will be slightly above that of last year. Further cash generation in the period lead to a cash balance slightly ahead of expectations. Market conditions are strong in the UK and Asia and the US is showing improving conditions but Germany remains challenging. Overall a decent update with no real surprises, I remain a holder.