Berkeley Homes has now released its prelim results for the year ended 2016.

Revenues declined when compared to last year with a £26.1M fall in revenues from operations and a £46.4M decline in revenue from the sale of ground rents. Cost of sales also fell during the year to give a gross profit £15.1M below that of last year. The group also made a £2.8M profit from the sale of fixed assets and £8.2M more than last year from the joint ventures but share based payments increased by £26.1M to an astonishing £28.8M relating to the acceleration of the accounting charge for the modification of various LTIPs following changes to the dividend programme during the year. After other operating expenses increased by £15.8M, the operating profit fell by £14M. There was a £2M fall in bank loan interest and a £2.6M decrease in facility fee amortisation but income tax charges increased by £10.6M to give a profit for the year of £404.1M, a decline of £19.4M year on year.

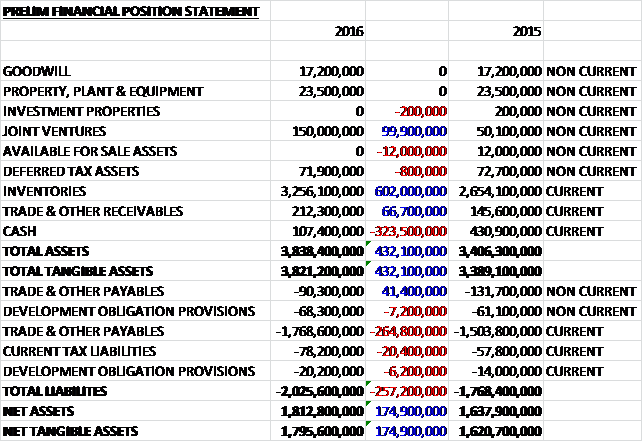

When compared to the end point of last year, total assets increased by £432.1M driven by a £602M growth in inventories, a £99.9M increase in investments in joint ventures reflecting funding into the St. William joint venture and profits generated in St. Edward but not distributed, and a £66.7M growth in receivables, partially offset by a £323.5M decline in cash and a £12M decrease in available for sale assets. Total liabilities also increased during the year due to a £223.4M increase in payables due to a growth in on account receipts from customers, a £20.4M growth in current tax liabilities and a £13.4M increase in development obligation provisions. The end result is a net tangible asset level of £1.797BN, a growth of £174.9M year on year.

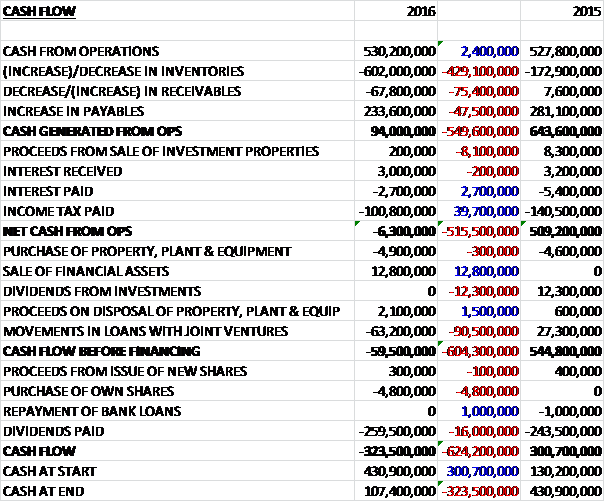

Before movements in working capital, cash profits increased by £2.4M to £530.2M. There was a large cash outflow from working capital, however, with a £602M cash outflow on inventories. There was an £8.1M decline in proceeds from the sale of investment properties and after tax payments fell by £39.7M, there was a net cash outflow from operations of £6.3M, a detrimental movement of £515.5M year on year. The group sold £12.8M of financial assets but invested £63.2M in loans to joint ventures which meant that before financing, there was a cash outflow of £59.5M. The group also spent £259.5M on dividends to give a cash outflow for the year of £323.5M and a cash level of £107.4M at the year-end.

During the year the group sold 3,776 homes at an average selling price of £515K which corresponds to 3,355 sold at £575K last year, reflecting the mix of properties sold with the group completing two student developments in the year. They made gross profit of £650.7M from operations, an increase of £19M year on year and £51M profit on the sale of ground rent assets, a decline of £34.1M. Revenue of £26.6M from commercial activities was down £45.1M on last year and included the sale of 119,000 square feet of office, retail and leisure space across a number of developments with last year benefiting from an 89,000 square foot hotel at Goldman’s Fields.

The group acquired 12 new sites, encompassing 8,600 plots, secured nine new planning consents and 21 revised planning consents. This has meant the land holdings have risen to 42,858 plots with an estimated future gross margin of £6.1BN, this is up from the 37,473 plots at £5.3BN a year ago. The new sites include a range from outside London in locations such as Ascot, Wokingham and Southwater, and in London at Cockfosters, Black Heath and Paddington, along with the large, complex and long-term regeneration sites of Stephenson Street, the Oval Gasworks, and within St. William, the former gasworks at Fulham, Hornsey, Watford and Borehamwood. Five of the sites have been acquired unconditionally and seven are contracted on a subject to planning or vacant possession basis.

The new planning consents include White City for over 1,450 homes to be delivered over the next fifteen years, St. William’s scheme in Battersea, West End Green in Paddington and on other developments in Southwater, Taplow, Winchester, Latchmere, Kingston and Cranleigh, some of which remain subject to finalisation of section 106 agreements.

The revised consents include the securing of an improved masterplan at Southall along with a resolution to grant detailed planning for the first phase of this long-term regeneration scheme. This phase will comprise some 620 units over nine blocks with 1.4 acres of public parkland. The affordable housing will be delivered ahead of the private units. The group’s long term regeneration schemes now comprise Royal Arsenal, Kidbrooke Village, Woodberry Down, Beaufort Park, Southall and Stephenson Street which was acquired in the year. This latter site comprises some 27 acres adjacent to West Ham station.

The group’s land holdings at the year-end are across 77 sites, of which 56 have an implementable planning consent and are in construction, a further 7 have at least a resolution to grant planning and 14 remain in the planning process, eleven of which are subject to conditional contracts.

During Q4 the group launched a new design concept called the Urban House. This enables twice as many homes to be built on a site compared to traditional terraced housing. The houses are three storeys and the back garden is replaced with a private roof garden. The first 22 homes of this prototype have been built on two streets at Kidbrooke Village and others are under construction at Green Park Village in Reading. The group believes that these houses will offer local authorities a new way of providing high density family homes and the increase in density will make smaller sites viable for residential development.

As part of the estate regeneration programme at Woodberry Down, the group have worked with the London Wildlife Trust to restore an eleven hectare wetland and at One Tower Bridge they are building a 900 seat theatre. In Bath, they recently completed 307 student rooms for Bath Spa University which won a Royal Town Planning Institute Award for Planning Excellence.

St. Edward has four schemes currently in development at Stanmore Place, Kensington High Street, The Strand and, launched in H1, a new site at Green Park in Reading. 240 homes were sold in the year at an average selling price of £1,329,000. Some 1,868 plots in the group’s land holdings relate to St. Edward schemes and the business is continuing to identify opportunities in which to add value to the joint venture, controlling a commercial site in Westminster which has a detailed planning consent but will not move into development until the premises are vacated by the current tenant. 3,599 plots in the land bank relate to St. William schemes and the group is working closely with National Grid to identify sites from across its portfolio to bring into its land holdings. Of the 12 new sites acquired by the group during the year, four were through this joint venture.

Over the course of the year the housing market has remained stable with forward sales increasing by 10% to £3.25BN, reflecting a greater value of new properties exchanged in the period compared to those taken to profit in the year. The forward sales have now peaked as the group enters a period of enhanced delivery over the next two years, over which time the forward sales and customer deposits are likely to reduce with customers buying later in the development cycle as market conditions normalise.

During last year the group dismissed finance director, Nicholas Simpkin, who issued legal proceedings in the employment tribunal against the company. They are being defended by the company with the assistance of external professional advisors.

The upcoming EU referendum is clearly a major headwind here with an out vote likely to severely affect the market. On the other hand, the group are encouraged by the noises coming out of the new mayoral administration in London which has apparently shown some welcome signs of adopting an approach to delivery which is “ambitious and pragmatic”.

There is a robust underlying demand but uncertainty is impacting current transaction levels with reservations over five months to May down 20% on reduced new launches in the run up to the EU Referendum. This had a more distinct impact on the higher end of the market which has also been affected by increased transaction taxes and the policy shift against buy-to-let investors. The group continue to achieve sales prices ahead of their business plan with price inflation remaining for properties of less than £1.25M where demand is more robust. They are able to absorb the increased cost of transaction taxes above this level in their pricing, however. New sales activity is now focused on the period beyond 2017/2018 with a number of new launches planned for later in the year.

It is of some concern that after such strong market conditions in the industry, transaction levels in both the second hand and new homes market have not increased to the levels hoped for at this stage in the cycle.

There is cash due over the next three years on forward sales of £3.25BN, however, and the board are maintaining their earnings guidance for the three years to 2018 despite the fact that the scale of the key regeneration schemes from which they expect to generate these earnings makes the delivery of profit in specific annual periods sensitive to timing.

At the current share price the shares trade on a PE ratio of 12.7 which falls to 8.7 on next year’s consensus forecast. At the end of the year the group had a net cash position of £107.4M compared to £430.9M at the end of last year. After an interim dividend of £1 per share was declared, the shares are yielding 6.2% which expected to remain the same next year.

So, this is an interesting one. It has been a bit of a mixed year for the group. Profits fell but it seems as though this can be attributed to a reduction in ground rent asset sales rather than the underlying trading as a fall in the value of homes sold was offset by an increase in numbers of sales. Net assets increased but there was an operating cash outflow due to a huge investment in inventories so no free cash was generated, although cash profits were up.

The shares look very cheap with a forward PE of just 8.7 and an impressive yield of 6.2% but now that the UK has voted to leave the EU, there will be a lot of uncertainty around the market so I don’t feel as though now is the time to invest here – perhaps when share prices have stabilised this could be a bargain though?

Following the share price crash after the Brexit vote, there has been a spate of director purchases. Non-executive Glyn Barker has purchased 5,000 shares at a value of £119K; chairman Tony Pidgley has purchased 35,061 shares at a value of £796K; and veronica Wadley and Andy Myers, both non-execs, purchased 1,000 shares each at a value of about £23.5K. The directors now own 15,042; 6,948,916; 7.500; and 3,000 shares respectively.

On the 6th September the group released an update covering the period from May to August. The group entered the year with forward sales of £3.25BN and future estimated land bank gross margin of £6.15BN. The board re-iterates its guidance for the delivery of £2BN of pre-tax profit over the three years ending 2018 and they expect to remain ungeared at the half year point.

Reservations in the first five months of the year were 20% lower than in the same period of 2016 as customers adjusted to higher property taxes and uncertainty surrounding the Brexit vote with the group deferring the release of new product onto the market. After a hiatus in June and July, August returned to these levels, some 20% below that of last year, reflecting the lower levels of available product, as well as the broader market conditions. Throughout the year, site visitor numbers and enquiries have been at a similar level to last year, however, demonstrating the strength of underlying demand, although customers are taking longer to commit. Pricing has remained resilient and above business plan levels with reservation cancellation rates at normal levels, following a temporary and expected increase after the Brexit vote.

The group has been selective in the land market, acquiring just two sites in the period, both unconditionally, with planning advanced on a number of existing sites. It is clear that government policy has had a negative effect on the capital. Transaction taxes are now restricting the pace of supply of new homes in London and the very high rates of the Community Infrastructure Levy adopted by local authorities now pose a significant threat to development viability.

Overall though, the group is well positioned to deliver its earnings and dividend guidance and optimise shareholder returns in the current market conditions. It is apparent from this update that the group has suffered a couple of months of lower trade around the Brexit vote but the real issue at the moment seems to be the slow-down in the London market related to taxation issues. Given how the group is skewed towards London, this is a bit of an issue and I am not sure this is a sensible investment at the moment.

On the 16th September the group announced that non-executive director Adrian Li purchased 10,000 shares at a value of £257K.