Braemar Shipping has now released its final results for the year ended 2016.

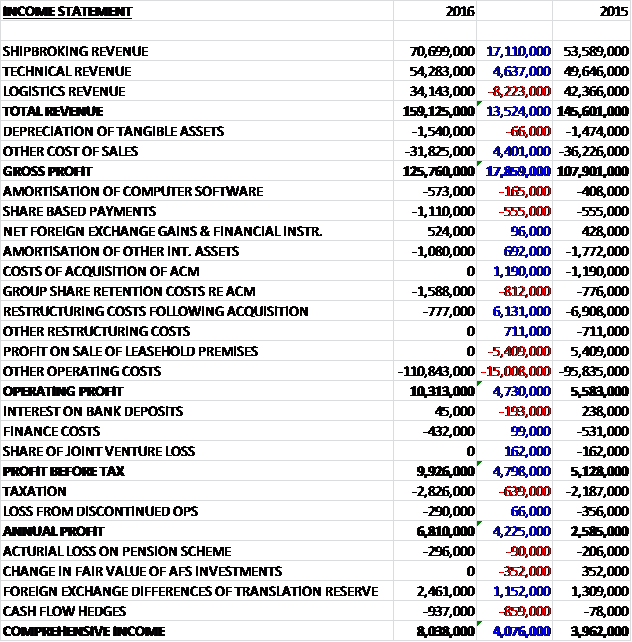

Revenues increased when compared to last year as an £8.2M decline in logistics revenue due to a fall in freight forwarding was more than offset by a £17.1M growth in shipbroking revenue and a £4.6M increase in technical revenue. Cost of sales declined year on year which gave a gross profit £17.9M above that of last year. Share based payments increased by £555K but this was offset by a fall in amortisation. Other underlying operating costs increased by £15M, however. We then see a reduction in non-underlying costs as the lack of the £5.4M profit on last year’s building sale and an £812K increase in share retention costs relating to the ACM acquisition was more than offset by a £6.1M reduction in other acquisition costs and the lack of £711K of restructuring costs that occurred last year to give an operating profit £4.7M ahead. There was a small increase in finance costs and after the lack of losses from discontinued operations was more than offset by increased tax charges the profit for the year came in at £6.8M, a growth of £4.2M year on year.

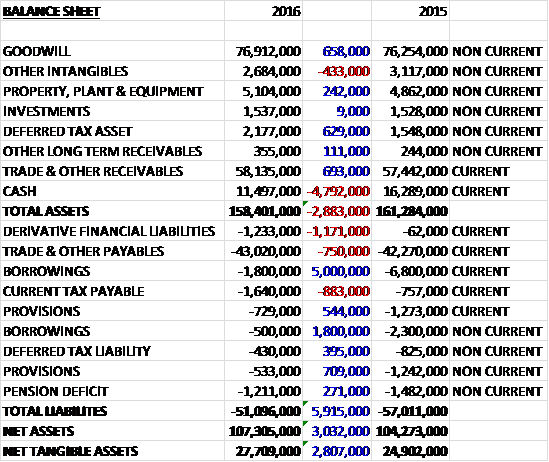

When compared to the end point of last year, total assets declined by £2.9M driven by a £4.8M fall in cash levels and a £433K decrease in other intangible assets, partially offset by a £693K growth in receivables, a £658K increase in goodwill and a £629K growth in deferred tax assets. Total liabilities also decreased during the year as a £1.2M increase in derivative financial liabilities, an £883K growth in current tax payables and a £750K increase in payables were more than offset by a £6.8M fall in borrowings and a £1.3M decline in provisions. The end result was a net tangible asset level of £27.7M, an increase of £2.8M year on year.

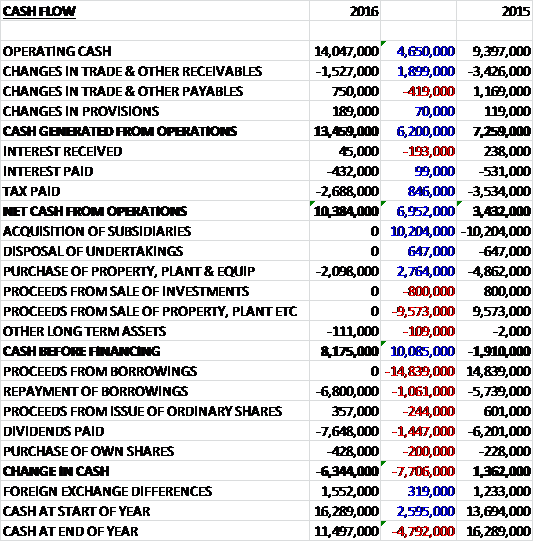

Before movements in working capital, cash profits increased by £4.7M to £14M. There was a small cash outflow from working capital, although this was lower than last year and after less tax was paid out too, the net cash from operations came in at £10.4M, a growth of £7M year on year. The group spent just £2.1M on capex to give a decent free cash flow of £8.2M. This only just covered the £7.6M spent on dividends, however, so the £6.8M repayment of borrowings meant that there was a cash outflow of £6.3M for the year to give a cash level of £11.5M at the year-end. I think I would have preferred to see a dividend reduction or holiday whilst the group acquitted ACM as pretty much all of the cash is going out in dividends.

The underlying operating profit in the shipbroking division was £9.7M, a growth of £4.1M year on year reflecting the ACM shipbroking merger. The tanker teams delivered a strong performance driven by increased oil production which stimulated demand for tankers and served to increase freight rates to levels not experienced since 2008.

Crude oil trade surged during the year as refineries increased activity to meet demand for transport fuels and petrochemical feedstock. This increased consumption of oil and the demand for seaborne crude particularly stimulated the VLCC market. The global rise in supply of oil led to increased competition for tonnage which was further enhanced as Far Eastern countries diversified their crude intake from the Middle East to include the Atlantic Basin producers, thus increasing tonne miles and keeping freight rates strong. The rise in supply also allowed contangos to develop which created an incentive for oil traders to store oil, increasing the levels of land-based storage and leading to some discharge delays and a reduction in available tonnage.

Despite China’s economic slowdown, it continued to fill its strategic petroleum reserves. The market also benefited from relatively low growth in the global tanker fleet with a small number of new ships coming into the market. Ship owners also chose to defer demolition of other vessels to capitalise on the strong freight rates, however. The strong spot market had a positive effect on the long term period charter market and the freight futures market and the group’s teams were able to help clients in managing their exposure to volatile freight markets.

The fall in oil prices also boosted clean product demand globally, particularly in developing countries that lacked the refining infrastructure to meet their own product needs. Having started 2014 significantly underutilised, the world’s refineries were able to meet this new demand and this rising demand was supported by rising average voyage duration.

The market in the coming year looks to remain uncertain. Low crude oil prices and longer voyage distances are expected to continue which may drive further growth in demand, but this could be offset by the effect of the delivery of new ships and an unexpected low level of demolition. With the lifting of sanctions against Iran, more Iranian crude oil volumes are expected but the effect on the market is unclear and may be offset by the utilisation or Iranian-owned crude tankers in the international market.

Specialised Tankers performed well and delivered growth. The LNG and LPG markets have experienced overall fleet growth during recent year, with investment in VLGCs leading expansion. This growth in fleet sixe has generated an oversupply of freight against a lack of world-wide demand which has resulted in low rates in the spot market and a diminishing need for time charters.

This year was a tough one for the offshore business with exploration activity significantly curtailed as major oil companies sought cost reductions. Reduced exploration activity led to decreased demand for vessels while supply increased as time charter contracts came to an end resulting in a reduction in spot rates. It is likely that these market conditions will continue until there is a period of higher and more stable oil prices stimulating new exploration activity. Against this challenging backdrop, the offshore team has still managed to deliver a profitable performance.

Despite increased transaction volumes, the year was one of the poorest dry bulk freight markets on record due to the oversupply of tonnage combined with weaker commodity demand. This was largely driven by the slowdown in the growth rate in China where iron ore and coal demand remains a significant influence on the Capesize market and cape rates reached lows not experienced since the mid-1980s.

Going into the coming year, the projected volume of new ships coming on to the market is expected to put further pressure on the current imbalance between oversupply of tonnage and dry bulk demand. The full unwind of excess supply is likely to take some time and an increase in layup and demolition for the older vessels will be needed to correct the imbalance. In recent weeks freight rates have recovered somewhat, as measured by the increase in the Baltic Dry Index from its historic low in February, and the group are seeing increasing interest in investment in the sector. Nonetheless, market weakness presents opportunities to build the group’s business and they are selectively hiring experienced brokers to build their global reach in the Dry Bulk sector.

The Sales and Purchase team achieved a strong performance with second hand activity in the dry cargo market particularly strong. This was predominantly driven by the oversupply of tonnage and pressure on ship owners to sell. The opposite was true in the tanker market, however, as higher charter rates limited owners desire to sell vessels. The board expect that increased regulation will lead to more investment in fleet renewal and an acceleration of demolition of certain ships which will be replaced with new designs. The timing of this activity is currently uncertain, however.

The underlying operating profit in the Technical business was £5.2M, a decline of £1.1M when compared to last year reflecting margin pressure and lower activity in the offshore market. Revenues in the division actually increased mainly as a result of strong growth in Braemar Engineering.

At Braemer Offshore the fall in the oil price resulted in markedly lower exploration and construction activities in the offshore energy sector as oil companies seek to reduce their own costs. A number of forecast large projects have either been shelved or delayed and many existing projects have been scaled down. Despite the challenging market environment, the business performed relatively well due to a proactive approach to retain existing business and by expanding its service offering.

Braemar Engineering continued to benefit from its market leading position in the LNG sector and reported a strong result in the year based on both marine and shore-based LNG consulting for long term investment programmes. The team in the UK progressed with a major three year project for the design, site supervision and crew training for six LNG carrier newbuildings. The project has now delivered five of the six vessels with the final vessel due for completion in mid-2016. The office in Houston has also seen solid growth from its involvement in a significant project aimed at supplying LNG to vessels for use as a bunker fuel. At the end of 2015, they announced their exclusive involvement in the development of a new cost-effective technology for the containment of LNG.

Braemar Adjusting was also affected by reduced activity in the oil and gas sector. Output from the four US shale basins declined with construction projects and major field development being postponed or experiencing significant regulatory delay. The active worldwide drilling fleet also reduced significantly during the last year, impacting all oil and gas service industries.

Over the last few years, however, management took several strategic decisions which have helped build and shelter the business. These were to establish a strong presence in the Middle East, expand North American operations and to diversify the business to include refining, petrochemical, power and mining as well as upstream oil and gas. The business continues to recruit and develop staff and focus on growing its market share through the current market cycle to position the business for the future.

Braemar incorporating the Salvage Association performed well in the year against a backdrop of fewer casualty claims. Although the number of surveys undertaken was lower than the previous year and increase in the number of consultancy assignments, project cargo surveys and complex Hull and Machinery cases contributed to a higher level of revenue. This increase reflects the group’s desire to expand the business into new areas of marine consultancy. There was an improvement in the Middle East and Americas offset by lower level activity in SE Asia where trading conditions are challenging.

Despite the challenges faced in most marine and offshore sectors, Braemar Howells operated at a similar activity level to the prior year and achieved a higher operating profit due to cost savings flowing from a restructuring at the end of the previous year. The results benefited from a flowing from a number of projects including a project to handle bitumen and the removal of the wreck of a vessel of the Pembrokeshire coast.

The underlying operating profit in the Logistics business was £1.6M, a fall of £698K when compared to 2015 largely due to the set-up costs of their new office in Houston and the lead tome to the start of new contracts. The profitability of the freight forwarding and bespoke projects departments was also affected by delays to specific infrastructure projects in the UK.

Cory Brothers had a challenging year reflecting the tough ship agency and logistics markets. Their strategy has been to focus on higher value work together with geographic expansion into European and US markets. In the Port Agency division, the global hub business continued to grow through their customer base. The underlying UK port agency market has been difficult, but their market share has increased and ship numbers have been maintained. Markets continue to be challenging but there are signs of improvement in 2016. The group are seeking to build their UK market share in the coming year as well as continuing to growth the global hub business and their presence in North America.

Cory logistics revenue fell during the year due to delays in major infrastructure project cargoes and the impact of lower activity in the oil and gas markets. They were able to sustain their position in key business areas through growth in new services as well as the existing contract business. This was achieved despite a market backdrop of volatile freight rates. The introduction of new logistics teams in Houston, Atlanta and Singapore have provided new opportunities of growth.

The US dollar exchange rate relative to Sterling moved by 10% in the year. A significant proportion of the group’s revenue is earned in US dollars and the movement of the exchange rate has had a positive impact on earnings. The group has mitigated the full impact of this movement, however.

The group has new financing arrangements of up to £30M with HSBC to provide flexibility for future acquisitions so I would have thought something has already been identified.

The total shipbroking forward order book was about $49M, of which $26M relates to the coming year. The board anticipate that the group’s markets will continue to experience volatility and uncertainty and their expectations for the coming year is for a broadly similar activity level overall.

At the current share price the shares trade on a hefty PE ratio of 21.3 which reduces to 13 on next year’s consensus forecast. After the dividend remained the same, the shares are yielding 5.8% which remains the same for next year too. At the year end the group had a net cash position of £9.2M compared to £7.2M at the end of last year.

Overall then this has been a mixed year for the group. Profit was up, although I suspect this was mainly due to the contribution from ACM. Net assets increased and operating cash flow also grew, with a decent amount of free cash being generated. Unfortunately this only just covered the dividends and I think progress has been hampered here somewhat by the high level of pay outs. The shipbroking business performed well as lower offshore and dry bulk activity was more than offset by growth in tankers due to the increase in demand for oil. The Technical business saw profits decline due to lower offshore and adjusting activity following the slow-down of the oil and gas market.

The logistics division performed poorly, being affected by lower oil price, a decrease in freight forwarding, not helped by the delay in some UK infrastructure projects and the cost of the new Houston office. Going forward, the logistics division is expected to show some improvement but I am not sure about the technical division as the large LNG tanker project is coming to an end, and who knows what’s ahead for shipbroking. Overall, the board expect the next year to be broadly in line with this one and with net cash on the books, a forward PE of 13 and yield of 5.8% these shares are probably fairly valued.

On the 30th June the group released a trading update and as anticipated, market conditions have continued to be challenging. The board do not believe that demand for their services will be materially impacted by the Brexit vote and the associated market volatility but there may be second order economic effects that are difficult to foresee at this time. At present, they do not believe that the referendum result will affect their long term strategy.

Trading for Q1 in the shipbroking division followed the wider market patterns. The tanker markets have continued to experience high trading volumes as a result of increased worldwide oil production and refining activity but as expected, tanker freight rates have been lower. The sale and purchase desk remains good, with similar levels of activity to the prior year. The dry cargo market continues to suffer from a surplus of tonnage and a slow-down in demand and while the volume or transactions remains good, the rates remain low. The offshore desk remains weak due to low activity levels in the sector. The board expect the difficulties in these markets to take some time to correct and they will continue to ensure that they are appropriately structured to respond to these market conditions.

The performance of the technical division was behind the first quarter of last year. In particular, Braemar Offshore and Braemar Engineering are suffering the consequence of project delays and reduced activity which are currently impacting most service providers to the energy sector. The ship agency business started the year well as a result of new client business and an active tanker market. Although this was partially offset by a slower freight forwarding result, overall divisional performance is in line with board expectations.

Overall the short term outlook remains difficult and it looks as though the group is looking for another acquisition as its underlying business doesn’t seem to be growing at the moment – I remain uninvested but interested!

On the 30th August the group released a trading update. In shipbroking, over the summer tanker markets have seen both lower activity levels and freight rates which is resulting in reduced revenues. While the group expected the tanker market to soften after the high levels experienced last year, there has been a market slowdown. In the dry cargo markets, despite healthy demand and good transaction volumes, overcapacity continues to suppress freight rates. Accordingly the group have put in place a programme to reduce their costs in this area and ensure they are appropriately structured.

The sale and purchase and offshore desks continue to perform in line with expectations, with similar levels of activity to the prior year. In addition, the US dollar earnings will benefit from the weakness of sterling if the exchange rate is sustained at current levels; but the full beneficial impact will be felt in the next year due to the rolling hedging policy.

In the Technical division, to respond to the tough market conditions, the group have already made a number of senior management changes in the Braemar Technical business. The new leadership team have implemented a restructuring programme to reduce costs, create regional hubs with responsibility for division-wide service delivery, and improve the utilisation of the professional staff. This has particularly been focused on engineering services and Asia-related businesses which are most exposed to reduced industry activity. The logistics division is performing well and in line with board expectations.

While results for the current year will be materially lower than 2016, the structural management changes and cost reduction measures put in place will result in an improvement to business performance. Overall though, things seem to be tough here and I am not rushing to buy back in.