Avon Rubber has now released their interim results for the year ending 2018.

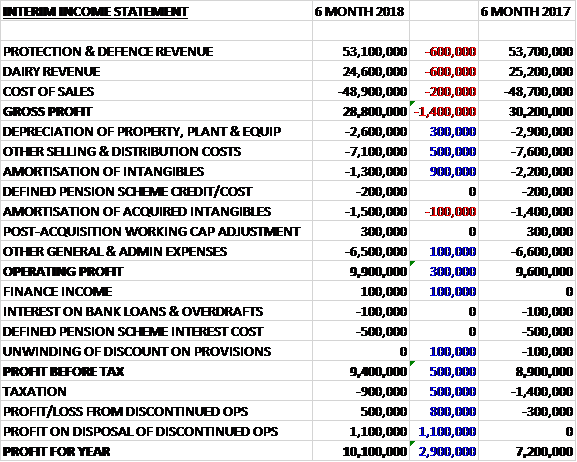

Revenues declined (although there was a growth at constant currency) when compared to the first half of last year with a £600K decrease in protection and defence revenue and a similar £600K fall in dairy revenue. Cost of sales grew by £200K which meant that the gross profit was £1.4M lower. Depreciation declined by £300K and other selling and distribution costs were down £500K. We also see a £900K decrease in amortisation to give an operating profit £300K higher. Finance income was slightly higher and tax charges fell by £500K to give a profit for the year of £8.5M, a growth of £1M year on year.

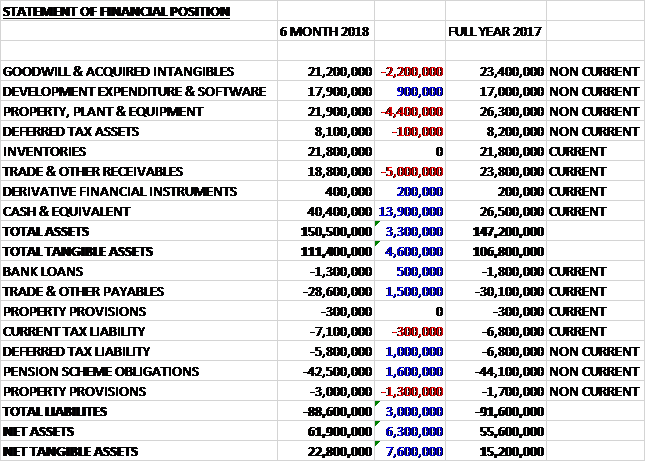

When compared to the end point of last year, total assets increased by £3.3M, driven by a £13.9M growth in cash, partially offset by a £5M decline in receivables, a £4.4M fall in property, plant and equipment, and a £2.2M decrease in intangible assets. Total liabilities declined during the period as a £1.3M growth in property provisions was more than offset by a £1.5M decline in payables, a £1.6M decrease in pension liabilities and a £1M fall in deferred tax liabilities. The end result was a net tangible asset level of £22.8M, a growth of £7.6M over the past six months.

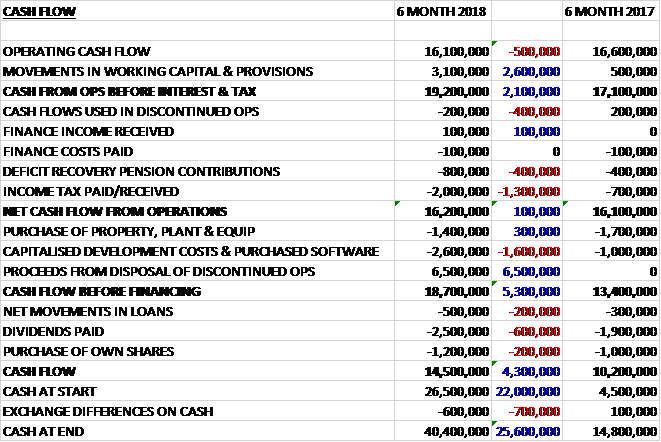

Before movements in working capital, cash profits declined by £500K to £16.1M. There was a cash inflow from working capital and after tax payments increased by £1.3M and pension deficit recovery payments increased by £400K the net cash from operations was £16.2M, a growth of £100K year on year. The group spent £1.4M on property, plant and equipment, along with £2.6M on development costs and software. This was offset by the £6.5M received from the disposal of discontinued ops to give a free cash flow of £18.7M. Of this, £2.5M was paid out in dividends, £1.2M to buy back shares and £500K to repay borrowings which meant the cash flow for the half year was £14.5M and the cash level at the period-end was £40.4M.

The profit in the Protection division was £8.7M, a growth of £1.1M year on year. Revenues declined slightly but increased at constant currency with good growth in law enforcement more than offsetting declined in military and fire.

Military revenues were 6% lower. DoD revenues were flat with higher spares sales offsetting the planned lower shipment of M50 mask systems of 79,000. The ROW order book has grown strongly in the period driven by the initial MCM100 underwater rebreather orders. The lower first half ROW revenue arose due to delivery timings being weighted to the second half.

They received orders for 100,000 M50 mask systems in the period, resulting in an order book of 70,000 systems as they enter the second half, and since the period-end they have received a further order for 24,000 systems. They continue to pursue a number of identified opportunities with the DoD and ROW military customers and anticipate further orders, both for existing products and the new product portfolio.

Law enforcement revenue grew 42% on a constant currency basis to £18.6M. This was driven by strong performances in hoods and mask systems in Europe, the Middle East and Asia as they continue to make progress converting police forces to their products. In North America they also benefited from increased sales of filters and spares to the expanding customer base. Initial sales of their Powered Air range also contributed to the growth in the period and they see the new product range as a driver for growth moving forward.

Fire revenues reduced by 6% to £7.2M as the sector experienced tougher market conditions in North America. The group expect the launch of the Magnum SCBA later in the year to upgrade the existing product offering to their customers and support the medium term outlook for revenue growth.

The profit in the Dairy division was £2.6M, a decline of £400K when compared to the first half of last year although at constant currency there was a very modest increase. Revenue grew by less than 1% at constant currency as continued growth in Precision, control and Intelligence and Farm Services was offset by the performance of Interface in North America due to tougher market conditions as a result of increased feed costs squeezing farmer margins. With the softer market conditions in North America, they will continue to focus on managing the operating costs of the business in the second half.

Interface revenue was impacted by weaker market conditions in North America following the recent feed cost increases which are expected to continue in the second half. Market conditions in Europe, Middle East and Asia Pacific remain positive reflected in a constant currency revenue growth of 9% across these regions.

The Precision, Control and Intelligence range and sales have continued to perform well across the key markets. Revenue of £4.8M grew 5% at constant currency as dairy farmers continue to invest to drive farm efficiency. Farm Services has continued to show good growth with revenue of £2.6M up 29%, reflecting the success of Cluster Exchange which saw a 23% growth in cluster points. The extension of Farm Services to include Pulsator Exchange and Tag Exchange continues to progress in line with expectations.

During the period the most significant investments have been in the further development of the Magnum Self Contained Breathing Apparatus and MCM100 underwater rebreather product ranges. In Milkrite, investment has been focused on expanding the Precision and Intelligence heavy duty product range.

In March 2018 the group disposed of Avon Engineered Fabrications, their US-based hovercraft skirt and bulk liquid storage tank business. This non-core business was included in the Protection division. It was profit-making in the period though, with a £500K profit being made. The group made a profit on disposal of £1.1M and last year it made a loss of £300K.

Going forward the board remains confident on delivery of its current year expectations.

At the current share price the shares are trading on a PE ratio of 19.6 which falls to 19.3 on the full year consensus forecast. After a 30% increase in the interim dividend the shares are yielding 1% which increases to 1.1% on the full year forecast. At the period-end the group had a net cash position of £39.1M compared to £24.7M at the year-end.

On the 30th May the group announced that Chairman David Evans sold 5,000 shares at a value of £70K.

Overall then, this has been a decent period for the group, although they have suffered from detrimental forex movements. Profits were up due to lower costs, and net assets increased. The operating cash flow also increased but this was due to working capital movements and cash profits declined. Still, a good amount of free cash was generated. The protection business was strong, driven by increased sales to law enforcement. The dairy business found going a bit tougher, however, due to the increased feed costs in North America. The group remains very cash generative but the quality is reflected in the share price, with a forward PE of 19.3 and yield of 1.1%. Not great value, but I am holding on for now.

On the 17th July the group announced the receipt of an order for 93,000 M50 mask systems worth $25M from the US DoD. This order further contributes towards building the order book for 2019 and the group continue to pursue a number of identified opportunities with the DoD and ROW military customers to build the order book further.

On the 26th July the group announced that CFO Nicholas Keveth purchased 1,383 shares at a value of £20K.

Also on the 26th July it was announced that non-executive director Chloe Ponsonby purchased 1,400 shares at a value of £20K.