Avon Rubber has now released its interim results for the year ending 2017.

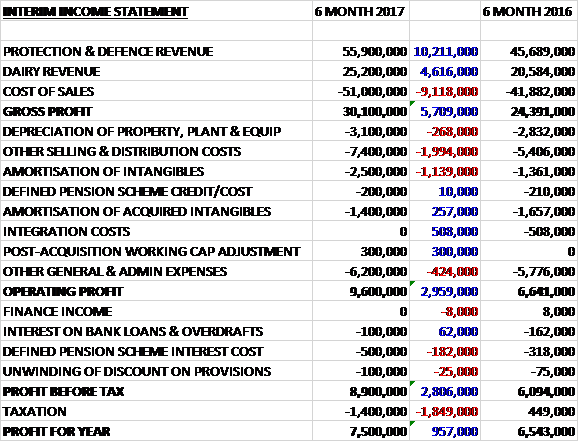

Revenues increased when compared to the first half of last year due to a £10.2M growth in protection and defence revenue, and a £4.6M increase in dairy revenue, both mainly as a result of currency movements. Cost of sales also increased to give a gross profit £5.7M higher. Depreciation was up £268K and other selling and distribution costs increased by £2M. We also see a £1.1M growth in the amortisation of intangibles, partially offset by a £257K decline in the amortisation of acquired intangibles, no integration costs (which counted for £508K last time) and a £300K post-acquisition working capital adjustment. After a £424K growth in other admin expenses, the operating profit was up £3M. Interest costs increased somewhat and tax charges saw a £1.8M negative swing which meant the profit for the period was £7.5M, a growth of £957K year on year.

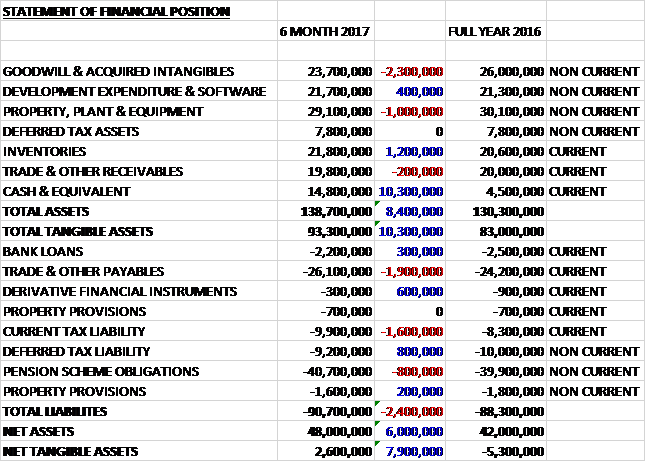

When compared to the end point of last year, total assets increased by £8.4M to £138.7M driven by a £10.3M growth in cash, a £1.2M increase in inventories and a £400K increase in development expenditure, partially offset by a £2.3M decline in goodwill and acquired intangibles along with a £1M fall in property, plant and equipment. Total liabilities also increased during the period as an £800K decline in deferred tax liabilities was more than offset by a £1.9M growth in payables, a £1.6M increase in current tax liabilities and an £800K growth in pension scheme obligations. The end result was a net tangible asset level of £2.6M, a growth of £7.9M year on year.

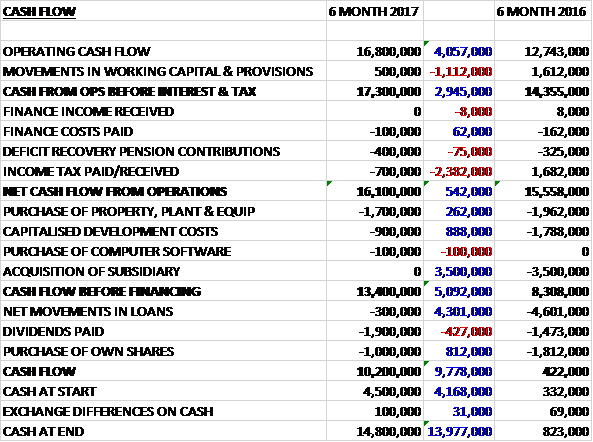

Before movements in working capital, cash profits increased by £4.1M to £16.8M. There was a small inflow of cash from working capital but this was lower than last time and after a £2.4M detrimental swing to tax payments, the net cash from operations was £16.1M, a growth of £542K year on year. The group spent £1.7M on property, plant and equipment along with £1M on intangible assets so the free cash flow came in at £13.4M. Of this £1.9M was spent on dividends, £1M on shares and £300K in loan repayments. All of which meant the cash flow for the period was £10.2M and the cash level at the period-end was £14.8M.

The group benefited strongly from the weakening pound which accounted for £1.3M in extra underlying operating profit.

The Profit in the Protection and Defence division was £7.6M, a growth of £1M year on year excluding last year’s integration costs. M50 respirator sales to the DOD were, as expected, slightly lower at 93,000 systems. During the period the group received a further order for 131,000 systems, providing good visibility of revenue under this contract. Higher volumes of M61 filter pairs were secured allowing them to deliver 95,000 pairs during the period compared to 36,000 last time. The board continue to believe the end user demand for this product will grow as the deployment continues to expand and they anticipate further orders in the second half.

Sales to foreign military, law enforcement and first responder customers increased year on year as the portfolio continues to grow. The acquisition of Argus has seen the Mi-TIC product range contribute to the sales growth in the fire market, where they have also seen organic growth in sales of their Deltair Self Contained Breathing Apparatus. AEF has experienced a first half in line with the prior year, reflecting the variability in timing of certain DOD procurement programmes.

Order intake for the division totalled £67.1M compared to £55M last time. Of the closing order book of £32.5M, £19M is for delivery in the second half of the year. Negotiations with Middle East customers continue to make progress and they expect to receive orders this year. Significant military opportunities for high value sales of M53A1 respirators and the aircrew XM69 programme are materialising to offset the expected reduction in the JSGPM M50 respirator mask programme.

The profit in the dairy division was £3M, an increase of £500K when compared to the first half of last year. The market environment for the business has been positive following the improvement in milk prices. Following an extended period of market weakness, conditions for dairy farmers, particularly in Europe, have improved as milk prices have increased. The dairy business has become less dependent on OEMs as they continue to grow sales of their own high margin milkrite/Interpuls branded products and their market share continues to increase.

Following their strategy to expand farm services, the growth of their cluster exchange service remains at encouraging levels in both North America and Europe. They completed farm pilots for the Pulsator Exchange Service and will launch in North America during the second half of the year. The pilot farms for the Tax Exchange Service will be installed during the second half. The farm service model should lead to a more robust and sustainable business model with the potential to grow a significant recurring revenue stream which is less susceptible to a cyclical milk price.

The board are pleased with the integration of InterPuls into the wider dairy business and are on track to realise the long-term benefits that have been identified, in particular the sale synergies available in the North American market. InterPuls products are already being rolled out through Milkrite distribution channels with a pipeline of opportunities being developed.

In emerging markets, including China, Brazil and India, the number of dairy cows being milked using automated milking processes is growing rapidly. This is adding to the market potential for the products the group sells. The sales and distribution operations they have opened in China and Brazil are progressing as they expand their dealer and distribution networks in these regions.

After an increase in the pension deficit it was agreed to increase deficit repair contributions to £1.5M per annum from £700K per annum with the revised contributions payable half-yearly. During the period Rob Rennie and Andrew Lewis resigned and were replaced with Paul McDonald as CEO and Paul Rayner as Interim Finance Director so there might be quite some disruption due to this. In May it was announced that Nick Keveth will be joining the board as finance director when Paul will step down.

The first half of the year has been positive and the group have grown their order pipeline. With a continued strong US dollar against Sterling the board anticipate a forex tailwind in the year and against the backdrop of anticipated increases in US defence spending and continuing improvement in milk prices, the board remains confident of achieving current year expectations.

At the current share price the shares are trading on a PE ratio of 18.2 which falls to 16.8 on the full year consensus forecast. After a 30% increase in the interim dividend the shares are yielding 1% which increases to 1.1% on the full year forecast. At the period-end the group had a net cash position of £12.6M compared to £2M at the year-end.

Overall then this has been a strong period for the group. Profits increased, net assets grew and the operating cash flow increased with plenty of free cash being generated. The group has been benefiting from the weakness in Sterling and quite a large chunk of this good performance is due to that but they have also seen underlying growth with most of the protection and defence division seeing strong demand and the improving milk price driving growth in the dairy division. With a forward PE of 16.8 and yield of 1.1% these shares are not cheap but I am tempted to get back in to this top quality company.

On the 23rd May the group announced the award of a contract to supply about 37,000 of their FM50 respirators together with a range of related spares and accessories. They expect to fulfil the order during the first half of 2018 and it reflects their further expansion into foreign military markets.

On the 31st August the group announced that CEO Paul McDonald purchased 6,170 shares at a value of £58.5K.

On the 12th September the group announced that the division head of protection Leon Klapwijk purchased 7,325 shares at a value of £69K.

On the 15th September the group released a trading update covering the second half of the year where they stated that full year pre-tax profit would be in line with current market expectations. In Protection, over the year as a whole they expect to deliver 152,000 M50 mask systems and 144,000 spare filter pairs under their sole source contract with the US DoD. In addition, due to scheduling requirements, they now expect to fulfil the order for 37,000 FM50 general purpose masks announced in May during the current year. Order intake in the second half has continued to be strong across all three market segments, providing good visibility for next year.

The dairy market environment has continued to be positive with improved milk prices reflected in increased farmer confidence. The growth trends in the first half of the year have continued into the second half with strong growth in sales of Inter Puls products in particular. All this seems fine, I continue to hold.