Braemar Shipping has now released their final results for the year ended 2017.

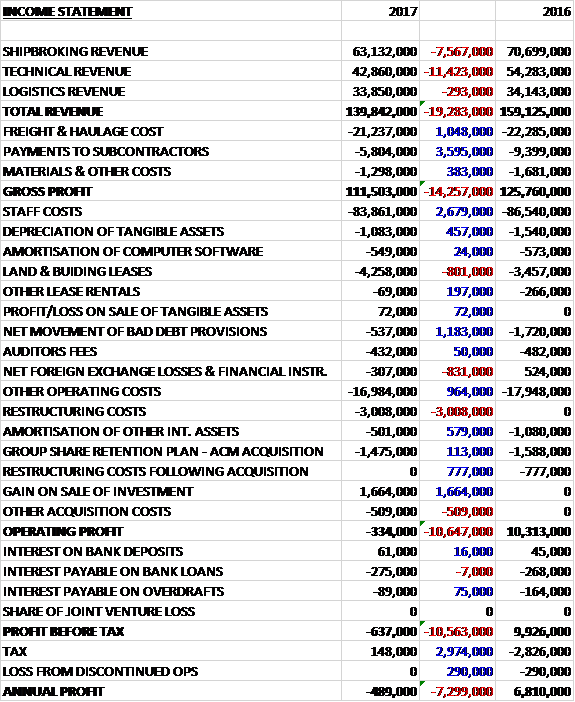

Revenues declined when compared to last year due to a £7.6M decrease in shipbroking revenue and an £11.4M fall in technical revenue. Freight and haulage costs were down £1M, payments to subcontractors decreased by £3.6M and materials costs fell by £383K to give a gross profit £14.3M below that of last year. We then see a £2.7M decline in staff costs, a £457K decrease in depreciation, a £1.2M fall in bad debt provisions and a £964K decrease in other operating costs, partially offset by an £801K growth in land and building leases and an £831K negative forex swing. There was also a £2.2M growth in restructuring costs and a £509K increase in other acquisition costs but amortisation was down £579K and there was a £1.7M gain on the sale of an investment which meant that the group made an operating loss, a negative swing of £10.6M. Interest costs were slightly lower and tax charges saw a £3M positive swing, all of which gave an annual loss of £489K, a negative swing of £7.3M year on year.

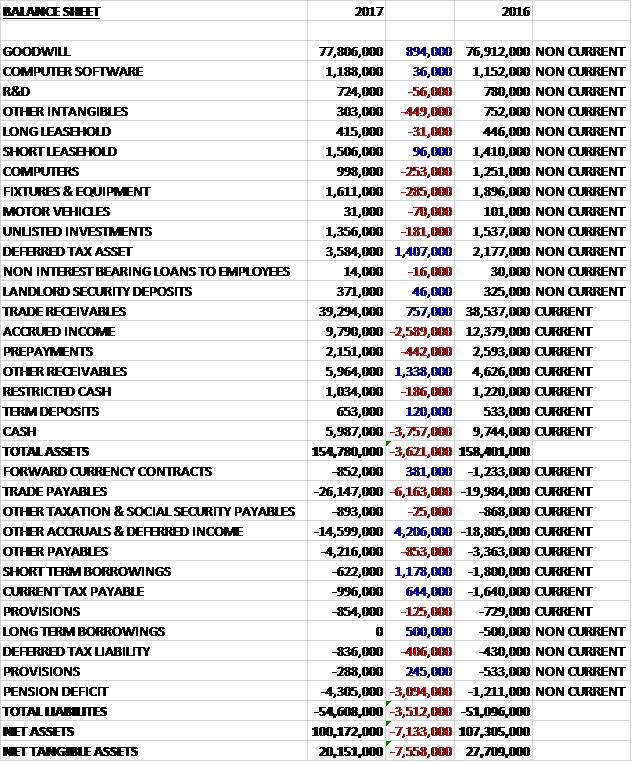

When compared to the end point of last year, total assets declined by £3.6M driven by a £2.9M decrease in accrued income, a £449K fall in other intangibles and a £442K decline in prepayments, partially offset by a £1.4M growth in deferred tax assets, a £1.3M increase in other receivables and an £894K growth in goodwill. Total liabilities increased during the year as a £4.2M decline in accruals and deferred income, a £1.2M fall in short term borrowings and a £644K decline in current tax payables were more than offset by a £6.2M growth in trade payables and an £853K increase in other payables. The end result was a net tangible asset level of £20.2M, a decline of £7.6m year on year.

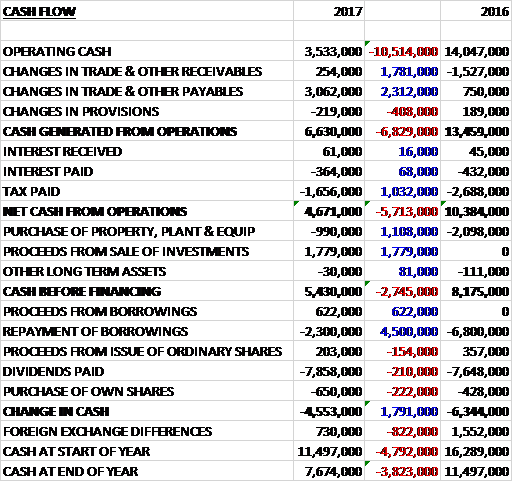

Before movements in working capital, cash profits fell by £10.5M to £3.5M. There was a cash inflow from working capital due to a rise in payables and after tax payments declined by £1M the net cash from operations came in at £4.7M, a decline of £5.7M year on year. The group spent £990K on capex but recouped £1.8M from the sale of the Baltic Exchange shares to give a free cash flow of £5.4M. This didn’t cover the £7.9M paid out in dividends and after the group also paid back some borrowings there was a cash outflow for the year of £4.6M and a cash level of £7.7M at the year-end.

The underlying operating profit in the Shipbroking division was £7.9M, a decline of £1.8M year on year. As expected the business faced tough market conditions marked by falling tanker rates and continued low offshore rates. Despite the fall in profits, transaction volumes increased in virtually all sectors. The total forward order book at the year-end was $39M, of which $20M relates to 2018.

The deep sea tanker market weakened in the year as the growth in tonnage drove freight rates down and the beneficial effects of low oil prices wore off. High product stocks and lower refinery runs caused product carrier earnings to fall steadily throughout the year and tanker asset values continued their steady decline since 2014.

Heavy delays to newbuildings under construction meant that tankers scheduled for delivery in 2016 slipped into 2017 resulting in lower overall fleet growth than expected. In 2017 there is expected to be a similar slippage and a slightly higher level of demolition but that overall capacity will increase. This fleet growth is likely to outweigh growth in seaborne trade volume but tankers trading should be protected to some extent by an average lengthening of voyage distance as Atlantic basin sweet light crudes replace lost heavy sour crude production in the Middle East. This year freight rates will reduce if seaborne imports are replaced from local stocks but will hold up is crude exports from the US, Nigeria or Libya rise to fill a void left by others. Refining margins could suffer if crude prices rise and the resulting drop in run rates could hurt the crude sector. Both crude and product tanker rates stand to recover once local product stocks are drained, however.

There has been a continued expansion to the fleet of LPG and LNG vessels which put pressure on freight rates in the spot market and challenged demand for time charters. Fixture volumes remained steady, however, and the teams overall maintained their level of earnings compared to the previous year. After a challenging first half to the year, the LNG shipping market saw charter rates improve modestly. The start-up of several new projects in the US, Australia and Malaysia has driven supply to record levels.

LPG rates weakened in the year with significant downward pressure felt in the VLGC sector. Despite the fall in earnings the spot market remained active, with seaborne LPG trade expanding during the year with most of the growth in LPG exports coming from production in the US. Saudi LPG exports rose but growth from the rest of the Middle East was flat.

The petrochemical market was turbulent during the year with a significant increase in the number of newbuild vessels adversely impacting freight. As the shipping surplus became evident, owners cancelled new-building orders during the year and there was limited new production in the petrochemical segment. This year there is likely to be a significant number of new vessels delivered into the market with apparently very limited product supply growth.

The offshore desk continued to experience challenging markets as global oil and gas exploration and production activity remained low. The team performed well in these tough market conditions to deliver a profitable result for the year. The board don’t expect much improvement in the market over the next year and it will take some time for any recovery to take effect once exploration and production expenditure increases.

Freight rates in the dry bulk market, which hit an all-time low during the year, were depressed in the first half due to over-capacity and weaker commodity demand in the core markets. Capesize time charters hit their lowest point in March 2016 while the main Panamax, Supramax and Handysize time charter indices all dropped to levels that did not cover daily operating costs. By the end of 2016, however, spot rates were hitting their best levels in two years with time charter rates and vessel values appreciating as the market recovered. The group cut staff numbers but despite this, the teams achieved a similar number of transactions compared to the previous year.

This year growth in dry bulk demand is expected to continue considering widely-expected economic recovery. In the short term the Chinese government’s strategy for the steel and coal sectors will ultimately determine import demand for the two largest dry bulk trades of coal and iron ore but there are also positive developments in grain and agricultural trade which are expected to continue growing.

The sale and purchase team concluded a higher volume of second hand and demolition vessel transactions compared with last year but the average value of vessels was reduced. Towards the end of the year an increased interest in the market for older vessels caused the second hand value of bulk carriers to rise substantially. There has also been some renewed interest in newbuild bulk carriers. As new ballast water treatment regulations come into effect in 2020 there is likely to be an increase in the scrapping of older vessels potentially either reducing the overall fleet or stimulating newbuild demand. Sale and purchase activity in the tanker market has been relatively quiet as tanker freight rates have remained at a level where owners have been able to achieve good earnings from the relatively new fleet.

The underlying operating loss in the Technical division was £2.9M, a detrimental movement of £8.1M when compared to last year. The performance of this division was severely affected by the slowdown in oil and gas exploration and production development activity where a significant proportion of revenue has previously been earned. Drilling activity has also reduced which affected service companies and suppliers with demand for offshore construction, heavy life vessels, supply boats and anchor handlers all reducing significantly. This fall in drilling activity caused a significant reduction in offshore energy premiums for insurance services businesses. Finally, although the world shipping fleet continued to grow there was a general downward trend in claim numbers and claim values with premium levels in the hull and machinery and cargo sectors continuing to decline.

The group has enacted a new structure for the division which will ultimately operate under one brand name. The substantial restructuring programme is now complete and they expect the effects of their actions to generate a £6M annualised cost saving.

The marine warranty surveying and engineering consultancy business was affected considerably by project delays and reduced activity due to the low oil price and reduced exploration and constructions activity in the region. They have reduced their cost base across all offices and the workforce is now scaled appropriately to operate in the current market conditions.

The consulting engineering business concluded its three year project for the design, site supervision and crew training for six LNG carriers in the first half of the year. On completion of this project and in response to the downturn in LNG sector activity, the board relocated staff to their integrated divisional London office. The office in Houston continued its involvement in the development of new technology for the containment of LNG which it started in 2015. Both teams are now focusing on growing their engineering activity and at the end of the year started to see an increase in tender enquiries in both the marine and onshore LNG markets.

The energy loss adjusting business reported a profitable performance in the year despite challenging market conditions. The office in the Middle East performed particularly well with a high level of utilisation. The hull and machinery damage surveying and marine consultancy experienced reduced activity with a lower level of instructions received. The business has also taken steps to address its cost base and saw an increase in utilisation as a result of these actions.

The incident response and environmental consultancy business carried out a routine level of work with no significant project work undertaken in the period. During the year, the business focused on developing its UK operations, particularly retained services and framework agreements with major customers. They terminated their activities in West and Central Africa at the end of contracted business. The business reset its cost base to cater for this change in focus while ensuring that it could still respond to larger incidents as required.

The underlying operating profit in the Logistics division was £1.3M, a decrease of £323K when compared to 2016. The shipping agency business achieved strong business development and an improved financial performance. They have won a number of substantial client accounts and are developing them internationally by delivering high levels of service. As well as maintaining their strong UK business their key focus remains on the expansion of their service in North America and Europe.

The freight forwarding business experienced a tough market this year resulting in a lower level of activity. They have performed a detailed review of all aspects of the business and they are implementing a business development programme across all service areas which they expect to generate and improved performance in the future.

The group incurred £2.5M of acquisition –related expenditure during the year. When they acquired ACM in 2014 they established a share plan to retain key staff and the charge in the year was £1.5M. The annual charge relating to these awards will reduce as these awards vest and they will incur about £1.1M in 2018. The rest of the expenditure relates to the amortisation of acquired intangibles and other activity.

The current financial year has started in line with board expectations.

The group made a loss so there is not much point trying to value it on the current PE ratio but on next year’s consensus forecast the group is trading on a PE of 11.4. After a cut in the dividend the shares are still yielding 5.1% which is expected to grow to 5.5% on next year’s forecast. The board is aiming to cover the dividend 1.5 times (which it certainly isn’t doing currently, it has been unsustainable for some time in my view) At the year-end the group had a net cash position of £7.1M compared to £9.2M at the end of last year.

Overall then this has been a tough year for the group. They were loss making, net assets declined and the operating cash flow decreased although they still made some free cash even if it was not enough to cover dividends. All divisions saw a deteriorating performance but the logistics division did the best as a struggling freight forwarding market dragged down a good performance in the port agency business.

The shipbroking division saw a decline in profits due to falling tanker rates and low offshore rates but it was the technical division which was the real driver of the poor performance. The division struggled with the continued low oil and gas price and the end of the lucrative LNG design contract. It has been restructured, however, so performance should improve in the coming year.

The forward PE stands at 11.4 and the yield is predicted to be 5.5% which, if achieved, actually looks decent value despite the terrible performance of the technical division. I am tempted to dip in here but it would be more prudent to wait for some signs of recovery. Tricky, not sure what to do!

On the 22nd June the group released a Q1 trading update. After a disappointing comparative period for last year, trading profit for the group has improved. While revenues were lower, profitability improved as the benefit of the cost savings measures taken last year were realised.

Trading in the shipbroking division has been good and results show a significant improvement on the prior year’s performance. The tanker desk has achieved improved trading volumes despite lower freight rates. The sale and purchase and project desks have started the year strongly and have concluded some significant new building and long term project business which will benefit future years. The dry cargo desk has shown a marked improvement in performance reflecting the recovering market and the offshore desk is ahead of the prior year with some increase in activity although the market remains low due to asset over capacity.

The performance of the technical services division shows a modest improvement. Solid revenue in the incident led business has offset a lower performance in offshore and engineering which are mainly influenced by energy related projects. The effect on profitability of lower project income is much reduced by the cost savings measures taken last year, however. Over the past few months there have been stronger signs of project related activity as evidenced by the volume of new tenders in the market. Conversion of these opportunities into income will take time but the overall market picture is more encouraging than it was a year ago.

Revenue in the logistics division is in line with prior year equivalent although there has been some margin degradation due to the business mix. Overall the end markets remain challenging and the board’s expectations for the year as a whole remains unchanged. This is a decent update I think actually. There are clearly still some problems but this is looking quite tempting.