Asian Citrus have now released their interim results for the year ended 2015.

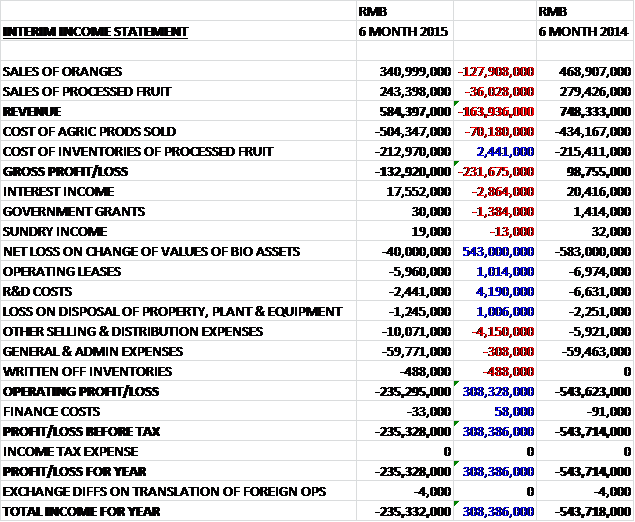

When compared to last year, revenues fell by £16.4M driven predominantly by the £12.8M decline in the sales of oranges, although sales of processed fruit also fell by £3.6M. To make matters worse, cost of sales increased due to increased fertilizer and pesticide usage following the typhoon and canker outbreak to give a gross loss of £13.3M, a reversal of £23.2M compares to the first half of last year. Selling and admin costs were broadly flat and the non-cash loss on the biological asset values was better than last time which meant that because of this, the loss for the year was some £30.8M better at £23.5M. Still a pretty terrible performance, though.

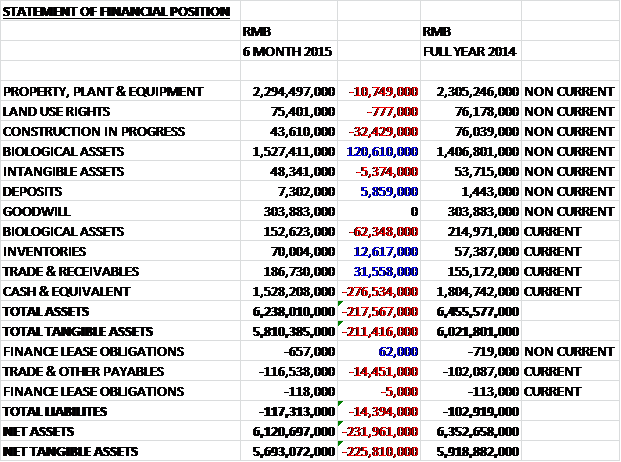

When compared to the end point of last year, total assets collapsed by £21.8M. This was driven by a £27.7M decline in cash levels somewhat offset by a £5.8M net increase in the value of biological assets. Liabilities remained fairly flat, increasing by just £1.4M due to a growth in payables. The end result is a £22.6M decline in net tangible assets to £569.3M which if accurate, seems pretty strong.

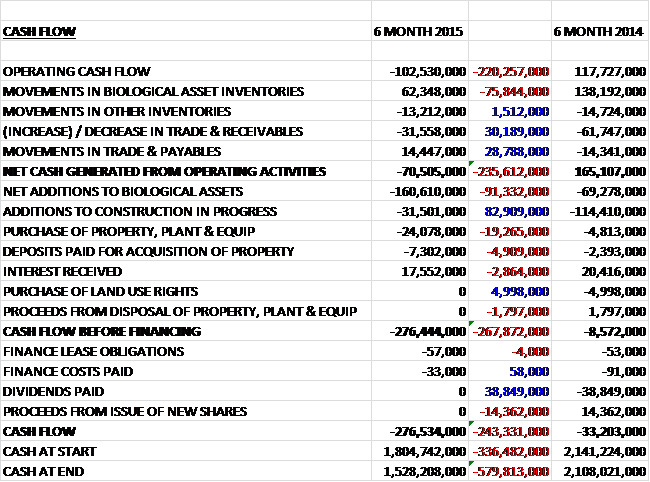

Before movements in working capital cash losses were £10.3M, a £22M detrimental swing when compared to the first half of 2014. Due to movements in biological asset inventories, this improves somewhat to a £7.1M cash loss which was still £23.6M worse than last time. The group then spent £16.1M on new biological assets, presumably to replace those lost in the storms and a further £5.6M on capital expenditure so that the cash outflow before financing was £27.6M, of which there was negligible amounts so that the cash outflow for the six month period was a pretty terrible £27.7M, some £24.3M worse than in the first half of last year. The group apparently still has a pretty sizeable cushion though, with £153M cash left in the bank. Although following recent scandals involving Chinese companies listed on AIM, one has to wonder whether this cash is really present. The HK listing does help somewhat in this regard, though.

The Agricultural Produce business made a loss of about £22.7M, an improvement from the £57.6M loss incurred last year. The production yield at the Hepu plantation decreased by 71% to just 7,146 tonnes, mainly due to the extensive damage from the impact of Typhoon Rammasun but the arrival of Typhoon Seagull in September didn’t help either. The oranges the group did manage to sell suffered a 40% fall in average selling price due to their poor appearance following the canker outbreak. The production yield at the Xinfeng plantation decreased by nearly 16% to 103,847 tonnes and was affected by cryogenic freezing rain (hail?) and frosts in early 2014 that affected the fruit blossom, although the average selling price for Xinfeng oranges did increase by 3%. Conversely the drought and high temperatures from September to December caused a water scarcity for irrigation which impacted the size of the winter orange crop.

The Processed fruit business made a profit of about £450K, a decline from the £4.8M profit during the first half of 2014. The fall was mainly due to a decrease in the sales of pineapple juice concentrate due to limited raw material supplies after Typhoon Rammasun destroyed a significant volume of the fruit crop. The average utilisation of the BPG was approximately 83% and with costs remaining broadly flat, the business still managed a 12.5% margin, a decline from the 23% margin achieved last year.

During the period it seems that the group is having some trouble collecting receivables in a timely manner. A total of £2.9M were overdue during the first half of this year out of a total of £10.2M compared to £1.4M out of £8.7M last time round. Apparently these are from a variety of different customers, though, so there is hopefully not too much risk tied up here.

After 26,960 grapefruit trees were planted, the construction of the Hunan plantation is now complete with 1.05M summer orange trees and over 750,000 grapefruit trees, but as mentioned at the end of last year, operations were delayed but remain on schedule to begin production in 2016. At the beleaguered Hepu plantation, after being replanted the first harvest of banana trees is now expected in September 2015. In all, the Hepu plantation now has 975,000 summer orange trees, 268,557 winter orange trees and 221,769 banana trees. The Hunan plantation has 1,049,875 summer orange trees and 750,320 grapefruit trees and the Xinfeng plantation has 1,600,000 winter orange trees.

Going forward high levels of costs are expected to be incurred in the short term and due to the weak condition of the trees it will take a number of years for harvests at both plantations to fully recover to previous levels. In the second half of the year, management expects conditions to remain demanding so there doesn’t seem to be any near term improvement in sight.

The board have elected not to pay an interim dividend this year. Whilst this has undoubtedly been a poor six months for the group, it does appear that there should be plentiful cash to pay a dividend if they were mindful to do so as the net cash position fell by £27.7M to £152.8M during the last six months.

Overall this performance is pretty terrible. The group is loss making, net assets are down and there was an outflow of cash. Going forward, there seems little prospect of a return to previous profitability in the short term and the sheer number of natural disasters to befall the Asian Citrus plantations is just incredible. On the plus side, the banana crop should be ready by the end of the year as long as they don’t get uprooted in a bit of a breeze and if the accounts are to believed, there is still a strong balance sheet and plenty of cash. I will not be investing here though until such a time that there at least a bit of good news.

Unsurprisingly the chart looks pretty terrible – I would touch this share with it looking like this.

On the 20th March the group announced that it had concluded negotiations on the pricing with its customers for the forthcoming summer orange crop. They will supply 20,100 tonnes of oranges from the Hepu plantation which is a decrease of 59% when compared to the same period last year. The production yield was impacted by the previously announced typhoons. To heap more misery on investors, the average selling price of the orange crop is expected to be 33.5% lower than last year as a result of the typhoon damage and poor appearance of the oranges due to the canker outbreak. The board believes that these factors will continue to adversely affect the performance of the group’s operations going forward – no light at the end of the tunnel yet here then.

On the 15th April the group announced yet more bad news. They have identified the presence of Huanglongbing, also known as Citrus Greening Disease which is a bacterial plant disease spread by the Asian Citrus Psyllid. Once infected, the disease is fatal to trees and the only control is through pesticides against the insects that spread it. It is thought that about 18% of the trees in the Xinfeng plantation will be affected and will have a significant impact on the 2015 winter harvest. What else can possibly happen to Asian Citrus? Perhaps a plague of locusts?

On the 7th May the group confirmed that the rate of infection of HLB disease is approximately 18% of the total orange trees in Xinfeng. In order to prevent its spread and protect the unaffected trees, about 300,000 diseased trees will be removed this month. The costs of the removal and additional pesticides is about £1.2M which will be incurred in Q4 this year. Apparently the insurance policy does not cover damage from disease (just like it didn’t cover bad weather – I am not sure if it covers anything) so there will not be any reimbursement for these losses. As a consequence of the above, there will be a significant reduction in the winter harvest at Xinfeng which will have an adverse effect on the results for the year ending 2016. Certainly no light at the end of the tunnel yet here!

On the 5th June It was announced that the actual summer orange crop yield at the Hepu plantation was 19,132 tonnes compared to 49,540 tonnes last year and broadly in line (although actually a bit lower) than the previous guidance of 20,100 tonnes. The annual production yield for the group decreased by 34% to 130,120 tonnes. The board believes that the reduction yield of orange crop, citrus canker and Huanglongbing disease will continue to adversely influence the performance of the group’s agricultural produce operations. This is pretty desperate stuff so I am very puzzled by the share price response to the announcement!

Sometimes the stock market never ceases to amaze me. Something seems to be going on but I am steering clear of this one.

On the 13th July it was announced that the company’s shares had been suspended on the Hong Kong exchange pending the release of an announcement in relation to the disposal of shares off market by a substantial shareholder.

Later in the day it was announced that Changjiang Tyling Management Company had purchased 179,252,394 shares representing over 14% of the total issued share capital from Market Ahead Investments ltd who used to be the largest shareholder. Changjiang is half owned by Mr. Ng Ong Nee. Market Ahead is majority owned by Mr. Tong Wang Chow who resigned as CEO last year so this transaction is basically transferring the old CEO’s share of the company to the new CEO so I don’t think much can be read into it. The suspension in Hong Kong has now been lifted.

On the 9th September the group released a trading update for the full year. It is anticipated that turnover in 2015 will be lower and the core loss for the year will be significantly higher than last year. Turnover for the half year was down nearly 22% and the outturn for the full year will reflect a similar performance. The core net loss is expected to be more than double the RMB193M reported in the first half. This deterioration reflected the significant impact of the Huanglongbing disease infection at the Xinfeng plantation and the damage sustained from Typhoons Rammasun and Seagull which affected both production yield and selling price of the orange harvests, which were down 15% in the year.

The processed fruit business saw comparable sales tonnage decrease marginally compared to last year but was loss making due to the increased cost of raw materials owing to limited supplies, the increased material scrap and maintenance costs caused by low productivity of the production equipment and increased labour costs. The assessment of the net change in fair value of biological assets for the year is still under review but I doubt it will be good!

What a shame, this company seemed to have real potential a few years ago but it is one thing after another and to be honest, anyone investing here at the moment really needs to think long and hard about what they are doing! Despite the dual listing in Hong Kong, this really is looking more and more like a dodgy Chinese investment with each update.