Ashley House have now released their final results for the year ended 2018.

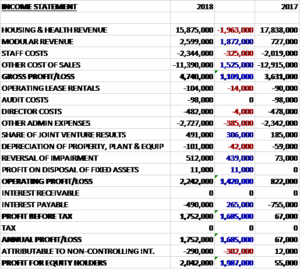

Revenues declined slightly when compared to last year as a £1.9M growth in modular revenue was offset by a £2M decline in housing and health revenue following the creation of the joint venture. Staff costs increased by £325K but other cost of sales were down £1.5M to give a gross profit £1.1M higher. Admin expenses increased by around £400K and depreciation was up £42K but the share of joint venture results increased by £306K and there was a £439K increase in the reversal of an impairment to give an operating profit £1.4M higher. Interest payments fell by £265K which meant that the profit for the year was £2M, a growth of £2M year on year.

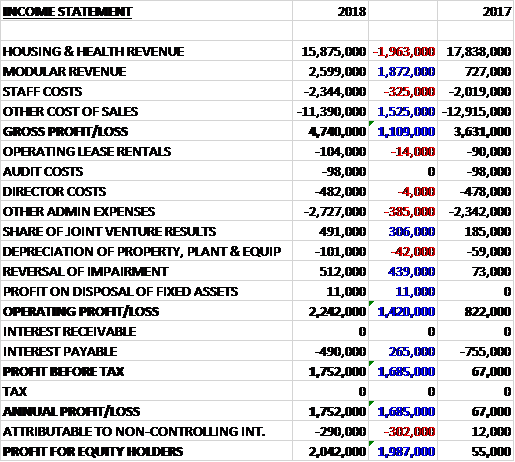

When compared to the end point of last year, total assets increased by £537K driven by a £793K growth in the investment in joint ventures, a £775K increase in prepayments and other receivables and a £582K increase in trade receivables, partially offset by a £1.1M fall in the value of work in progress. Tital liabilities declined during the period as a £320K increase in deferred income was more than offset by an £894K decrease in the bank loan, a £258K reduction in retentions held on contracts and a £716K fall in other payables. The end result was a net tangible asset level of £5.1M, a growth of £1.8M over the past six months.

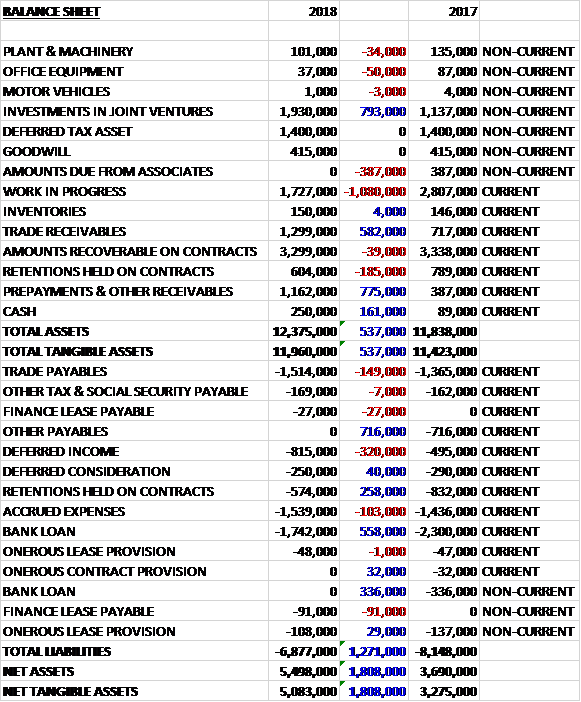

Before movements in working capital, cash profits increased by £1.2M to £2M. There was a cash outflow from working capital but interest payments reduced by £265K to give a net cash from operations of £1M, a growth of £779K year on year. The group only spent a net £3K on capex so there was a free cash flow of £1M. After most of this was used to pay back loans, the cash flow for the year was £161K and the cash level at the year-end was £250K.

In October the Prime Minister announced that the Local Housing Allowance cap that had threatened to restrict the amount of housing benefit available for schemes such as those developed by the group would not after all be imposed. The group was subsequently able to take three extra care schemes to financial close and on to site. This event has enabled the unblocking of the pipeline of extra care developments and with the threat to rental schemes significantly diminished the improved investability of those schemes has stimulated demand and the group have seen an increasing number of REITs as well as Housing Association clients keen to acquire this type of property.

In December a 50:50 joint venture was established with Morgan Sindall Investments to deliver extra care housing, care homes and supported living housing. The partner brings complementary quality and skills in supported living, long term strategic property partnerships with local authorities and the NHS, and a broad range of expertise in investing and managing institutional capital. The relationship between the two parties developed well so far and Morgan Ashley is already extending MSIL’s offer to Local Authority partners which is further extending its pipeline. With the first scheme already on site, future prospects are healthy.

During the year Morgan Ashley’s first scheme, an extra care facility on the Isle of Wight, reached financial close and commenced on site. The Ryde scheme comprises 75 extra care apartments with communal areas together with 27 affordable bungalows. The scheme will be operated by Southern Housing and owned and financed by Funding Affordable Homes.

The group has started on site with an extra care scheme in Scarborough. This is a collaboration with Home Group, Scarborough Council and North Yorkshire County Council and will provide 63 apartments for over 55s and those with extra care needs. The scheme will also see facilities including a restaurant and cage. Contracts have also been signed with the care provider HSN Care for a second care facility, this one located in Peterborough. The scheme will provide specialist accommodation for twelve disabled young adults. The modular component of the development is being built by F1 Modular. Both Scarborough and Peterborough sit outside the joint venture.

Despite the continuing limitations on government funding in primary care, the group have recently completed three health schemes. The first is a diagnostic treatment centre near Durham for City Hospitals Sunderland. The second is a GP surgery development in Essex and the third is Wales’ first fully integrated family centre and primary care centre in Swansea. All three schemes were funded by Assura.

F1M is now a 76% owned subsidiary of the group. While the business was lossmaking this year, recent orders have secured its activity for the coming months and the board expects it to contribute to profits in 2019.

The profit this year included the £512K write back of an impairment previously recorded against the carrying value of a loan receivable from an associated company. The group holds 33% of Partnering Health which provides out of hours and other medical services. Whilst management had expected to recover the full value of the loan in due course, the performance of that business improved during the past year such that is was able to advance significant repayments ahead od when it had previously been expected.

The housing and health pipeline now stands at £206.4M across 22 schemes compared to £212M across 28 schemes. Currently four are in the factory with a total development value of £8.6M. There are a further seven identified schemes at advanced stages with a total development value of £9.9M.

There is no doubt that government policy in recent times has hampered development opportunities but recent developments have enabled the group to push forward with its extra care and supported living pipeline. The outlook for the group has improved and the board is confident that the pipeline it has built in recent years can now be unblocked.

At the current share price the shares are trading on a PE ratio of 4.8 which falls to just 3.7 on next year’s consensus forecast. There are no dividends on offer here. At the year-end the group had a net debt position of £1.5M compared to £2.5M at the end of last year.

Overall then this has been a positive year for the group. Profits are up, net assets increased and the operating cash flow improved with a decent amount of free cash being generated. The outperformance seems to be down to the reversal of the housing allowance cap from the government, and aided by the joint venture. Things are starting to move here and the forward PE of 3.7 looks a bit unjustified to me. I’m happy to hold, might even buy some more.