Berkeley group has now released their final results for the year ended 2017.

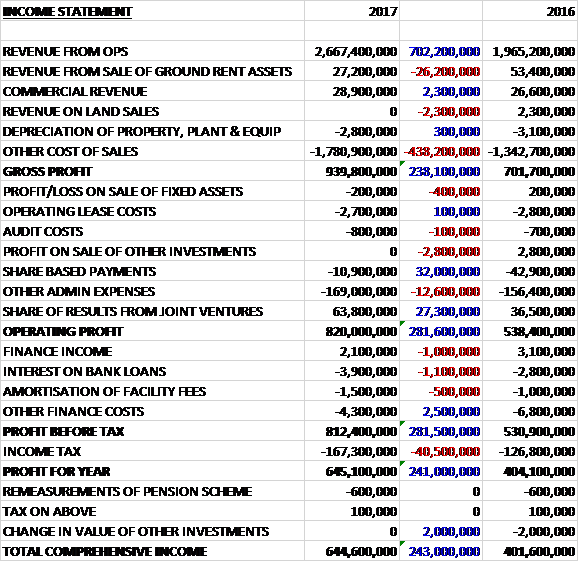

Revenues from the sale of ground rents reduced by £26.2M and revenue from land sales fell by £2.3M but revenue from operations increased by £702.2M and commercial revenue was up £2.3M. cost of sales grew by £437.9M which meant that the gross profit was £238.1M higher. Share based payments declined by £32M and there was a £27.3M increase in the contribution from joint ventures but there was no sale of investments, which made £2.8M last time, and other admin expenses were up £12.6M to give an operating profit £281.6M higher. Finance income was down £1M, there was a £1.1M increase in bank loan interest and a £500K growth in the amortisation of facility fees but other finance costs were down £2.5M and after tax charges increased by £40.5M there was a profit of £645.1M for the year, a growth of £241M year on year.

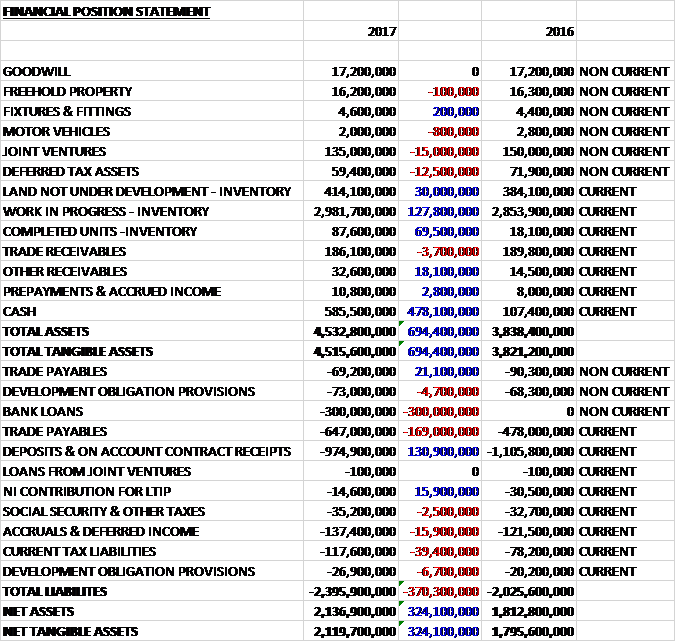

When compared to the end point of last year, total assets increased by £694.4M, driven by a £478.1M growth in cash, a £127.8M increase in work in progress, a £69.5M growth in completed units, a £30M increase in land not under development and an £18.1M growth in other receivables, partially offset by a £15M decline in joint ventures and a £12.5M decrease in deferred tax assets. Total liabilities also increased during the year as a £130.9M decline in deposits on account and a £21.1M fall in trade payables were more than offset by a £300M increase in bank loans, a £169M growth in trade payables, a £39.4M increase in current tax liabilities and a £15.9M increase in accruals and deferred income. The end result was a net tangible asset level of £2.119BN, a growth of £324.1M year on year.

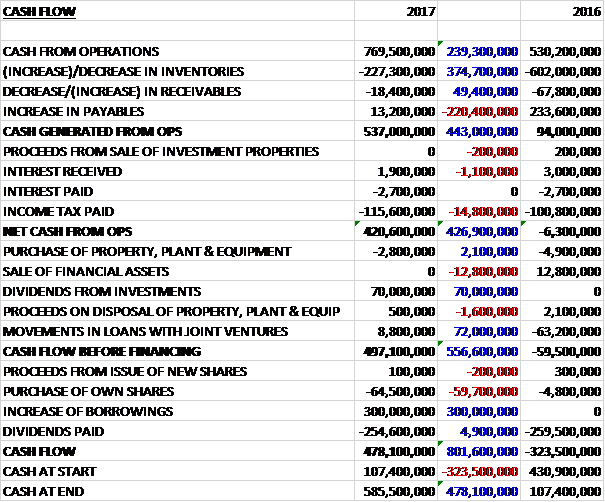

Before movements in working capital, cash profits increased by £239.3M to £769.5M. There was a cash outflow from working capital but this was less than last year and after tax payments increased by £14.8M the net cash from operations was £420.6M, a growth of £426.9M year on year. The group spent just £2.8M on capex and received £70M in dividends from St. Edward, along with the receipt of £8.8M in loans from joint ventures to give a free cash flow of £497.1M. The group then spent £64.5M on their own shares and paid out £254.6M in dividends but covered this with a £300M increase in borrowings to give a cash flow of £478.1M and a cash level of £585.5M at the year-end.

Overall the group sold 3,905 homes at an average selling price of £675K per home compared to 3,776 at £515K last year. They have acquired 16 new sites, of which nine are on a conditional basis, totalling some 7,200 plots. They have also secured ten new planning consents and over 30 revised consents. This activity has seen their holdings rise to 46,351 plots with an estimated gross margin of £6.4M, up from 42,858 plots and £6.1BN a year ago. Since the year-end they have acquired their first site in St. Joseph in Birmingham where they plan to develop around 400 new homes.

Taking the year as a whole. Including the period around the Brexit vote, the value of reservations is 25% lower than last year but this decline has now fully reversed with the return to more stable conditions. Sales continue to be split broadly evenly between owner occupiers and investors and include 157 Help to Buy reservations. Build costs have increased at a similar rate to last year, around 6%, with currency movements impacting materials pricing. There is a recognised skills gap in the UK construction workforce and it is hard to predict how build costs will be affected by Brexit as about half of London’s site labour comes from the EU.

The revenue of £28.9M from commercial activities included the sale of 85,000 sq foot of office, retail and leisure space across a number of the group’s developments including Royal Wells Park in Kent and Kew Bridge, Riverlight, Chelsea Creek, Fulham Reach and Goodman’s Fields in London.

There are a number of factors that resulted in the net £22.3M reduction in share scheme charges, which includes the associated employer’s NI costs. The company cash settled the tax and NI liabilities arising on the vesting of options for participants in the 2011 LTIP in September in lieu of issuing shares. This was more than offset by the effect of the introduction of the caps on the Executive Director remuneration and the prior year included the costs associated with the second tranche of Part B of the 2009 LTIP which vested in April 2016 which was also cash settled for tax and NI.

The increase in the share of joint venture profit reflects the first completions during the current year at 190 Strand and Green Park in Reading, as well as further completions at 375 Kensington High Street and Stanmore Place within St. Edward, and pre-development costs within St. William in the early stages of the joint venture.

St. Edward currently has four schemes in development at Stanmore Place, Kensington High Street, The Strand and Green Park in Reading. 251 homes were sold in the year at an average selling price of £1,332,000. 2,152 plots in the group’s land holdings relate to St. Edward schemes and during the year a resolution to grant consent for a development in Wallingford has been obtained. The site has come through the strategic land holdings and is now included in the land bank. St. Edward also controls a commercial site in Westminster which has a detailed planning consent but will not move into development until the premises are vacated by the current tenant.

6,459 plots (last year: 3,599) in the group’s land holdings relate to St. William schemes, with five new schemes contracted in the year. During the year the production started on St. William’s Prince of Wales Drive development in Battersea. The group continues to work with National Grid to identify sites from across its portfolio to bring into its land holdings. In total there are now eleven St. William developments included in the land holding.

Excluding joint ventures, ten new sites have been added to the land bank in the year. These include six developments in the SE: Farnham, Leatherhead and Cranleigh in Surrey; Royal Tunbridge Wells in Kent; Rudgwick in West Sussex and Sunningdale in Berkshire. In London they have acquired two sites unconditionally: a 21 acre Northfields industrial estate where they are preparing a planning application and a site in Ealing adjacent to their existing Dickens Yard development. In addition, they have conditionally acquired a site on Wood Lane to the west of the existing White City development, and a further conditional site in Paddington.

The group’s land holdings now comprise 90 sites, which is up from 77 a year ago. Of these, 58 have an implementable planning consent and are in construction and a further 14 have at least a resolution to grant planning but the consent is not year implementable; typically due to practical technical constraints and challenges surrounding vacant possession, CP requirements or utilities provision. The remaining 18 sites are in the planning process with 15 of these subject to conditional contracts.

The housing market has stabilised in London and the South East following the disruption either side of the Brexit vote but there are a number of headwinds facing the market. Brexit and wider global macro instability will likely result in constrained investment levels. At the same time, the headwinds from changes in recent years to stamp duty and mortgage interest deductability coupled with the planning environment’s increasing demands from Affordable housing, CIL, Section 106 obligations and review mechanisms are resulting in reduced levels of new housing starts in London. For the group this leads to greater uncertainty around the timing of delivery of homes from the land bank but notwithstanding these issues, the forward sales position and land bank provide sufficient visibility to reiterate the previous guidance of delivering at £3BN of pre-tax profit in the five years beginning 2016 assuming prevailing market conditions persist.

At the current share price the shares are trading on a PE ratio of 8 which remains the same on next year’s consensus forecast. After a reduction in the latest dividend the shares are yielding 5.1% which increases to 5.5% on next year’s forecast. At the year-end the group had a net cash position of £285.5M compared to £107.4M at the end of last year.

Overall then this has been another strong year for the group. Profits increased, net assets grew and the operating cash flow increased, with a decent amount of free cash flow being generated. The group did increase borrowings at the same time as dividends though, which is not something I am a big fan of. The increase in profit seems to be mostly down to an increase in the average value of home sold, which is down to mix and may not be repeated going forward and there are certainly some headwinds such as continued uncertainty over Brexit, increased build costs and the stamp duty changes.

All in all, though I think the forward PE of 8 and yield of 5.5% probably takes this into account. If I wasn’t already invested in some housebuilders, I’d probably be interested in buying some shares here.

On the 6th September the group released a trading update covering the four months to the end of August where they stated that they continued to trade in line with management’s expectations. The London market continues to be adversely impacted by uncertainty around Brexit and the changes in recent years to SDLT which has been partially offset by good mortgage availability at low interest rates, and favourable currency exchange rates. On the supply side, the planning environment remains challenging and new construction starts in London remain 30% lower than 2015.

On the 8th September Chairman Anthony Pidgley sold 750,000 shares at a value of £26.8M! Also, CEO Robert Perrins, sold 500,000 shares at a value of £17.9M. This is not a ringing endorsement of prospects going forward!

On the 10th October the group announced that non-executive director Alison Nimmo sold 2,000 shares at a value of £755K.