Ashley House has now released its interim results for the year ending 2017.

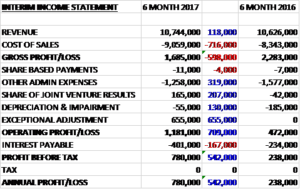

Revenue increased by £118K during the period but cost of sales grew by £716K so the gross profit was down £598K due to the increase in construction income which has a lower margin than pre-construction income. Admin costs declined by £315K, however, and the joint venture enjoyed a £207K swing to profit. There was also a £130K reduction in depreciation and impairments and a £655K exceptional adjustment relating to an agreement to cancel a historic liability with a counterparty, which meant that the operating profit grew by £709K. We then see a £167K increase in interest charges so the profit for the period came in at £780K, a growth of £542K year on year.

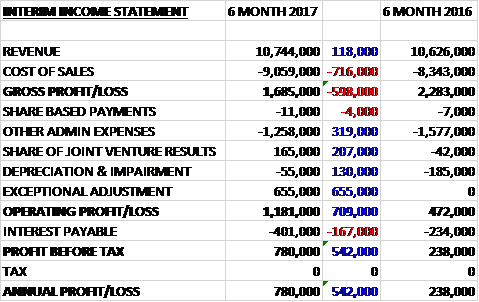

When compared to the end point of last year total assets increased by £1M driven by a £1.1M growth in receivables. Total liabilities also increased as a £385K growth in the bank loan was partially offset by a £147K decline in payables. The end result was a net tangible asset level of £4.6M, a growth of £809K over the past six months.

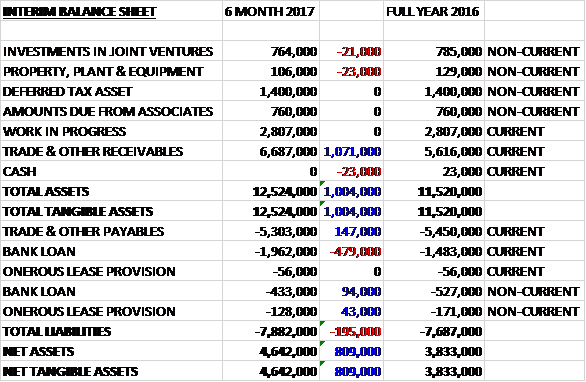

Before movements in working capital cash profits increased by £483K to £1.2M. There was a cash outflow from working capital, however, with a £1.1M growth in receivables and after interest payments grew by £167K there was a cash outflow from operations of £426K, a £130K improvement year on year. The group only spent £5k on capex and £90K in loan repayments so the cash outflow in the half was £498K and the cash level at the period-end was £475K.

The group continue to wait for full clarity on the government’s proposal to top up housing benefit at a local level to fund supported housing. A consultation process started in November where the government reiterated that it is committed to protecting and boosting the supply of supported housing.

Ashley House continues to work with their clients, both councils and registered providers, to find solutions to enable at least some of their pipeline schemes to proceed whilst this consultation continues.

This month’s announcement by the Homes and Communities Agency of grant funding for the next five years included Ashley House with £11.5M of funding for five of their current schemes. In addition, a registered provider partner has been awarded another £7.5M for another three of their schemes. The total of £19M of grant funding is an opportunity for the business to develop out these schemes once the government’s position on social rents becomes clear.

In each case the grant funding allows the rents to be around 20% lower than they would have been and makes the schemes acceptable to the Local Authority Housing Benefits team. It does not in itself close the gap created by the capping of housing benefits to local housing levels but it should help unlock schemes. Having successfully completed their extra care scheme in Harwich last month, they remain n site with the scheme in Walton on the Naze which is due to complete in the coming weeks. The board currently believe that three schemes in their extra care pipeline will be able to reach contract before the year-end, thereby qualifying for revenue recognition but they still all require local authority and partner board final approvals.

The group will continue to diversify in order to lessen the exposure to the risk of Government making changes that affect the fundamental elements of the business. They continue to work with a modular construction contractor through a joint venture company to increase the speed and efficiency of their existing build programmes which is enabling them to tap into a new range of products and development opportunities and start to move away from a reliance on government funded schemes.

In the Health segment they have started construction on two new schemes, a fully integrated GP surgery and family centre complex in Swansea and the redevelopment of an old school building into new surgery premises in Wivenhoe. The diagnostics and treatment centre in Durham will start on sire in the coming weeks. In addition they continue to support their partners Integrated Pathology Partnerships in the programme of creating new pathology labs.

There are currently three schemes on site – Walton on the Naze in extra care and the health schemes in Swansea and Wivenhoe compared to four last year – the Harwich extra care scheme was completed in December. There is a total forward pipeline of 25 schemes with £170.7M of revenue anticipated compared to 31 schemes worth £177.2M at this point of last year.

The ongoing government consultation relating to funding for supported housing means that a further complication is added to the process of contracting on schemes. Subject to the timing risk of some of these schemes, the board expects that the group will be profitable in the full year.

At the current share price the shares are trading on a PE ratio of 16.7 which falls to 2.7 on the full year forecast which I find hard to believe. At the period-end they had a net debt position of £2.4M compared to £2.6M at the same point of last year.

Overall then this has been a period where not a great deal has happened! Profits did increase but this was due to a historic liability being cancelled, without which profits fell due to an increase in interest costs. Net assets grew, however, as did cash profits, although there was still a cash outflow at the operating level reflecting increased receivables. The health projects seem to be ticking along OK but the issue really is the lack of clarity over how the government is going to top up housing benefit to fund supported housing – if indeed it is. I suspect this is why there is only one Extra care project on sire and the pipeline is not being replenished. The forward PE of 2.7 looks like a nonsense to me and I find it hard to want to invest here until there is more clarity over the future of the Extra Care schemes.

On the 14th March the group announced an acquisition and released a trading update. The trading update highlights the risk of delays to the closing of certain projects arising from ongoing uncertainty of government funding support for such projects which might result in revenues being delayed from this year into the next financial period. As a result, the board have been seeking revenues less dependent on government funding hence the acquisition.

The group, through their joint venture subsidiary, F1M, have acquired their former modular off-site construction partner. They have also increased their holding in F1M to 76%. F1M is the only modular contractor to hold a place on local government’s national framework for housing and is currently bidding to deliver mixed developments including private accommodation. The short term pipeline includes contracted housing for two local authorities, specialist units for a Welsh council, and a flow of work with an innovative retail developer delivering ready built retail pods. The business is seeking to extend its reach into schools, student accommodation and other similar products which are well suited for building in a factory before being transported to site.

It is also capable of delivering a significant proportion of the group’s own pipeline as they will use a mixture of off-site and traditional build methods for its schemes. It is this ability to provide an integrated approach involving a modular solution which was a key benefit in their recent bid win in York of a 70 bedroom care home. This scheme is expected to start onsite during the next financial year.

The business is being acquired by F1M from administration and produced a loss of £93K in 2015. F1M have agreed to pay £114K for the assets of the business and is entering into a new lease on the factory with an option to acquire the freehold over the next six months. The increase in holding in F1M from 52% to 76% was for a consideration of £250K, £240K of which is payable only when the enlarged F1M business is profitable.

Overall then this is a decent enough acquisition but it is for the future and it is looking increasingly likely that the group will not hit targets this year. I am steering clear for now.

On the 25th April the group announced that it had signed a new loan facility of £500K with the deputy Chairman secured against some assets of the company. This doesn’t quite sit that well to me.