The Berkeley Group is engaged in residential-led mixed use property development focusing on London and the South East of England. It has now released its final results for the year ended 2015.

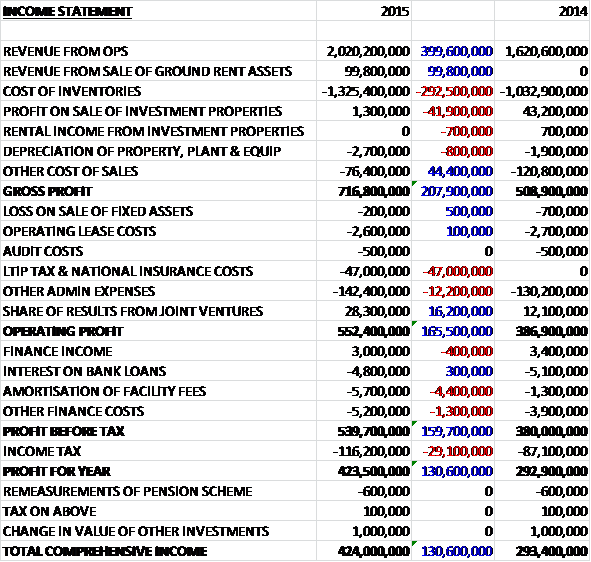

Revenues increased when compared to last year with a £399.6M growth in operating revenue and a £99.8M revenue achieved from the sale of ground rent assets which did not occur last year. Cost of inventories were up £292.5M and there was a £41.9M reduction in the profit from sales of investment properties but other cost of sales fell to give a gross profit £207.9M above that of last time. We see a £47M settlement of LTIP tax costs and a £12.2M growth in other admin costs offset by a £16.2M increase in the share of the joint venture results so that operating profit came in £165.5M ahead of 2014. There was a larger amortisation of the bank facility fees reflecting the expensing of £3.9M of un-amortised fees following the refinancing and other finance costs relating to imputed interest on land creditors also increased which meant that after a £29.1M growth in the tax charge, the profit for the year was £423.5M, a growth of £130.6M year on year.

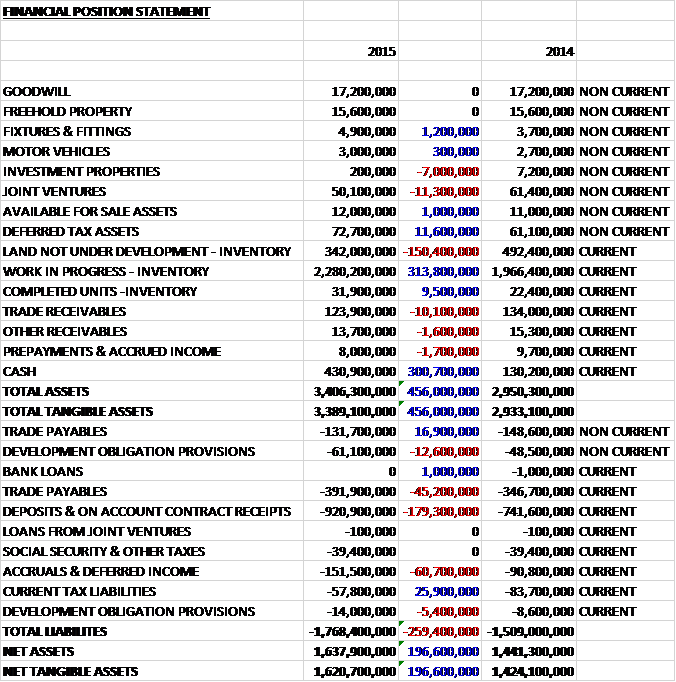

When compared to the end point of last year, total assets increased by £456M driven by a £313.8M growth in work in progress, a £300.7M increase in cash and an £11.6M increase in deferred tax assets, partially offset by a £150.4M fall in the value of land not under development, an £11.3M decrease in the value of joint ventures and a £10.1M fall in trade receivables. Total liabilities also increased during the year as a £179.3M growth in deposits on account, a £60.7M increase in accruals & deferred income, a £32.6M growth in trade payables and an £18M increase in provisions was partially offset by a £25.9M decline in current tax liabilities. The end result is a net tangible asset level of £1.620BN, an increase of £196.6M year on year.

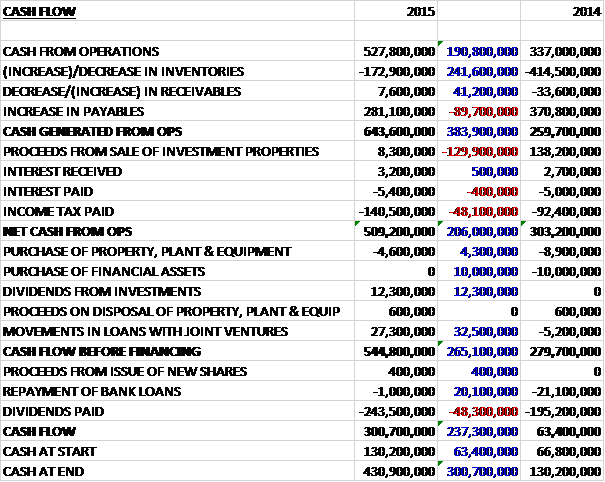

Before movements in working capital, cash profits grew by £190.8M to £527.8M. A decline in working capital, mostly as a result of an increase in payables, meant that cash generated from operations increased by £383.9M to £643.6M. There was a £129.9M fall in the proceeds from the sale of investment properties, however, and the group paid £48.1M more in tax which meant that the net cash from operations stood at £509.2M, an increase of £206M year on year. The group only spent £4.6M on property, plant and equipment so that after a £12.3M receipt of dividends and a £27.3M repayment in loans from joint ventures, there was a stonking cash flow of £544.8M before financing. After dividends were paid, the group then had a cash flow of £300.7M for the year and a cash pile of £430.9M at the year-end.

During the year the housing market returned to normal transaction levels from a high point in 2014. Domestic demand was strong in the group’s core markets of London and SE England, whilst London has continued to benefit from a stable social and political environment. The group has experienced sales price increases in line with those reported in the wider market but these have generally been matched by cost increases at a similar rate.

The group launched a number of new schemes to the market this year, from London Dock in Wapping to Smithfield Square in Hornsey and 250 City Road in Islington amongst others, all of which were marketed in the UK first and were well received by customers. The stable market has resulted in cancellation rates of 10% compared to historical levels of 15% to 20% and completed stock remains at historically low levels with 31 completed residential properties in inventories at the year-end.

Following the announcement of the formation of a joint venture with National Grid, St. William, to regenerate redundant gas works across London and the South East, the group is now working with its partner to identify sites from across its portfolio to bring through its pipeline and land holdings. This has had the potential to deliver some 7,000 plots from an initial ten sites and is a clear source of future land. One site in Battersea was already in the group’s land bank, and one further site in Rickmansworth has been added this year.

The group has secured 28 planning consents during this year, nine on schemes which did not previously have implementable planning consent and 19 revised consents. The new consents include Fitzroy Gate in Isleworth, 250 City Road in Islington, 22-29 Albert Embankment in Lambeth, Smithfield Square in Hornsey, South Quay Plaza in Docklands, and further residential schemes in Kingston, Bracknell, Barnes and Orpington. The revised consents have improved the planning position on each of the schemes on which earlier phases are already in construction, and these include a full re-plan of the third phase at Kidbrooke Village and a detailed consent on the waterfront block at Royal Arsenal Riverside which will contribute further impetus to this regeneration scheme.

Since the year end the group has acquired a resolution to grant planning at its scheme in White City for over 1,400 homes to be delivered over the next fifteen years, and a resolution to grant planning for 839 at St. William’s first scheme in Battersea.

Two new sites have been acquired unconditionally during the year, a 15,000 square foot office building in Sevenoaks and a scheme for 600 homes in Reading in the St. Edward joint venture. Three have been acquired on a conditional basis, including sites in Kingston and Winchester, as well as the second St. William site in Rickmansworth.

At the year-end, the group has 74 sites in its land holdings, of which 55 have an implementable planning consent and are in construction, a further ten have at least a resolution to grant planning but the consent is not yet implementable and seven remain in the planning process. The group’s land holdings now stand at 37,473 plots compared to 35,963 last year with an estimated gross margin of £5.272BN and an average selling price of £456K (£419K last year).

Within the £2.02BN of revenue from operations, there was £1.936BN (£1.605BN) of residential revenue, £12.3M (none) from land sales on three sites, and £71.7M (£15.6M) of commercial revenue. In all, 3,355 new homes were sold across London and SE England at an average selling price of £575K compared to 3,742 new homes at an average price of £423K last year. The increase in average selling price reflects the first completions at Ebury Square, Riverlight, Fulham Reach and One Tower Bridge, all London schemes acquired in 2009 and 2010. Last year included the disposal of 534 properties from the rental fund to M&G Investments at an average selling price of £197K and the sale of two student developments.

The revenue of £71.7M from commercial activities included the sale of some 130,000 square feet of office, retail and leisure space across a number of the group’s developments including Fulham Reach in Hammersmith, Langham Square in Putney and Royal Worcester as well as a 90,000 square foot hotel at Goodman’s Fields in Central London. The £15.6M from last year was mainly from the sale of retail space on developments including Marine Wharf in Deptford, Goodman’s Fields in Aldgate, Fulham Reach and Imperial Wharf. During the year the group also sold a portfolio of 10,000 ground rent leases across sixty sites for proceeds of £99.8M and a gross profit of £85.1M. The group has also exchanged contracts for the sale of a further portfolio of ground rent assets for £53M which is expected to be completed in the first half of 2016 and give rise to a profit on disposal of £50M.

The £47M charge with regards to the LTIP scheme is in respect of the company’s decision to settle the tax and national insurance liabilities arising from the vesting of options for the 2009 LTIP scheme, in lieu of issuing shares to this value and the intention is to do the same in respect of options next year. Of this £47M, £33.5M is in respect of prior periods and £13.5M in respect of this year.

The group’s share of the results of joint ventures was a profit of £28.3M compared to £12.1M last year which reflects a further 230 completions at 375 Kensington High Street and Stanmore Place. The reduction in investments in joint ventures from £61.4M to £50.1M reflects the distributions in the year relating to St Edward, a joint venture with Prudential. The business has three schemes currently in development at Stanmore Place, 375 Kensington High Street, and 190 Strand. 230 homes were sold during the year at an average selling price of £1.229M. Some 2,116 plots in the group’s land holdings relate to this joint venture which includes a site at Green Park in Reading which was acquired during the year. The joint venture also controls a commercial site in Westminster which has a detailed planning consent but is conditional on vacant possession and is included in the land bank.

Key challenges include the upward pressure on costs and the limited availability of skilled labour and materials in the supply chain. Another risk is the potential referendum for the UK to stay within the EU and of course the house building sector is very cyclical and come the next down-turn, these shares will be hammered considerably. Obviously another risk is the potential increase in interest rates and the effect this will have on the housing market along with regulation risk and mortgage availability.

Interestingly the group enjoys the highest customer loyalty in the housing sector and apparently is the only public company to address and measure people’s wellbeing in the places that they build with adherence to certain space standards, something that many new builds don’t seem to take into consideration. They have a net promoter score of 69.8 and some 98% of customers would recommend the group to a friend so they genuinely seem to have a differentiating focus on customer service.

During the year the group renegotiated its banking facilities. They increased their committed corporate facilities from £525M to £575M, extending the maturity date to March 2020 and have materially reduced the ongoing costs associated with the facility. It seems strange, though, that the group don’t seem to be using it – is this just some leeway for a potential downturn? A further £60M of banking facilities in St Edward Homes were cancelled during the year as they were no longer required by the joint venture.

It has to be said that I have never seen directors so highly paid as those at this company. This is mainly as a result of a LTIP scheme devised during the recession when the shares were much lower than they are now, but nevertheless, the total remuneration for Chairman and founder Tony Pidgley was £23.3M this year – ridiculous! Sean Ellis, the lowest paid director, took home an incredible £3.8M! Also, during the year the company dismissed its finance director, Nicholas Simpkin, who was put on fully paid gardening leave. Nicholas has issued legal proceedings against the company which they are defending.

Whilst earnings remain sensitive to the timing of delivery of certain key developments, the board currently expects adjusted earnings in 2016 to be similar to that of 2015 and is targeting the delivery of pre-tax profits in the region of £2BN over the next three years. This target is a result both of the group planning to deliver the London sites which were acquired between 2009 and 2013, and of continuing to benefit from the maturity of its longer term regeneration sites. The new year will see increased investment in construction ahead of this advanced profit delivery.

At the current share price, the shares trade on a PE ratio of 12.5 but this increases to 15 on next year’s consensus forecast. At the current share price the shares are yielding 5.2% which increases to 5.8% on next year’s forecast. At the year-end, the group had net cash of £430.9M compared to £129.2M at the end of last year.

Overall then, this was a very good year for the group. Profits increased strongly, net assets grew and the operating cash flow improved and provided oodles of free cash. The housing market in the SE of the country is steady and we also see the group’s land holdings grow, with an increased average plot sale price. In addition, the joint ventures have been performing strongly but it should be noted that profits this year were boosted by the sale of ground rent leases which are not going to be a permanent feature going forward.

It is nice to see that Berkley seem to have a genuinely impressive customer service ethos which should hold them in good stead but as with all potential investments, not everything here is perfect. The LTIP scheme is a bit ridiculous in my view with material amounts being spent on it and the directors getting pretty grotesque salaries. Their performance has been impressive but total remuneration of over £23M for a chairman is just too much in my view. There are also other risks here, the housebuilding industry is clearly very cyclical and come the next downturn, the shares are likely to collapse. Plus (hopefully) more short term risks include the potential of a UK exit from the EU and an increase in interest rates.

With a forward PE of 15, the shares do not look that cheap but there is plenty of net cash on the balance sheet and the dividend yield of 5.2% is very nice to have. The question has to be though, are they worth the risk and the answer to that is probably dependent on when you see the next recession hitting the UK. I am thinking about taking a position here.