Tower Resources is an oil and gas exploration company focused on Africa in general, and more specifically Uganda, Namibia and Western Sahara. The most exciting asset is a 30% stake in a substantial field in Namibia. I am not sure how useful a financial analysis will be on a company like this but I will give it a try.

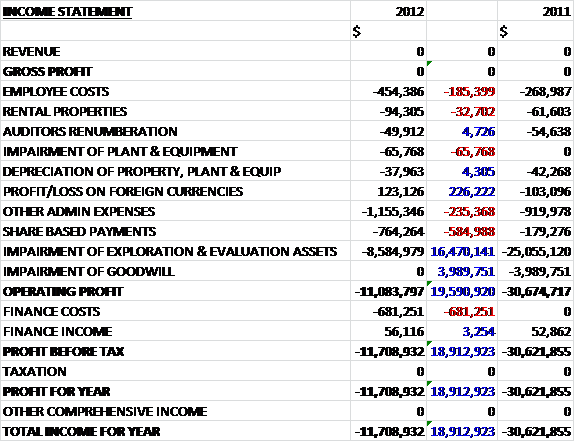

The group have not struck black gold yet so there is currently no revenue. The largest increases in operating costs are employee based with cash costs and share based payments both increasing. The group did manage to make a small profit on its foreign currencies but the largest cost is the impairment of exploration assets ($8.6M, down by $16.5M last year). The impairment, along with the impairment of equipment relates to the end of the Ugandan licence where the group failed to strike oil. It is notable that the group incurred financial costs this year, up $681K from nothing last year relating to the costs for new finance arrangements. No profits means no tax so the loss for the year was $11.7M, an improvement of $18.9M from 2011.

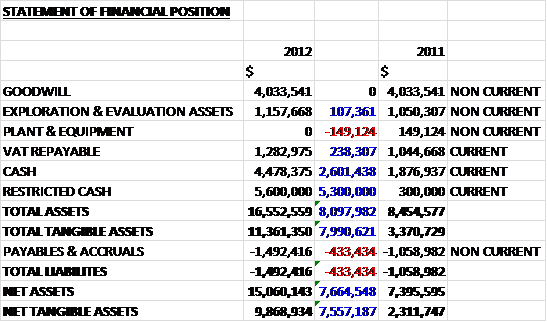

Total assets for the group were $16.6M, up by $8.1M when compared to last time. The increases were a $5.3M hike in restricted cash held in an escrew account ready to be transferred to Arcadia to double their interest in the Namibian license, and an extra $2.6M held in normal cash. The current capitalised E & E costs relate to the Namibian license ($1.2M) and the Western Sahara license ($225K). The receivables relate to VAT repayable by the Ugandan government which the group are negotiating over. The only liability comes under payables and mostly involves VAT withheld related to the Uganda operation, and again, the group are negotiating with the Ugandan government over this. Overall net assets nearly doubled to $15.1M and net tangible assets of $9.9M were $7.6M higher than in 2011.

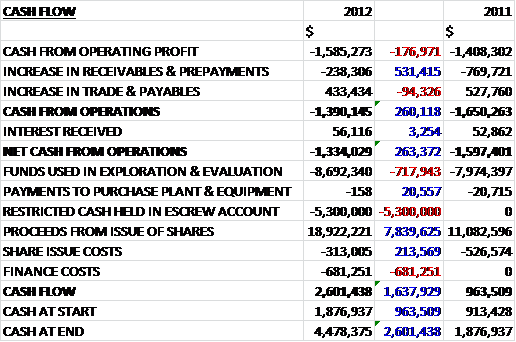

A cash flow analysis is probably more useful than some other measures. After favourable movements in working capital, the net cash outflow used in operations was $1.3M. The largest expense, as would be expected, was funds used in exploration, and at $8.7M they increased by $718K over last year. The group also spent $5.3M on the escrew account before it was used to acquire a higher stake in the Namibian asset. During the year, the group successfully raised $18.9M in a rights issue ($7.8M more than in 2011) to keep going and there was also $681K spent in finance costs, relating to the two new agreements mentioned below to secure extra financing, which was not present last year.

As can be seen from the above statements, there is quite a lot of impairment of assets. This relates to the full impairment of capitalised exploration and evaluation costs at its site in Uganda as the group failed to find any hydrocarbons there. The well was drilled at a cost of $8.6M and was relinquished in March 2012. The group has completed site restoration to the satisfaction of the Ugandan authorities and their bond was released in March 2013. They have retained a commercial presence in the country and will bid in the next licensing round.

During the year, the structure for companies working on the Namibian license changed. Tower doubled its holding to 30%, Repsol became the operator with a 44% interest and Arcadia makes up the rest with an interest of 26%. In order to complete the transaction, $5.3M was transferred from the escrow account, after the end of the balance sheet date, and will be capitalised under E&E. The asset covers three blocks, 1910A, 1911 and 2011A. The first well to be drilled on the Welwitschia, on the Delta structure, is due to be drilled early to mid-2014 and will go through the five identified reserves to a depth of 3,000m. 458M boe of risked recoverable reserves have been attributed to Tower’s 30% holding so we could be looking a potentially substantial amount.

Tower are not the only company drilling in Namibia, HRT have begun drilling offshore in the country so it will be worth keeping track of what they find, if anything. Recent geo-seismic studies within the block that Tower is part owner of have identified a number of direct hydrocarbon indicators. Although no commercial quantities of oil have been found in Namibia to date, the geology is similar to that in Congo, Angola and Brazil, all prolific sources in recent years. There have been two recent drills in Namibia. The Kabelijou exploration well drilled by BP, Petronas and Charity intercepted source rock but failed to discover commercial quantities of hydrocarbons. The other exploration well, the Tapir well drilled by Chariot announced It encountered sections of excellent quality reservoir but again, no commercial quantities of hydrocarbons were found.

As well as the geo-seismic data, there have also been sightings of surface seeps, pock marks and gas chimneys. The seismic data, as well as suggesting hydrocarbons are present, also provides evidence of the presence of sands in the Tertiary and Upper Cretaceous, and carbonate reservoir in the Lower Cretaceous. Within the license, there are four large leads. The southernmost, Delta, was covered by the 3D seismic survey and the first target, the Deep Maastrichtian, has an economic chance of success of 31%. Although this well has the highest chance of economic success, there is also Palaeocene with 19%, Upper Campanian with 9%, Campanian Wedge with 9%, Albian with 8%, Alpha Palaeocene with 12% and Gamma Palaocene with 9%. The Deep Maastrichtian is currently the most exciting, but given the sheer quantity of estimated reserves, Palaeocene is also a pretty decent prospect.

The total costs for the Namibian well is likely to come to about $30M, so obviously more funding will have to be obtained from somewhere. The group did enter into an $8M Standby Equity Distribution Agreement (SEDA) and a managed $3.125M SEDA backed loan agreement with YA Global Master, an investment fund managed by Yorkville. The loan can be increased in tranches of $1 up to a total of $6.125M. Also, an agreement was made with Darwin Strategic to enter into a £20M Equity Finance Facility (EFF).

Apart from Namibia, the other licence that Tower is currently involved in is in the Western Sahara. The group own a 50% interest in the offshore Guelta block and the onshore Bojador block, both of which are operated by Wessex exploration, the other 50% owner. In addition, the two companies have also entered into an assurance agreement for an interest in the Imlili block, also offshore. There has not been much exploration work in the country but high quality reservoir in wells drilled to date show some potential. Due to the political situation there, it is not currently possible to progress any exploration work on this asset but as part its acquisition in 2008, there is a potential contingent consideration payable should any future exploration activities be successful.

In June 2012, Graeme Thomson was appointed as the new CEO so it will be interesting to see if any new ideas are progressed. As things stand at the moment, there is no real chance of the Western Sahara license being progressed so this is pretty much a bet on whether they will find commercial quantities of hydrocarbons in Namibia. The lack of a find so far seems disappointing but given the size of the potential reserves, I think these shares are worth a (very) speculative buy. I am fairly comfortable with the 30% success rate for the first well.

On the 22nd May, the group released a statement regarding the HRT exploration well offshore Namibia. Whilst they did find some oil from thin sands, the principle target of the well, a carbonate reserve, was not as well developed as anticipated. Therefore no commercial quantities of oil were found. This well was 200km south of tower’s own Welwitschia prospect and while this well shows that oil has been generated and migrated, the lack of any large remaining reserves is disappointing.

On 2nd July, the group released a statement covering an update to the Competent Persons Report covering the Namibian well. Due to the discovery of light oil at the HRT well, there is considered to be a slight increase in the chance of an oil discovery. The estimate of net risked prospective resources at the Welwitschia well was increased from 458m mboe to 496m mboe.

On the 3rd July the group announced that acquired a 20% interest in the Marovoay block onshore Madagascar through the purchase of Wilton Petroleum ltd. The block is operated by Ophir energy and they have an 80% interest. The first exploration well is due to be drilled by mid-2014 and is targeting prospective resources of about 90m mbbls. The price for this acquisition is $1.75M in cash and shares equal to 7% of Tower’s equity, which values Wilton at $4.7M. There is also deferred consideration of $4M should the operator drill a second well. There does not seem to be huge potential here, but it is good to see the group branching out into other countries.

On the 5th July the group announced they had entered into a strategic partnership with Geoscience group PDF. They will provide exploration data tailored to the expanding needs of the company. PDF will earn a portion of its fee in Tower shares, which as management state, will align the fortunes of the two companies. It does seem, however, that Tower are creating quite a dilution of the share capital with these deals.

On the 5th July the group also announced a Namibian operational update. The drilling of the Welwitschia well is now planned to commence in mid-February and a firm rig is in place, the drilling location is agreed, the site survey is largely completed and the long lead time items are being manufactured. The new build Rowan Renaissance, on a three year contract with Repsol, is being used for the drilling. The rig will be delivered in December and move directly to Namibia for its first assignment. The budget is currently at $27M, with Tower’s share currently $8.1M to be called in the second half of the year. The board expect Tower’s share of the total cost to be $24M. The group are looking at various sources of financing for the well, including farm-out, asset swap and an equity raise.

On 22nd July, the group released a statement covering the recent exploration well drilled by HRT in Namibia. Although reconfirming the presence of an Aptian marine source, they failed to find the presence of quality reservoir in the primary Murombe objective. This was the second in three wells being drilled by the company and is located 200km south of Tower’s main project. A secondary target, the Baobab reservoir was found to be water-wet so the well is being prepared for plugging and will be abandoned. This is another failure in a similar area but it the question must be asked – where have the oil reserves migrated to?

On 25th July, the group announced a placing of £9M and an open offer of up to £4.1M. The proceeds will be used to fund the company’s share of the 2013 costs associated with the Welwitschia well in Namibia, the cash portion of the Wilton acquisition, for general working capital purposes and to enhance the ability to pursue new ventures. The placing will be offered to certain existing and new customers at a price of 1.125p per share. The directors are participating in the placing, investing £1.2M. There was also an announcement that they intend to farm out a 10% interest in the Namibian license to fund the 2014 drilling costs. If it is unable to farm out this interest, it is expecting that the company will have to seek additional funding in order to meet its remaining ongoing work obligations under the Namibian license.